The views expressed in this Policy Brief are solely the responsibility of the authors and should not be interpreted as reflecting the views of Sveriges Riksbank.

Actors in the political landscape have different tools to influence voters’ beliefs. For instance, the government can use fiscal policy adjustments ahead of elections to sway voters in their preferred direction. This is the well-known Political Budget Cycle. We argue that also economic forecasts might be used ahead of elections to influence voters’ beliefs. In a theoretical model of political selection, we show that governments have an incentive to release overly optimistic GDP growth forecasts ahead of elections in order to increase the re-election probability. Using high-frequency forecaster-level data from the United States, the United Kingdom, and Sweden, we also empirically document such behavior. Specifically, we find that governments overestimate short-term real GDP growth by 0.1–0.3 percentage points during campaign periods, relative to off-campaign periods and private forecasters.

Voters use elections to select their preferred politicians and ensure the accountability of elected officials once they are in office. However, this tool has limitations when voters lack sufficient knowledge about the competing candidates. Suppose voters cannot observe the true competence of politicians. In that case, they instead need to use observable signals to update their beliefs about the competing candidates.

Voters can, for example, use fiscal-policy and economic-growth outcomes to update their beliefs about the incumbent candidate. However, incomplete information provides an incentive for the incumbent to adjust fiscal policy ahead of elections to influence voters’ beliefs and thereby increase the re-election probability. This is the well-known Political Budget Cycle.1

However, elections occur before the complete realization of the effects of policy decisions on public goods or economic growth. Therefore, to evaluate the incumbent candidate thoroughly, voters need to form expectations about the future effects of already implemented policies. Forming such expectations is challenging, and voters must seek readily available information. Macroeconomic forecasts published by governments are publicly available and reported in mass media. Therefore, voters may use these forecasts when forming beliefs about the economy and the incumbent politician’s ability. In turn, if voters interpret economic performance as a signal of a leader’s ability, the incumbent leader can gain an electoral advantage by intentionally manipulating the forecasts released to the public before an election. Hence, on top of strategically using fiscal policy, the incumbent government may also strategically manipulate forecasts to gain an electoral advantage.

The notion of politically compromised forecasts can be further motivated by anecdotal evidence. One example of politically compromised forecasts in the public debate is the 2010 general elections in the United Kingdom. David Cameron claimed “fiddled forecasts and fake figures” – when blaming the Labour party for how they were handling the economy and the government for the quality of forecast releases. After the 2010 general election, the newly appointed government created the Office for Budget Responsibility with the primary purpose of providing unbiased forecasts and ending government interference with economic and fiscal forecasting (Giugliano, 2015, in the Financial Times). A second example comes from Italy. Former Prime Minister Berlusconi claimed that his government had created 1.5 million jobs in the economy. Despite lacking evidence that Italy experienced such a large increase in occupation over the period or that newly created jobs were due to government interventions (Guzzi and Lisciandro, 2018), Berlusconi has continuously reported the figure, including during the 2018 campaign.

In a recently published paper in the Journal of Economic Behavior & Organization, entitled Electoral Cycles in Macroeconomic Forecasts (Cipullo and Reslow, 2022), we provide a theoretical rationale for electoral incentives in macroeconomic forecasts released by the government.2 We also empirically confirm several theoretical predictions using data from the United States, the United Kingdom and Sweden – suggesting that governments indeed use macroeconomic forecasts to influence voters.

Voters care about the economy and have ideology (i.e., idiosyncratic) preferences. In each period, the politician in office implements a fiscal policy as a function of her innate ability. The economic outcome (say, GDP growth) comes as a combination of fiscal policy and an exogenous shock to productivity. Neither voters nor the incumbent perfectly observes the current or future state of the economy. However, the incumbent receives unbiased noisy information about the economy. During the campaign period, the incumbent releases forecasts, and voters use noisy observations of the forecast as a signal of the incumbent’s ability when deciding whether to re-elect her or not. The incumbent is office-motivated and faces a trade-off between the accuracy of the released forecast (due to reputational concerns) and the incentive to bias the estimates to increase re-election probability.

This model provides several intuitive predictions. First and foremost, it predicts the existence of bias. The model predicts that, in the run-up to elections, the government will overestimate economic growth to influence voters’ beliefs. The model also predicts that term-limited incumbents will release more accurate forecasts than incumbents who can run for re-election, and that the bias is reduced if the government is not aligned with the parliament. In addition, the model also predicts that a larger bias should arise when the incumbent expects a close election.

We test the predictions of the theoretical model by exploiting high-frequency panel data at the forecaster level from the United States, Sweden, and the United Kingdom. We rely on data that contains the short-term (current and next year) real GDP growth forecasts from multiple forecasters for all three countries. For all countries, we observe the ex-post forecast error of government and private forecasters, during campaign and off-campaign periods.

