This article was first published in the ECB Research Bulletin. It was written by Luca Nocciola and Alejandro Zamora-Pérez, drawing on selected results of Nocciola and Zamora-Pérez (2024). The authors gratefully acknowledge the comments by Ulrich Bindseil, Piero Cipollone, Ignacio Terol, Anton van der Kraaij, Claudia Lambert, Livio Stracca, Gareth Budden, Alexander Popov and Luc Laeven. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.

What factors could drive transactional demand for central bank digital currency (CBDC)? We analyse payment survey data to arrive at a framework for understanding the role of adoption frictions and design strategies in shaping CBDC demand. The results of our analysis show that, while consumers may initially prefer to use more traditional payment methods, a design tailored to their specific needs could significantly increase CBDC uptake. Raising awareness and capitalising on network effects could also boost demand for CBDC.

Central banks are at various stages in investigating and developing central bank digital currencies (CBDCs) alongside cash. While cash use is losing ground to digital private payment methods, the role of public money in payments remains crucial. The potential implications of a society without public money has long been a topic of debate1, highlighting concerns about maintaining its key role in payments. In the digital era, these discussions have resurfaced in central banking and academia. The Eurosystem is now preparing for the potential development of a digital euro alongside cash, the use of which is declining. One of the main motivations for introducing a CBDC is to consolidate the role of public money as the anchor of the monetary system (Lagarde and Panetta, 2022), a sentiment not confined to the euro area alone. In 2022 the Bank for International Settlements conducted a survey of 86 central banks, which revealed that the main reason for introducing a CBDC was to enhance payment efficiency and safety (Kosse and Mattei, 2023). Central banks’ ongoing efforts in CBDCs reflect global momentum and interest in the future of public money in payments.

While there is considerable interest in issuing CBDCs, one challenge lies in striking the right balance between “too much” and “too little” consumer demand (Ahnert et al., 2022). Extensive research has already tackled situations in which a CBDC might become too popular, potentially undermining the banking system (Burlon et al., 2024; Assenmacher et al., 2024). However, much less research has gone into ensuring there is sufficient interest in a CBDC for it to be used as a regular means of payment. Despite being universal to any CBDC, this challenge has been identified and qualitatively assessed in the euro area (Bindseil et al, 2021; Panetta, 2022 and Kantar Public, 2022). Here, drawing on Nocciola and Zamora-Pérez (2024), we shed further light on this “too little” scenario. Using a model based on survey data, we quantitatively examine some of the potential drivers and barriers to CBDC adoption and discuss strategies to overcome these obstacles.

Advances in the digital payments landscape underscore the importance of understanding the extent to which consumers might use a CBDC as a new form of digital currency and the need for comprehensive data on consumers’ current payment methods. To that end, the study on payment attitudes of consumers in the euro area (SPACE)2 collects survey data on current consumer behaviour and preferences concerning payment methods. The 2022 edition of SPACE spanned 17 euro area countries with over 40,000 respondents. The survey includes a payment diary, in which respondents recorded their transactions and respective means of payment, together with a questionnaire asking them to rank different payment instruments according to their most important attributes, such as transaction speed and convenience.

Using this data and on the basis of a model, we study how consumers’ payment choices are related to current preferences for certain attributes of payment instruments.3 We simulate a CBDC that resembles existing means of payment and assess the transactional demand for it. Payment methods, including CBDC, are distilled into various attributes, encompassing features like ease of use, transaction speed and safety. Additionally, we exploit consumers’ preferences for features such as budgeting usefulness and privacy protection.4 Comparing these attributes with familiar benchmarks such as cash and cards offers a framework for exploring the different designs of a CBDC.

To this end, it is important to differentiate between adoption and usage when discussing the uptake of new payment methods. We cannot assess novel payment technologies like a CBDC on the same playing field as entrenched methods like cash and cards. First, there is the adoption phase: this is when consumers decide to include a new payment method in their repertoire. But adopting a method does not necessarily translate into using it regularly. For instance, some consumers might prefer the idea of a CBDC and choose to adopt it, but if they have a deeply ingrained habit of using cash, they might not use the CBDC often in practice.

