We investigate a phenomenon we refer to as carbon home bias: the tendency of investors to overallocate investment towards relatively dirty firms in their home market. Based on our work – Boermans and Galema (2023) – we show that carbon home bias is significant in the euro area: domestic stocks account for 50% of investors’ total portfolio carbon footprint. Although European investors are decarbonizing their portfolios, they mainly do so through their foreign investments. We investigate why we might observe carbon home bias and find that active engagement is a potential explanation, whereas we find no evidence that differential carbon premia might be driving carbon home bias. Finally, we provide a list of policy implications based on our results elucidating why carbon home bias is important.

European investors are increasingly concerned with climate-related risks associated with their investment portfolios. To mitigate their exposure to these risks, investors can either divest from companies with high climate risk exposure or actively engage with companies to encourage them to reduce their emissions. ABP, a prominent Dutch pension fund and one of the largest institutional investors globally with assets under management amounting to EUR 552 billion, for years pursued an engagement strategy with oil companies, notably maintaining substantial positions in Royal Dutch Shell. They argued that actively engaging with Shell would ultimately yield better results than divesting. However, after pressures from stakeholders in 2022, ABP acknowledged its engagement strategy did not sufficiently accelerate the energy transition at Shell and it completed a full divestment from Shell and fossil fuels by early 2023.1

The experience of ABP’s continued investment in Shell first begs the question to what extent investors in general tend to hold on to especially the carbon-intensive assets in their home market, which is what we define as “carbon home bias” in our recent contribution (Boermans and Galema, 2023). In our paper we first document the extent of carbon home bias and show its relation to the general trend of investors decarbonizing their portfolios. Second, we try to better understand why we might observe carbon home bias. Is it conducive to investors’ active engagement strategies or might there be alternative explanations that are consistent with carbon home bias?

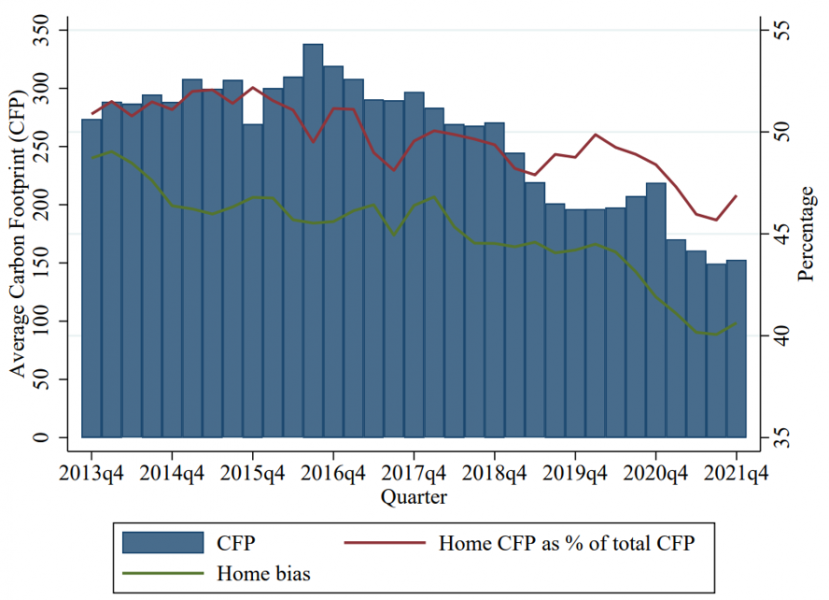

Figure 1 illustrates the decarbonization of European investors portfolios. The bar graph shows the carbon footprint, which is portfolio weighted average of carbon emission scaled by sales, averaged each quarter. Figure 1 shows that especially in recent years European investors have significantly reduced their carbon footprints. Concurrently, the level of home bias among European investors has also declined, reaching approximately 40% in 2021. However, notable carbon home bias persists among European investors, with around 45% to 50% of their portfolio’s carbon footprint attributed to domestic market stocks. This carbon home bias consistently exceeds the level of home bias.

