The collapse of global trade during the COVID-19 crisis was stunning in its magnitude, but in relative terms it was actually milder than during the global financial crisis. Trade has also recovered much more rapidly from the COVID-19 crisis. Analysis of demand-side factors suggests that a key factor explaining this development could be the composition of demand. The contributions of consumption and service sector demand on the import contraction were notably larger during the COVID-19 crisis than during the global financial crisis. This could lead to relatively milder import contraction, as consumption and service production are less import-intensive than investment and manufacturing production.

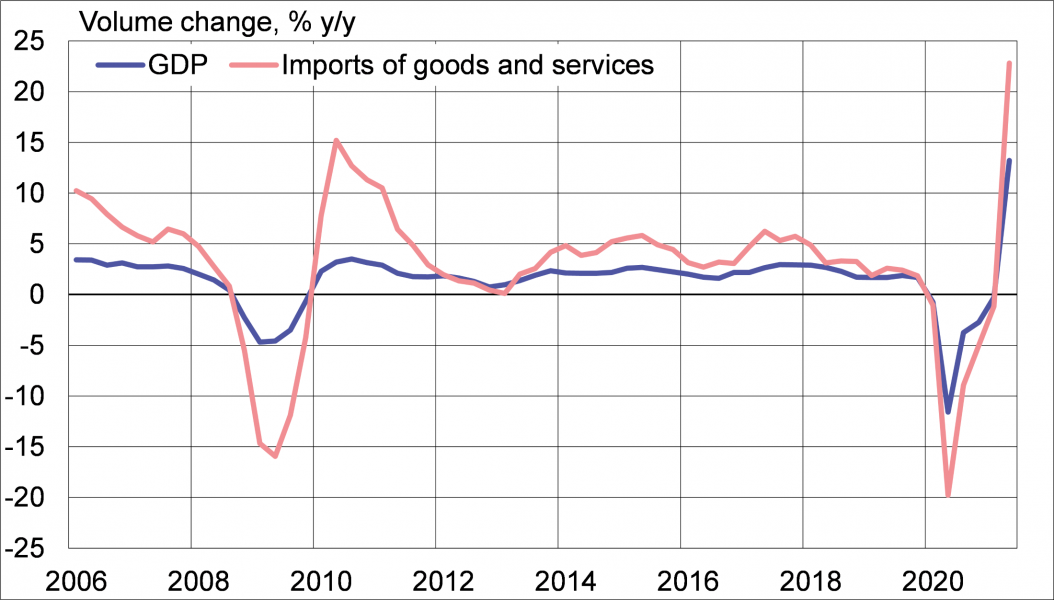

The global economy and global trade flows have been hit hard by the COVID-19 crisis. The trade collapse of 2Q20 was even more severe than during the trough of the global financial crisis (GFC) in 2009. However, taking into account the substantial fall in the GDP of most countries during the COVID-19 crisis, the relative trade contraction seems milder compared with the GFC. During the GFC, the combined volume of the GDP of OECD countries contracted by about 5%, and the combined volume of imports of goods and services by 17% from peak to trough (Figure 1). The corresponding figures for the COVID-19 crisis were -12% and -20%, respectively. Trade has also recovered rapidly since the trough in 2Q20. Pre-crisis levels were almost back by the end of the year.

Figure 1. Annual change in the quarterly GDP and imports in OECD countries, %

Source: OECD.

To shed light on potential factors that may explain this development, Simola (2021) examines the role of demand side factors in the COVID-19 trade collapse and the GFC. These include demand elasticity of imports, the structure of expenditure changes and the role of service sector demand. The analysis is based on a traditional import regression, where the change in the volume of goods and services imports is explained by a measure of import-intensity-adjusted demand and import prices. The import-intensity-adjusted demand measure developed by Bussiere et al. (2013) takes into account the varying share of imports in different demand components and thus tracks import demand developments more accurately than GDP.