We find that adoption costs play a pivotal role in determining the success of new payment methods. Introducing a novel payment method presents an inherent “cost” to consumers, and this is not purely a monetary cost – it also encompasses the effort, time and adjustments required of consumers when adapting to a new payment method. Previous qualitative findings show that some consumers are satisfied with current methods based on familiar technologies and prefer less complexity rather than adopting new methods (Kantar 2022; Kantar Public 2023). In contrast to those studies, we gauge this cost quantitatively by exploiting the SPACE survey and delving into the adoption patterns of mobile payment apps – a technology that, despite being available for some time, has only gained traction in the sampled countries relatively recently.5 The idea behind our approach is straightforward: if those accustomed to cash and cards hesitate to embrace mobile payments due to the perceived cost of switching, they might exhibit similar reluctance towards another newly introduced means of payment, such as a CBDC. Our findings show that consumers generally face a substantial adoption cost, revealing a preference for established payment methods like cash or cards and a tendency to stick to familiar habits.6 However, pinpointing the reasons for this cost offers avenues to lowering it.

Key among the strategies that central banks may consider is addressing those factors that drive CBDC adoption. We identify three potential drivers – design alignment with consumer preferences, effective information dissemination, and leveraging network effects from emerging payment technologies.

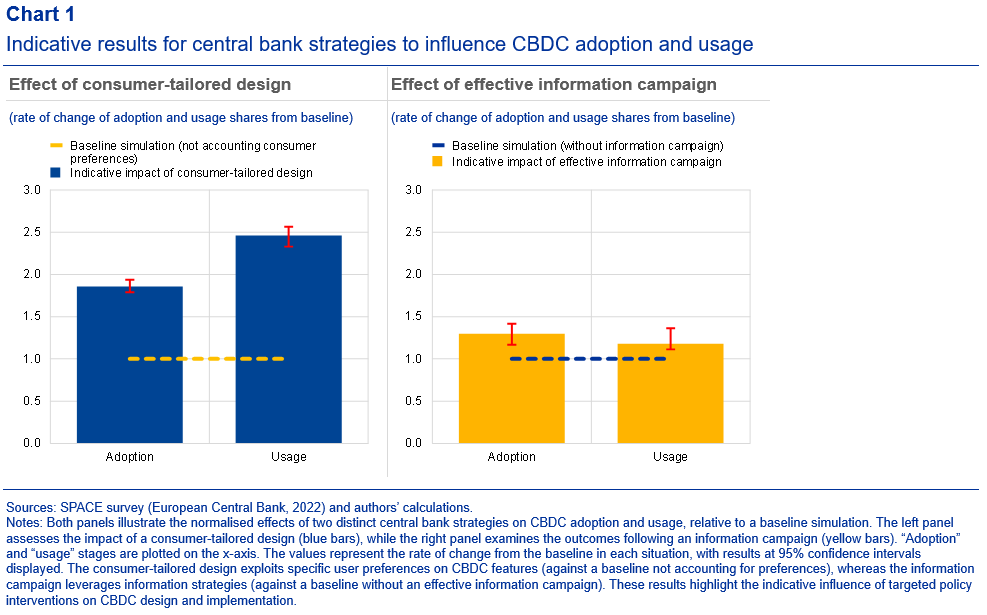

For a start, a CBDC’s design attributes can heavily influence how attractive it is to users. Our study suggests that CBDC demand could be influenced by merging the perceived top qualities of cards (like speedy transactions and ease of use) with the benefits of cash (such as tracking expenses and preserving privacy). The left panel of Chart 1 offers a glimpse into the potential impact of a CBDC tailored to consumer preferences, compared with one that is not. While it is essential to view these findings as indicative results rather than fixed outcomes – given the interplay of various factors – the chart does seem to suggest that a well-designed CBDC would enjoy more substantial adoption and regular usage.

Second, ensuring consumers have the right information can make it easier for them to embrace new payment methods, such as a CBDC. The literature often highlights the crucial role that raising awareness plays in boosting the appeal of novel technologies, including payment methods. To gain a clear and causal understanding of how new information influences payment choices, we need to look at an unexpected event or “exogenous shock” that might change the usual consumer behaviour. The COVID-19 pandemic provides such an opportunity. This unforeseen event significantly altered many consumers’ habits. The SPACE survey delves into these changes, specifically asking participants if discovering new payment methods due to the pandemic influenced their payment choices even two years later. Our model exploits this information from the SPACE survey, and we find that discovering new payment options, like mobile apps, can significantly reduce the barriers people face when adopting a new means of payment. Based on this fact, we model what might happen if there was a targeted campaign to raise consumers’ awareness of a CBDC as a prospective means of payment. The results depicted in the right panel of Chart 1 suggest that with the right targeted information, consumers might find it easier to make the switch to a CBDC. However, it is important to note that these results should not be seen as an attempt to make an accurate inference, but rather as indicative insights illustrating the potential influence of effective information dissemination on consumer behaviour towards CBDCs.