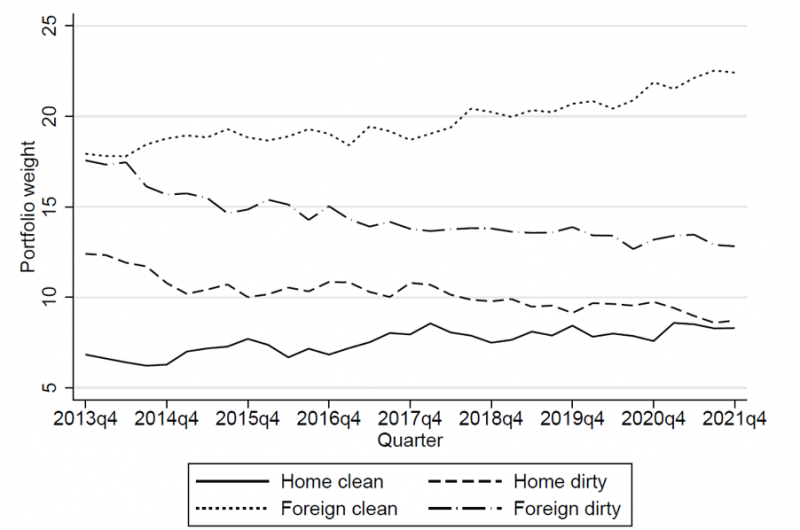

Investors can decarbonize by shifting their portfolios away from carbon-intensive stocks and towards clean stocks. They can do so for their domestic holdings, their foreign holdings or both. To assess their relative contributions, we split investor holdings in the 25% cleanest and 25% dirtiest stocks and calculate the aggregate weights of investors by holder country-sector in four subportfolios: Home clean, Home dirty, Foreign clean, and Foreign dirty. Figure 2 illustrates that European investors are actively decarbonizing both their foreign and domestic portfolios, but this trend is most pronounced in the foreign portfolios. There is a substantial increase in the allocation to Foreign clean stocks, coupled with a significant decrease in Foreign dirty stocks. While there is a slight uptick in the Home clean allocation, Home dirty holdings remain relatively stable over time, hovering around 10% for a significant portion of the sample period. This suggests that carbon home bias exhibits a notable level of persistence over time. Therefore, European investors primarily achieve decarbonization by shifting their portfolios away from dirty foreign firms and towards cleaner foreign firms (and, to a lesser extent, cleaner domestic firms).

Figure 1: Carbon footprint and (carbon) home bias

Figure 2: Carbon footprint adjustments through portfolio tilting

Like the anecdote of the Dutch pension fund ABP remaining invested in Royal Dutch Shell for a long time, investors might prefer to focus their active engagement (Dyck et al., 2019; Krueger et al., 2020; Gillan et al., 2021) on their domestic holdings. Due to costs of influencing, investors are forced to limit their engagement activities to a select number of firms. Empirical evidence shows that investors are more inclined to engage with domestic firms (Dimson et al., 2021; Dasgupta et al., 2023). To decarbonize investment portfolios, investors might therefore use a combined strategy of active engagement with firms that are easier to influence (i.e. domestic firms), whereas divesting firms that are more difficult to impact (i.e. foreign firms).