The import regression is estimated for 40 advanced and emerging economies using quarterly data from 1995 to 2020. The estimation results are applied to examine and compare the trade collapses and following recoveries in 2009 and 2020, focusing on the role of expenditure changes in explaining the trade developments during the crises. To take into account the role of service sector demand in the trade collapse, a novel import-intensity-adjusted demand measure is constructed in a similar manner for demand from main production sectors.

A simple explanation for the relatively mild trade collapse could be a decline in the global demand elasticity of trade after the GFC. Simola (2021) cannot, however, find support for this hypothesis either for advanced or for emerging economies. This is in line with the results of several previous studies (e.g. Aslam et al., 2018; Auboin & Borino, 2017; Timmer et al., 2021) finding that the demand elasticity has not declined in past decades, although there are also some contradicting results (Constatinescu et al., 2020; Martin-Martinez, 2016).

Another factor behind the relatively milder trade collapse could lie in the structure of demand changes. The literature suggests that compositional effects associated with changes in final expenditure explain most of the contraction in trade during the GFC (Baldwin, 2009; Bems et al., 2013). The findings of Simola (2021) imply that demand factors indeed played a key role also in the COVID-19-induced trade collapse. Import-intensity-adjusted demand explained an even larger share of the import contraction than during the GFC.

There is much variation across countries regarding the main contributing component. In most countries, the decline was either clearly consumption-led (e.g. Chile and the UK) or export-led (e.g. Korea and Hungary). The contribution of domestic demand components, particularly consumption, is higher on average in emerging economies. Correspondingly, the contribution of export demand is larger on average in the advanced economies. This could reflect the massive public sector support measures, particularly in advanced economies, to boost domestic demand. The relatively small sample size of 40 countries makes more detailed statistical analysis on the collapse difficult, but we can make some indicative comparisons.

Indicative comparisons based on correlations suggest that the import decline in the EU countries was much more strongly export-led than in the other countries of the sample. The contribution of exports to import decline also appears to be higher in countries where the share of intermediate inputs in imports is higher (e.g. Korea and Czech Republic). In contrast, the contribution of exports tends to be smaller in countries that export more raw materials (e.g. Norway and Russia), as the import content of raw material exports is typically very low. The import decline seems to have been more strongly consumption-led in those countries that have imposed stricter restrictive measures to contain COVID-19. In addition, stronger government support measures could be associated with less investment-led import decline.