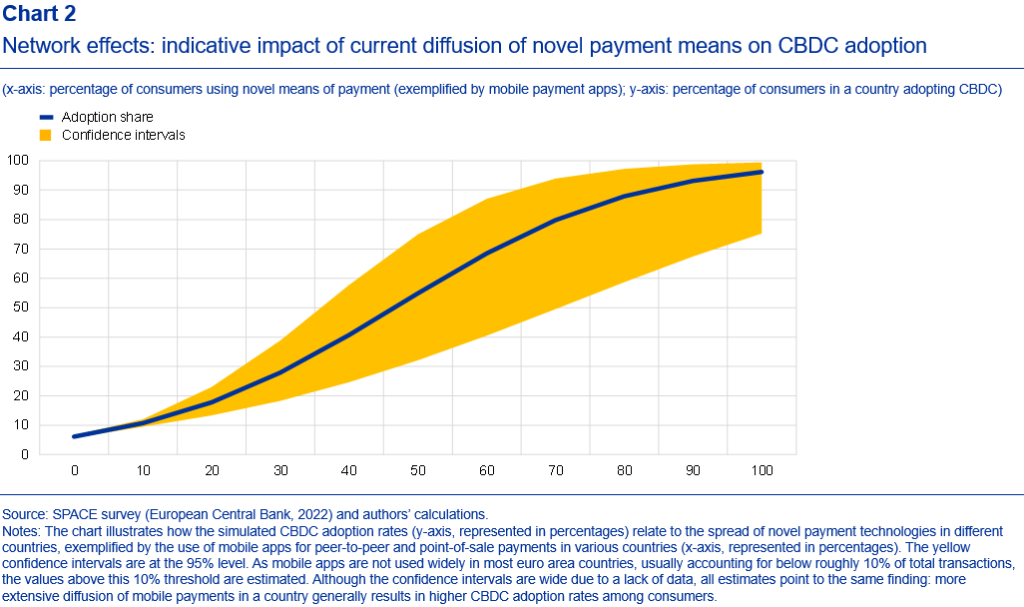

Network effects fuelled by the spread of emerging payment technologies can substantially boost CBDC adoption. The diverse landscapes within the sampled countries, as captured by the SPACE survey, reveal differences in both payment habits and available payment options across different countries. This variation can be exploited to analyse the relevance of an environment that is favourable to new payment methods.7 Chart 2 shows the importance of an environment in which new payment technologies are gaining traction, because the collective adoption of a method can be self-reinforcing. As more people use new payment methods, like mobile apps, their popularity snowballs, creating an environment where the adoption of new payment technologies – including CBDC – becomes more likely. We find that network effects can act as powerful multipliers, making markets receptive to emergent payment technologies fertile grounds for promoting CBDC.

Finally, although we lack the data necessary to produce the relevant simulation, it is likely that other important factors could boost CBDC adoption, such as the role of legislation in ensuring its distribution and obliging merchants to accept it at the point of sale, as found in Kantar Public (2022). These two components of the role of legislation could be important in accelerating these network effects, as suggested by Bindseil et al. (2021). Additionally, the universality of use cases could further enhance adoption.8

We assess potential drivers for the adoption of CBDC as a means of payment, providing insights which could contribute to the design of adoption strategies. In the digital age, the role of public money in our daily transactions is evolving, and it is important to ensure that CBDCs can effectively fit into this changing landscape. Drawing on the SPACE survey data, we develop a framework to quantitatively measure how likely consumers are to use CBDC as a means of payment in everyday transactions, by accounting for individuals’ preferences for payment method attributes. We distinguish between the initial decision to adopt a CBDC and the subsequent decision to use it, emphasising that the costs and barriers associated with the initial adoption phase are vital in understanding overall demand. Building on insights from previous qualitative research, our analysis confirms that three drivers are key to consumer demand: how CBDC is designed, the level of consumer awareness and the growth of current new payment technologies. However, we do not cover all potentially relevant factors, such as the role of legislation in exploiting network effects, ensuring efficient distribution, and boosting adoption through universal use cases. In sum, our research provides a framework for understanding the role of adoption costs and design strategies in shaping demand for CBDC.

Ahnert, T., Assenmacher, K., Hoffmann, P., Leonello, A., Monnet, C. and Porcellacchia, D. (2022). “Cold hard (digital) cash: the economics of central bank digital currency”, ECB Research Bulletin No 100, Frankfurt am Main.

Assenmacher, K., Ferrari Minesso, M., Mehl, A., and Pagliari, M. S. (2024). “Managing the transition to central bank digital currency“, ECB Working Paper Series, No. 2907, Frankfurt am Main.