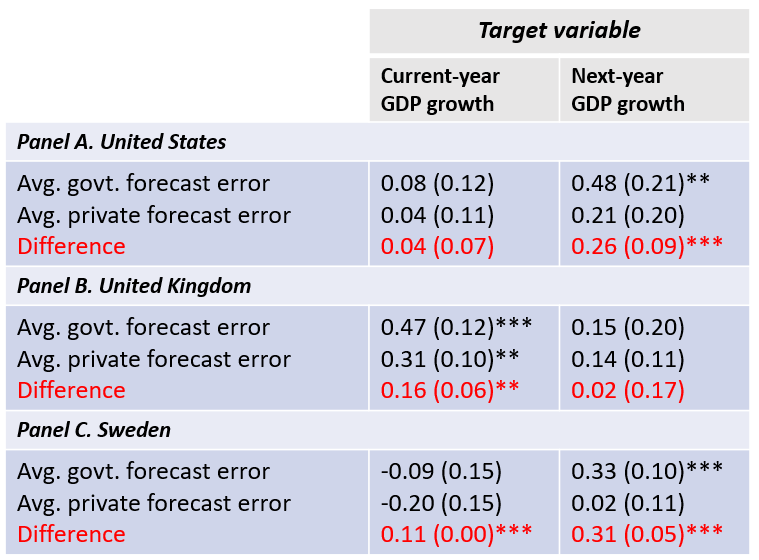

As summarized in Figure 1 and reported in the published manuscript, the data supports all the theoretical predictions summarized above.

Figure 1: Government and private-sector GDP growth forecast error

Notes: Forecast error is defined as the difference in percentage points between the average released forecast and the ex-post realization of GDP growth in the target period. Coefficients are obtained from estimating the Difference-in-Differences model in Cipullo and Reslow (2022). Standard errors are reported in parentheses. *, **, *** represent the 10%, 5%, and 1% significance levels, respectively.

First, we find that in all countries in our sample, the government overestimates future real GDP growth by 0.1–0.3 percent points in their estimates released in the months approaching an election compared to the other forecasters in the economy and the government itself in off-election years and the months following the vote. More specifically, Figure 1 documents that the US government (where elections take place at the end of the year) tends to bias forecasts that target GDP growth in the next period. Conversely, in the United Kingdom (where elections take place earlier in the year), the government tends to bias forecasts that target the current-year GDP growth. In Sweden, where elections take place during the summer, governments tend to overestimate both the current-year and the next-year GDP growth forecasts.

Second, we find that, in the United States, the government does not release biased forecasts when the president is term-limited and that government forecasts are relatively less biased when the president is not politically aligned with both branches of Congress.

Third, using opinion poll data, we disclose that incumbent governments overestimate real GDP growth ahead of elections significantly more when they expect a close election than when they expect a more clear victory or defeat.

Although we do not have any evidence on the degree of rationality in voters’ ability to understand bias in government forecasts, our theoretical model allows analyzing the two extreme cases of fully naïve and fully rational voters.

Suppose voters are rational in the sense that they expect the government to release biased estimates. In this case, they can account for it in expectations, and the signaling tool used by the politician will represent a Pareto inefficiency. The bias is costly and does not increases the equilibrium probability of winning the election. However, politicians who cannot commit credibly not to bias and are forced to do so as long as voters expect them to overestimate economic growth.

Suppose instead that voters are naïve in the sense that they do not expect the government to overestimate the state of the economy intentionally. In this case, the politician will gain a large electoral advantage in equilibrium thanks to the bias since voters will associate that favorable economic outlook with a high-ability politician. Hence, voters will overestimate the ability of the incumbent politician. Compared to a counterfactual world with no bias, voters would be worse off because of systematic voting mistakes, while incumbent politicians would be better off thanks to an increased re-election probability.

In turn, the overestimation of economic growth generates an incumbency advantage only if voters do not expect the government to release biased estimates. The bias is present in the case of both rational and naïve voters, yet the mechanisms behind it and the consequences for the electoral competition change substantially. While the bias arises from lack of commitment under rational voters, it comes from manipulation of voters’ beliefs if voters are naïve.

Our theoretical model assumes, for simplicity, that fiscal policy is exogenously determined by the innate ability of the incumbent politician and a random shock. This assumption allows us to show that electoral manipulation of macroeconomic forecasts can also be rational when politicians do not use it as an instrument to manipulate fiscal policy ahead of elections. While it is beyond the scope of our study to study if fiscal policy and forecasting are independent of each other, substitutes, or complements, we provide, using data on major tax reforms, evidence that electoral cycles in macroeconomic forecasts also exist in years when the government does not take significant fiscal policy decisions. This evidence confirms that forecasting bias may also exist in the absence of political budget cycles, as predicted by the model.

Biased forecasts pose a problem if voters fail to account for the electoral incentives behind their release. In addition to a potential reduction of voters’ welfare, biased forecasts could also damage the economy in a broader perspective. Firms update their beliefs when presented with information about forecasts from professionals and the government. In addition, firms’ beliefs about the economy impact their investment and employment decisions. Hence, the bias can result in inefficient firm and household decisions.