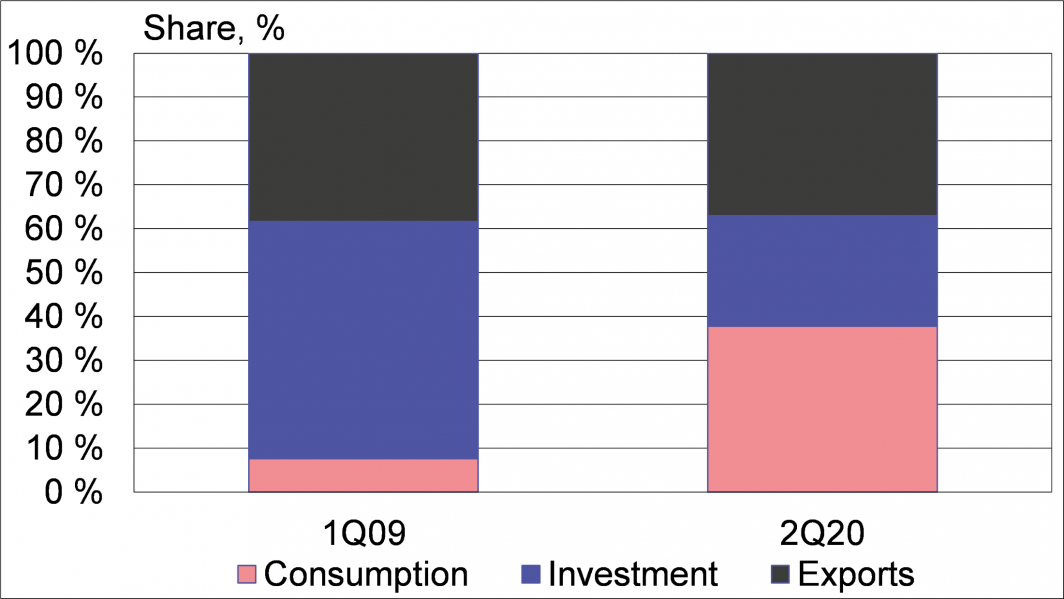

The compositional effect of demand changes was, however, very different during the COVID-19 crisis and the GFC. The trade collapse in 2020 was in most countries led by decline in import demand for consumption, while in 2009 it was much more strongly associated with a decline in import demand for investment (Figure 2a). Decomposing the total demand effect shows that in 2020 the average contribution of consumption demand to the import collapse was 38%, while it was only 6% in 2009. In contrast, the contribution of investment demand was 25% in 2020 compared with 55% in 2009. The trends are similar across advanced and emerging economies, although in emerging economies the import decline was even more pronouncedly consumption-led during the COVID-19 crisis. Consumption is typically less import-intensive than investment. Thus, the relatively milder import contraction during the COVID-19 crisis is compatible with the decline in demand when adjusted for import intensity.

The recovery paths of trade have also been different following the two crises. During the COVID-19 crisis, the import recovery has been faster overall in our sample countries, but also more heterogeneous than during the GFC. In 4Q09, the average level of imports was only 5% higher compared with the trough of 1Q09. In 4Q20, it was already 16% higher compared with the trough of 2Q20. In general, the in-sample predictions based on import-intensity-adjusted demand are relatively close to the realized outcomes after both crises. For most countries, the predictions would have suggested an even slightly faster recovery in imports during the COVID-19 crisis than was realized. In contrast, during the GFC the predictions tended to underestimate the recovery in imports. This could imply that supply factors have restricted the recovery more during the current crisis than during the GFC.

The picture of the COVID-19 trade collapse can be further complemented with analysis on demand component effects arising from the production structure of the economy. Final demand in manufacturing and primary sectors is typically more heavily oriented to imports than final demand in the service sector and construction. The current crisis has hit the service sector particularly hard with the strict restrictions imposed e.g. on the gathering and movement of people. This could also be reflected in the milder contraction in trade than in GDP, as service sector demand is less import-intense. To examine this issue, Simola (2021) applies an import-intensity-adjusted demand measure that takes into account the import intensity of the main production sectors (agriculture, industry other than manufacturing, manufacturing, construction and services).