Bindseil, U., Panetta, F. and Terol, I. (2021), “Central Bank Digital Currency: functional scope, pricing and controls“, ECB Occasional Papers, No 286, Frankfurt am Main.

Black, F. (1987), “Banking and interest rates in a world without money” in F. Black, Business Cycles and Equilibrium , Oxford: Basil Blackwell, pp. 1 1-20.

Burlon, L., Muñoz, M. A. and Smets, F. (2024), “The Optimal Quantity of CBDC in a Bank-Based Economy”, American Economic Journal: Macroeconomics (forthcoming)

European Central Bank (2020), The Eurosystem cash strategy.

European Central Bank (2022), Study on the payment attitudes of consumers in the euro area (SPACE) – 2022, European Central Bank, Frankfurt am Main.

Friedman, B. M. (1999), “The future of monetary policy: The central bank as an army with only a signal corps?” International Finance , Vol 2 No. 3, pp. 321-338.

Huynh, K. P., Molnar, J., Shcherbakov, O. and Yu, Q (2020), “Demand for payment services and consumer welfare: the introduction of a central bank digital currency”, Bank of Canada Staff Working Paper, No 2020-7, Bank of Canada, Ottawa.

Kantar Public (2022), Study on new digital payment methods, March.

Kantar Public (2023), Study on digital wallet features, March.

King, M. (1999), “Challenges for monetary policy: new and old”, Quarterly Bulletin, Bank of England, Vol. 39, pp. 397-415.

Kosse, A. and Mattei, I. (2023), “Making headway headway-Results of the 2022 BIS survey on central bank digital currencies and crypto” BIS Paper , No 136, Bank for International Settlements, Basel.

Lagarde, C. and Panetta, F. (2022), “Key objectives of the digital euro”, The ECB Blog, 13 July.

Li, J. (2022), “Predicting the demand for central bank digital currency: a structural analysis with survey data” Journal of Monetary Economics , Vol. 134, pp. 73-85.

Nocciola, L. and Zamora-Pérez, A. (2024) “Transactional demand for central bank digital currency”, ECB Working Paper Series , No 2926, Frankfurt am Main.

Panetta, F. (2022), “A digital euro that serves the needs of the public: striking the right balance”, Introductory statement at the Committee on Economic and Monetary Affairs of the European Parliament, Brussels, 30 March.

Wicksell, K (1936), Interest and prices, Ludwig von Mises Institute.

Woodford, M. (2000), “Monetary policy in a world without money”, International Finance, Vol. 3, No 2, pp. 229-260.

Zamora-Pérez, A. (2021), “The paradox of banknotes: Understanding the demand for cash beyond transactional use”, ECB Economic Bulletin, Issue 2, European Central Bank, Frankfurt am Main.

Historical discussions on the challenges of a cashless economy – and, by extension, an economy without public money in payments – date back to Wicksell (1936), who inquired as to whether private banks could control price fluctuations in a credit-only system. Over time some economists (Black, 1987; King, 1999; and Friedman, 1999) have expressed concerns about the overall effectiveness of the central bank’s policies in such scenarios, while others have downplayed potential risks (Goodhart, 2000; and Woodford, 2000).

See European Central Bank (2022).

There are similar studies by Huynh et al (2020) and Li (2023).

According to previous qualitative surveys, these attributes also play an important role for consumers when considering the prospective adoption of new means of payment (Kantar Public, 2023).

Despite over two decades of mobile payment availability, usage remains limited, particularly at the POS. In 2022, mobile apps accounted for just 3% of POS payments on average, with usage ranging from 1% in Slovenia to 10% in the Netherlands, according to the latest SPACE survey data. However, mobile payments are increasingly being used for person-to-person (P2P) transactions, averaging 10% in 2022, up from 3% in 2019, from 1.5% in Austria to 43% in the Netherlands.

Our findings should not be interpreted as a direct extrapolation of demand for any specific CBDC.

Although our analysis primarily assesses the impact at the point-of-sale, we also address the potential influence of the person-to-person (P2P) use case, in line with findings that highlight its relevance (Kantar Public, 2023). Hence, our simulation includes data on the aggregate usage of both P2P and POS transactions with novel means of payment, such as mobile payments, to estimate the potential level of adoption of a CBDC.

Our data primarily focus on established payment features and do not explicitly capture preferences for innovative features identified in the referenced qualitative surveys which still have a low adoption rate, such as QR code payments, offline payments, conditional payments or the benefit of integrated payment solutions. While these innovative features are among the unobservable factors that influence consumer behaviour in our model, the absence of specific data on them precludes detailed policy simulations.