The policy implications of our study echo those from the central bank independence literature. One of the main points of Rogoff’s theory of the conservative central banker (Rogoff, 1985) is that independence reduces politically induced variability and bias. Separating monetary policy from electoral incentives may serve to shield the economy from political business cycles by removing pre-election manipulation of monetary policy as in the Nordhaus (1975) model or reducing partisan shocks to policy as in the Alesina (1988) model. Likewise, in the case of government forecasts, the public would benefit from receiving forecasts also from independent agencies with the sole purpose of providing unbiased estimates. Guaranteeing independence and removing electoral incentives is however not a trivial task. Our work, indeed, documents that independent government forecasting agencies in Sweden (which are in the market at the same time as the Ministry of Finance) do not overestimate GDP growth ahead of elections. On the contrary, the outsourcing of the forecasting function from the government to the OBR, which we briefly discussed in the introduction, according to our data, did not succeed in avoiding pre-election forecasting bias.

Akhmedov, A. and Zhuravskaya, E. (2004). Opportunistic Political Cycles: Test in a Young Democracy Setting. The Quarterly Journal of Economics, 119(4):1301–1338.

Alesina, A. (1988). Macroeconomics and Politics. NBER Macroeconomics Annual, 3:13– 52.

Alesina, A., Cohen, G. D., and Roubini, N. (1992). Macroeconomic Policy and Elections in OECD Democracies. Economics & Politics, 4(1):1–30.

Alesina, A. and Paradisi, M. (2017). Political Budget Cycles: Evidence from Italian Cities. Economics & Politics, 29(2):157–177.

Bohn, F. and Veiga, F. J. (2021). Political Forecast Cycles. European Journal of Political Economy, 66:101934.

Boukari, M. and Veiga, F. J. (2018). Disentangling Political and Institutional Determinants of Budget Forecast Errors: A Comparative Approach. Journal of Comparative Economics, 46(4):1030–1045.

Boylan, R. T. (2008). Political Distortions in State Forecasts. Public Choice, 136(3):411– 427.

Brender, A. and Drazen, A. (2013). Elections, Leaders, and the Composition of Government Spending. Journal of Public Economics, 97:18–31.

Cipullo, D. And Reslow, A. (2022). Electoral Cycles in Macroeconomic Forecasts. Journal of Economic Behavior & Organization, 202:307-340.

Drazen, A. and Eslava, M. (2010). Electoral Manipulation via Voter-Friendly Spending: Theory and Evidence. Journal of Development Economics, 92(1):39–52.

Giugliano, F. (2015). Robert Chote Reappointed as Chairman of OBR. Financial Times, September 16, 2015.

Guzzi, G. and Lisciandro, M. (2018). Il Contratto di Berlusconi con le Bufale. lavoce.info, February 16, 2018.

Kauder, B., Potrafke, N., and Schinke, C. (2017). Manipulating Fiscal Forecasts. Finanzarchiv, (2):213–236.

MacRae, C. D. (1977). A Political Model of the Business Cycle. Journal of Political Economy, 5(2):239–263.

Nordhaus, W. D. (1975). The Political Business Cycle. The Review of Economic Studies, 42(2):169–190.

Picchio, M. and Santolini, R. (2020). Fiscal Rules and Budget Forecast Errors of Italian Municipalities. European Journal of Political Economy, 64:101921.

Repetto, L. (2018). Political Budget Cycles with Informed Voters: Evidence from Italy. The Economic Journal, 128(616):3320–3353.

Rogoff, K. (1985). The Optimal Degree of Commitment to an Intermediate Monetary Target. The Quarterly Journal of Economics, 100(4):1169–1189.

Rogoff, K. (1990). Equilibrium Political Budget Cycles. American Economic Review, 80(1):21–36.

Rogoff, K. and Sibert, A. (1988). Elections and Macroeconomic Policy Cycles. The Review of Economic Studies, 55(1):1–16.

Shi, M. and Svensson, J. (2006). Political Budget Cycles: Do They Differ Across Countries and Why? Journal of Public Economics, 90(8-9):1367–1389.

Seminal work by Nordhaus (1975) and MacRae (1977) on political business cycles proposed models in which politicians exploit the Phillips curve by inflating the economy during election years to reduce unemployment. Rogoff and Sibert (1988) and Rogoff (1990) later contributions expanded the analysis to taxes, government spending, and deficits, resulting in the vast literature on political budget cycles. Empirical evidence of electoral cycles in fiscal policy can be found in, e.g., Akhmedov and Zhuravskaya (2004); Alesina et al. (1992); Alesina and Paradisi (2017); Brender and Drazen (2013); Drazen and Eslava (2010); Repetto (2018); and Shi and Svensson (2006).

Earlier work on pre-election biased forecasts focused on the government’s manipulation of revenues and expenditures forecasts to expand their fiscal room for pre-election manipulation of fiscal policy (e.g., Bohn and Veiga, 2021; Boukari and Veiga, 2018; Boylan, 2008; Kauder et al., 2017; Picchio and Santolini, 2020.