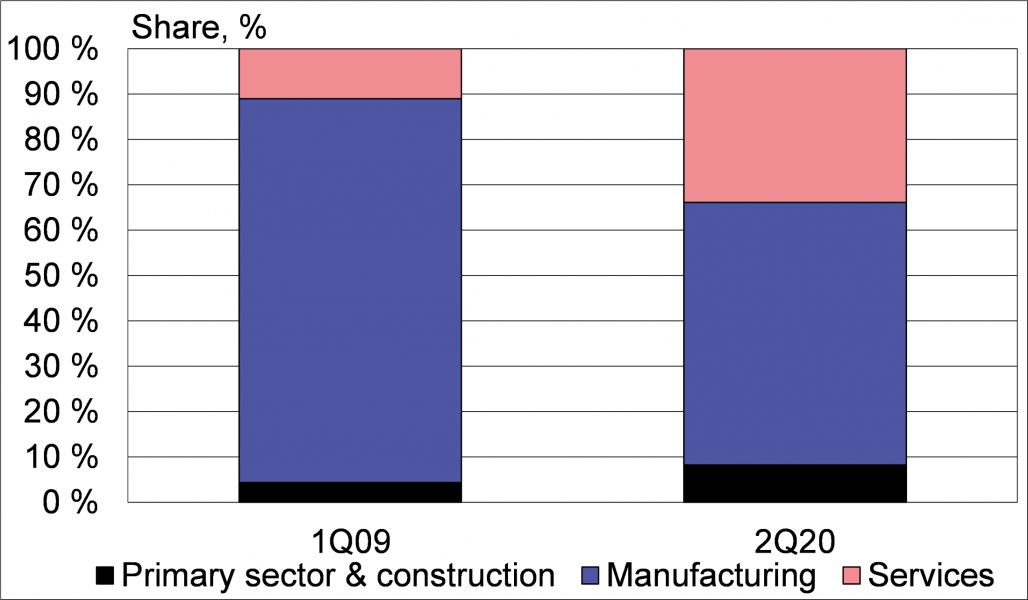

Decomposing the import decline during the crisis into sector contributions once again shows interesting differences between the COVID-19 crisis and the GFC. Although the manufacturing sector accounted for the majority (58%) of the import decline in 2020, the service sector also made a significant contribution of 34% (Figure 2b). The contribution of the manufacturing sector was nevertheless still notably higher (85%) in the import collapse of 2009, while the role of the service sector was correspondingly much smaller, at 11%. This picture is similar for both advanced and emerging economies, but the contribution of the service sector is higher for advanced economies. This highlights the unique nature of the COVID-19 crisis compared with previous crises in its strong focus on the service sectors. It could also be a factor behind the relatively mild trade contraction relative to GDP during the current crisis.

Figure 2. Average contributions of a) demand components and b) aggregate production sector demand in the import decline in 1Q09 and 2Q20

|

|

Note: The shares represent (unweighted) averages calculated across the countries in the sample and normalized to sum up to 100. Source: Simola (2021).

While the trade collapse during the COVID-19 crisis was stunning in its magnitude, in relative terms it was actually milder than during the GFC. The simplest explanation – decline in demand elasticity of trade – appears not to be the most adequate. Instead, compositional effects associated with changes in final expenditure were a key factor also in the COVID-19 crisis, as during the GFC. The contribution of demand from consumption and the service sector in the trade collapse was notably larger in 2020 compared with 2009. Consumption and services are less import-intensive than investment or manufacturing. Thus, the relatively milder trade contraction during the COVID-19 crisis than during the GFC could reflect changes in demand composition. Global trade has also recovered much more rapidly from the COVID-19 crisis than from the GFC, supported by the massive fiscal and monetary policy measures that were rapidly introduced across the world.

Aslam, A., Boz, E., Cerutti, E., Poplawski-Ribeiro, M. and Topalova, P. (2018). The slowdown in global trade: A symptom of a weak recovery? IMF Economic Review, 66(3), 440–479.

Auboin, M. & Borino, F. (2017). The falling elasticity of global trade to economic activity: Testing the demand channel. WTO Working Paper ERSD-2017-09, April 2017.

Baldwin, R., ed. (2009). The great trade collapse: causes, consequences and prospects. VoxEU Report. Centre for Economic Policy Research, November 2009.

Bems, R., Johnson, R. C. and Yi, K.-M. (2011). Vertical Linkages and the Collapse of Global Trade. American Economic Review, 101(3), 308–312.

Bussiere, M., Callegari, G., Ghironi, F., Sestieri, G. and Yamano, N. (2013). Estimating Trade Elasticities: Demand Composition and the Trade Collapse of 2008-2009. American Economic Journal: Macroeconomics, 5(3), 118–51.

Constantinescu, C., Mattoo, A. and Ruta, M. (2020). The Global Trade Slowdown: Cyclical or Structural? World Bank Economic Review, 34(1), 121–142.

Martinez-Martin, J. (2016). Breaking down world trade elasticities: A panel ECM approach. Bank of Spain Working Paper No. 1614.

Simola, H. (2021). Trade collapse during the COVID-19 crisis and the role of demand composition. BOFIT Discussion Paper 12/2021.

Timmer, M. P., Los, B., Stehrer, R. and de Vries, G. J. (2021). Supply Chain Fragmentation and the Global Trade Elasticity: A New Accounting Framework. IMF Economic Review (2021).

Heli Simola, Senior Economist, Bank of Finland Institute for Emerging Economies (BOFIT), heli.simola@bof.fi.