The views expressed in this paper are solely the responsibility of the author and do not necessarily reflect the views of the Bank of Slovenia or the Eurosystem.

This policy brief studies the introduction of new temporary taxation on banks and its effects on banks’ lending decisions. Focusing on a unique policy experiment in Slovenia in 2011, where the government imposed a 0.1% tax on banks’ total assets, I find that the introduction of the tax resulted in lower credit supply of loans to corporates. In particular, for each percentage point increase in the share of tax in capital, banks charge on average 8 basis points higher lending rate and decrease their lending amount by 0.5%. The findings of this research carry strong policy implications for countries contemplating or having already implemented windfall or other temporary taxes on banks. The introduction of the tax might lead to a reduction in lending beyond what would be warranted from the standpoint of monetary or other policies.

Several European countries have started imposing windfall or other temporary taxation measures on banks from 2022 on. The surge in inflation and the subsequent policy rate hikes in 2022 and 2023 have significantly boosted banks’ profits, due to almost instantaneous pass-through to lending rates, while banks have shown reluctance to raise deposit rates, largely attributed to large liquidity holdings resulting from previous accommodative monetary policy (see Volk, 2023).

Spain and Italy have emerged as the two largest European economies that have already imposed windfall taxes on banks. Similar measures have been adopted by governments in Hungary, the Czech Republic, and Lithuania, all aimed at taxing the soaring profits of lenders driven by rising interest rates. A temporary taxation on banks has also been introduced by the Slovenian government in response to the significant floods that struck Slovenia in August 2023. While this tax does not specifically target the windfall profits, it shares a comparable ad-hoc nature in its introduction.1

While the governments’ motivations behind the introduction of windfall taxes on banks are rather clear, the potential unintended consequences remain largely uncertain. The ECB has issued warnings to the governments of Spain, Italy, and Slovenia, highlighting potential side effects associated with the proposed temporary taxation on banks.2 Although the ECB’s concerns are tailored to the specific circumstances of each country and their proposed taxation plans, a shared apprehension is the possible adverse impact on bank solvency, financial stability, and the risk of a disproportionate reduction in credit activity—exceeding what would be warranted from a monetary policy perspective.

Motivated by recent tax initiatives in various countries, this policy brief studies the impact of an add hoc introduction of new bank taxation on bank credit supply. It focuses on a unique policy experiment in Slovenia in 2011, where the government imposed a temporary tax on banks total assets. The conclusions drawn from this analysis offer policy implications of an introduction of temporary bank taxation and particularly, of a similar tax measure proposed by the Slovenian government, scheduled for implementation in 2024.

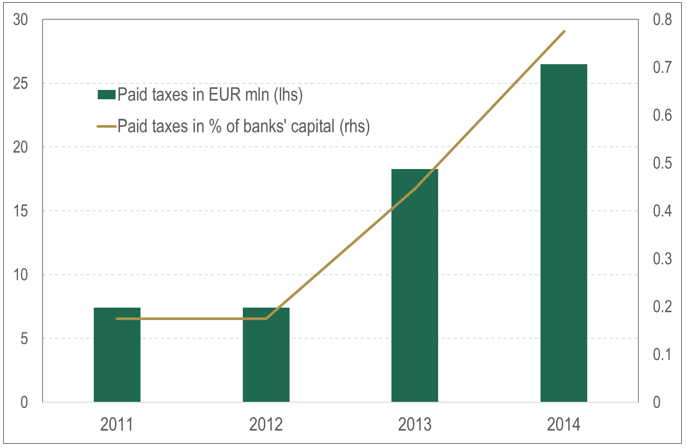

In August 2011, the Slovenian government introduced a temporary taxation measure targeting banks, imposing a 0.1% levy on their total assets.3 The tax was paid once per year and in total banks contributed 60 EUR mln to the government budget between 2011 and 2014 (Figure 1). Several deductions embedded in the tax depleted the ex-post effective tax rate. Although the tax rate was set at 0.1% of banks’ total assets, the actual payments were much lower, 0.03% on average (see Figure 1). First, the levy was lowered by 0.167% (0.1% from 2013 on) of the bank’s outstanding loan amount to firms. Second, banks that increased their lending to firms by the amount that exceed 5% of previous year’s total assets were exempted from paying the tax. Third, banks holding less than a 20% share of loans to firms in their total assets were also exempted.

Figure 1: The amount of paid taxes on banks’ total assets

Source: Banka Slovenije, FURS. The figure shows the amount of paid taxes on banks’ total assets to the government budget, measured in EUR mln and in percent of banks’ capital. As the tax was introduced in August 2011, the payment in 2011 reflects 5/12 of the total annual amount.

The idea underlying the outlined deductions and exemptions aimed to encourage banks to increase lending to firms during financial crises when obtaining external funding became challenging. However, this approach faced strong criticism from the Bank of Slovenia and the ECB. Both institutions expressed concerns about the potential threat to financial stability if banks were incentivized to engage in potentially risky lending practices merely to reduce their tax liabilities.4 Additionally, the Bank of Slovenia cautioned against potential adverse and unintended consequences of the tax, as it could lead to an increase in lending rates for the overall economy.

The analysis focuses on the policy’s introduction in August 2011, since the later stages are likely endogenous due to deduction items that incentivized lending. I estimate the change in lending rates and amounts in a narrow window after the introduction of the policy and how this change is related to the exposure of an individual bank to the taxation. The latter is defined as the amount of tax a bank would be required to pay in July 2011, which is one month before the official introduction of the new tax to mitigate the endogeneity concerns. I apply the methodology proposed by Degryse et al. (2019) that absorbs the demand side with industry-location-size-time fixed effects and I further include bank fixed effects and other controls: loan maturity, credit rating, collateral and interest rate fixation.

