Digital technologies are often seen as a potential vector for the third industrial revolution. This policy brief exploits a unique survey by the Banque de France to measure firms’ digitalisation and determine its potential impact on productivity. The use of technologies, which has been stimulated by the covid-19 crisis, could facilitate and reinforce the economic rebound.

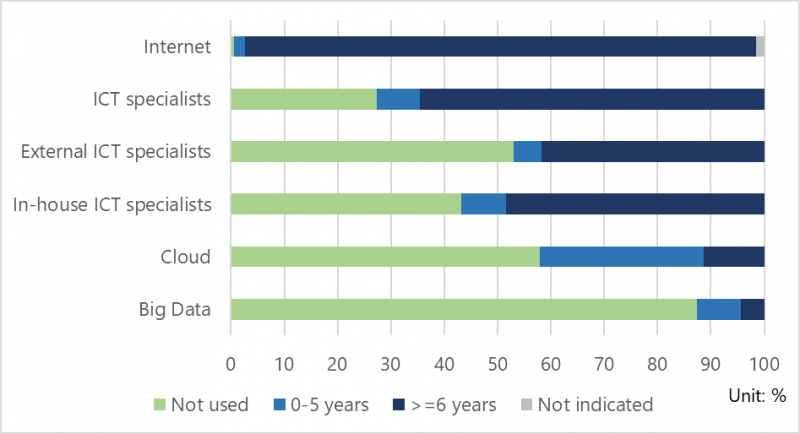

Chart 1: Use of ICTs and digital technologies in manufacturing in 2018

Sources: Survey of factor utilisation degrees and FIBEN (Banque de France).

Scope: Firms for which at least one establishment belongs to the manufacturing sector and with at least 20 employees.

Key: 58% of firms do not use the cloud at all, 31% have used it for less than 5 years and 11% have used it for more than 5 years.

Over the last decades, productivity growth has declined in most developed countries, regardless of their distance to the technological frontier. If this trend were to continue, such low productivity gains would make it very difficult to tackle the serious headwinds we currently face: population ageing, the sustainability of our healthcare systems, rising inequalities, environmental risks or the increase in public debt.

Digitalisation is often seen as the potential source of a huge and possibly long productivity revival that would enable us to address these challenges. However, paradoxically, this productivity revival induced by digitalisation is taking a long time to make itself felt. According to Van Ark (2016), “the New Digital Economy is still in its ‘installation phase’ and productivity effects may only occur once the technology enters the ‘deployment phase’”.

National strategies of repeated lockdowns will clearly foster greater digitalisation among firms. By way of example, according to the November Survey of SME Cash Levels, Investment and Growth (Bpifrance Rexecode), 50% of business leaders questioned about their medium-term strategy “indicated that they had begun steps to digitalise their company, focusing first on the organisation of their relationships with customers, and 20% planned to take such steps in the short to medium term but had not yet done so.” But what do we know about French firms’ use of digital technologies? How can it be expected to impact productivity?

The Banque de France carries out an annual survey of manufacturing firms with at least 20 employees, in order to collect information on their use of production factors. As part of each survey, it also gathers information on specific topics of interest. In 2018, firms were asked whether they used the internet (since when and with what type of internet connection), and whether they employed Information and Communication Technology (ICT) specialists (external or in-house) or used digital technologies (cloud and big data). To the best of our knowledge, this Banque de France survey, alongside INSEE’s ICT survey, is one of the few sources of data on firms’ use of digital technology in France.

The results of this survey show that use of digital technologies is:

i) still fairly limited (Chart 1): while the majority of the 1,065 firms surveyed said they used the internet, and 65% said they had employed ICT specialists (external or in-house) for 5 years or more, only 42% said they used the cloud (nearly a third for less than 5 years). In addition, 13% said they carried out big data analyses and had generally done so for less than 5 years.

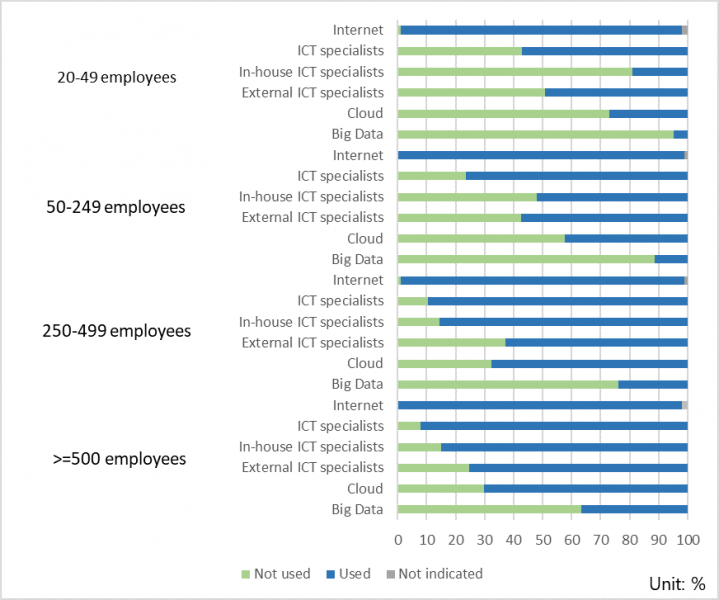

ii) highly concentrated among the largest firms (Chart 2): the use of ICT staff and digital technologies tends to increase with the size of the firm. While only 28% of firms with between 20 and 49 employees use the cloud, this rises to 70% for firms with between 250 and 499 employees. In the case of big data, nearly 40% of firms with at least 500 employees said they used it, while the figure was just 10% for SMEs. The existence of a positive correlation between firm size and demand for ICT is also documented extensively by Lashkari et al. (2019) with regard to French firms’ investment in IT hardware and software.

Chart 2: Use of ICT and digital technologies by firm size in 2018

Unit: %

Sources: Survey of factor utilisation degrees and FIBEN (Banque de France).

Scope: Firms for which at least one establishment belongs to the manufacturing sector and with at least 20 employees.

Key: 73% of firms with 20-49 employees do not use the cloud at all, while 27% do use the cloud.

These stylised facts raise two questions: do firms become more productive because they use ICT and digital technologies? Or do they adopt these technologies because they are already more productive? This is the challenge and difficulty posed by empirical studies of the subject.

An abundant literature has been devoted in the last decades to quantifying the impact of ICT on productivity. However, few papers have focused on the impact of digitalisation on productivity, and those that do mainly concern specific digital technologies such as broadband access. On this latter topic, Akerman et al. (2015) find that broadband access has a positive impact on labour productivity and wages at the firm level in Norway. Similarly, Malgouyres et al. (2019) demonstrate that the roll-out of broadband had a positive impact on French firms’ imports at the start of the 2000s, and suggest that a corollary of this could be an increase in productivity.

By exploiting data from the Banque de France survey described above, Cette et al. (2021) also conclude that digital technologies have a potentially strong impact on French firms’ productivity: all other things being equal, the employment of ICT specialists (in-house and external) and use of digital technologies (cloud and big data) are found to increase labour productivity and total factor productivity by 23% and 17% respectively compared with firms that do not use such technologies.

If confirmed by other firm-level studies, these results would suggest that the use of digital technologies and ICT could be an essential vector for a third industrial and technological revolution. These technologies could contribute strongly to an economic rebound after the Covid-19 crisis, which has stimulated their use.

This article was first published in Banque de France‘s Eco Notepad as blog post n°194.