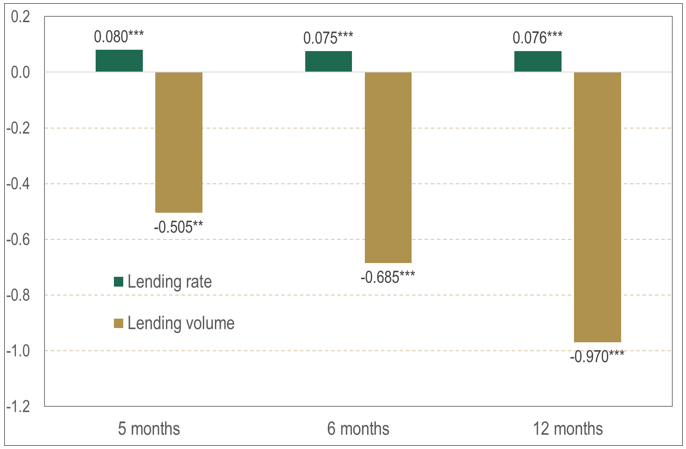

Leveraging on detailed credit register data, the results indicate that the introduction of the tax caused a reduction in the availability of loans, leading to higher lending rates and diminished loan volumes. In particular, I find that with every percentage point rise in exposure to the tax, banks, on average, raise their lending rates by 8 basis points and decrease lending amounts by 0.5% within five months following the policy introduction (Figure 2). This implies that a bank at the 90th percentile in the distribution of tax exposure, with 0.84% exposure in its capital, charges on average 7bp higher lending rate to firms and decreases credit amount by 0.42%, compared to a bank at the 10th percentile, which has close to zero exposure to the taxation. These results hold true even over longer periods, extending up to one year.

Figure 2: The impact of bank taxation on bank credit supply

Source: Banka Slovenije, own estimates. The figure reports the estimated diff-in-diff coefficients of the impact of bank taxation on credit supply in the horizon of 5 and up to 12 months after the policy change. The variable of interest is either lending rate on new loans or the log of outstanding loan amount, measured at firm-bank-time level.

The presented results add to the ongoing discussion regarding the impact of bank taxation on bank behaviour. The existing literature on this subject is relatively limited and most of the papers conclude that tax shocks lead to lower lending volumes (Buch et al., 2016 and Sobiech et al., 2021) and higher lending rates (Capelle-Blancard and Havrylchyk, 2017 and Kogler, 2019). While most of the studies focus on changes in corporate tax or study the tax on bank liabilities, this paper presents novel evidence on the impact of a tax specifically targeting banks’ assets. This inherent characteristic of the tax creates a direct link to the incentives driving banks to manage and streamline their balance sheets, offering a unique perspective on the broader impact of taxation on banking behaviour.

The conclusions drawn this analysis carry important implications for policymakers. I show that the imposition of new taxes is likely to prompt banks to contract their lending supply, which could intersect and potentially clash with other policy measures, such as monetary and macroprudential policies. For example, the implementation of a similar tax in the current economic environment could amplify credit contraction beyond those stemming from an elevated policy rate, a scenario that may run counter to the objectives of monetary policy.

Based on the presented estimates, a 0.2% tax on banks’ assets, proposed by the Slovenian government from 2024 on5, would result in a 14 basis points increase in lending rates and a 1% reduction in credit availability. Several noteworthy points merit attention. Currently, the banking system differs significantly from its state in 2011, having strong capitalization, a minimal share of NPLs, and substantial profits fuelled by rising interest rates. Consequently, one might expect a milder impact in the current economic environment. However, it is important to note that the exposure to the tax would now be more substantial than in 2011. In 2011, a median bank’s exposure was merely 0.3% of its capital, compared to current 1.8%. Additionally, the estimates show only the immediate response of banks to the tax introduction, whereas the 0.2% tax rate is planned to be in place for five years, potentially exerting additional strain on credit supply in subsequent years.

Claudia M Buch, Bjorn Hilberg, and Lena Tonzer (2016). Taxing banks: An evaluation of the German bank levy. Journal of banking & finance, 72:52-66.

Gunther Capelle-Blancard and Olena Havrylchyk (2017). Incidence of bank levy and bank market power. Review of Finance, 21(3):1023-1046.

Hans Degryse, Olivier De Jonghe, Sanja Jakovljević, Klaas Mulier, and Glenn Schepens (2019). Identifying credit supply shocks with bank-firm data: Methods and applications. Journal of Financial Intermediation, 40:100813.

Michael Kogler (2019). On the incidence of bank levies: theory and evidence. International Tax and Public Finance, 26(4):677-718.

Anna L Sobiech, Dimitris K Chronopoulos, and John OS Wilson (2021). The real effects of bank taxation: Evidence for corporate financing and investment. Journal of Corporate Finance, 69:101989.

Matjaž Volk (2023). Is the ECB monetary tightening effective? The role of bank funding and asset structure. Applied Economics Letters, forthcoming.

See description in the article by The Slovenia Times.

See ECB’s opinion for the proposed tax measures in Spain, Italy and Slovenia.

See Official Gazette of the Republic of Slovenia, no. 59.

See ECB’s opinion on the proposed tax measure in 2011.

See the description of the law in the Opinion by the ECB.