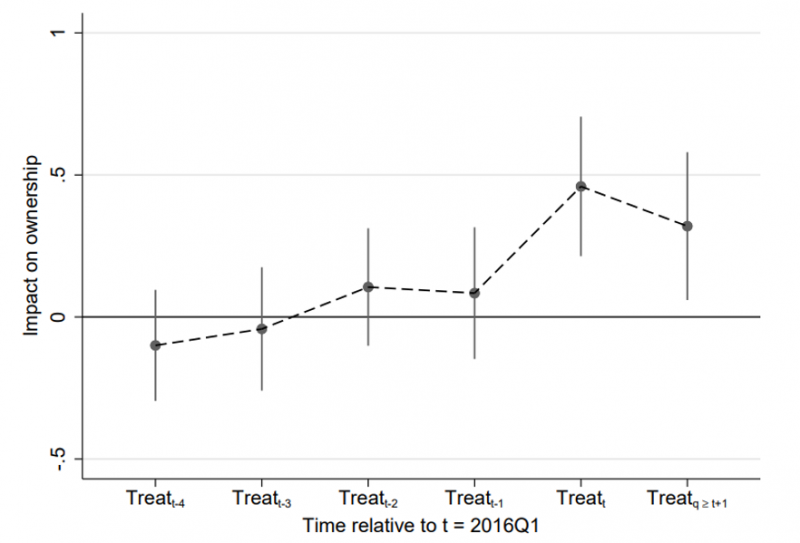

Figure 3: Dynamic effect of treatment estimates

To identify and separate these effects, we exploit the effects of the French carbon disclosure Article 173, which mandates institutional investors to measure and publicly disclose the carbon footprint related to their portfolio investments. This arguably is an exogenous shock to investors’ propensity to decarbonize, that allows us to identify how they subsequently adjust their portfolios. Figure 3 shows the impact of this shock on ownership. Consistent with our hypothesis, we show that the French carbon disclosure Article 173 is linked to significantly higher institutional ownership of carbon-intensive domestic stocks post-Article 173, whereas we do not observe any impact pre-Article 173. In additional differences-in-differences analyses, we show that for foreign stocks the opposite holds, i.e. a lower institutional ownership of carbon-intensive assets post-Article 173. So a shock urging investors to decarbonize their portfolios, results in increased domestic carbon-intensive holdings but decreased foreign carbon intensive holdings.

To provide further evidence for the active ownership of domestic firms, we use the same Article 173 shock to investigate its subsequent impact on carbon emissions and disclosure. We show domestic active engagement is successful: ex post French firms with high French institutional ownership ex ante, subsequently reduce their carbon emissions, whereas this does not hold for foreign firms. They are also more likely to report emissions, but only when institutional ownership is sufficiently large.

Finally, we also consider an alternative explanation for carbon home bias: Investors might invest in dirty domestic firms to earn a domestic carbon risk premium (Bolton and Kacperczyk, 2021), which may exceed the carbon premium they earn on foreign stocks. This could be due to investors possessing country- or industry-specific informational advantages concerning domestic polluting industries (Van Nieuwerburgh and Veldkamp, 2009; Schumacher, 2017). However, we find no evidence of differential carbon premia. If anything, we only find a carbon premium on investors’ foreign holdings which is opposite of what would be needed to be consistent with carbon home bias.

Activist and stakeholders have urged institutional investors to divest from their carbon-intensive assets. If large groups of investors would completely divest from carbon intensive firms, this would increase their cost of capital. However, currently there are likely enough investors willing to hold the complement of sustainable investors, such that the impact of carbon divestment on the cost of capital might be small (Berk and van Binsbergen, 2021). If so, active engagement is likely to be a good alternative and advises to do exactly the opposite: Instead of divesting carbon-intensive assets, investors that want to actively engage need to have a sufficient stake in dirty firms to convince them to become cleaner. Our results suggest that this might be more effective for domestic firms, which offers a justification for the substantial carbon home bias we observe – even though engagement might not always be effective.

High exposures to domestic carbon-intensive firms could however come at a risk. With substantial carbon home bias and domestic firms that are impacted by more stringent carbon regulation, investors are potentially hit twice: once via their domestic economies and once via their investment positions. Moreover, active ownership of domestic carbon-intensive assets can also go the other way. More financially oriented investors may be inclined to stall progress towards costly investments in cleaner domestic production, and concentrated financial interests in domestic industries could lead to lobbying to prevent more stringent domestic carbon regulations. So, carbon home bias offers opportunities for effective active ownership, although concentration also poses risks.

Berk, J., & van Binsbergen, J. H. (2021). The impact of impact investing. Mimeo.

Boermans, M. A., & Galema, R. (2019). Are pension funds actively decarbonizing their portfolios? Ecological Economics, 161, 50-60.

Boermans and Galema (2023). Carbon home bias of European investors. DNB Working Paper No 786.

Bolton, P., & Kacperczyk, M. (2021). Do investors care about carbon risk?. Journal of Financial Economics, 142(2), 517-549.

Dasgupta, S., Huynh, T., & Xia, Y. (2023). Joining forces: The spillover effects of EPA enforcement actions and the role of socially responsible investors. Review of Financial Studies, Forthcoming.

Dimson, E., Karakaş, O., & Li, X. (2021). Coordinated engagements. Mimeo.

Dyck, A., Lins, K. V., Roth, L., & Wagner, H. F. (2019). Do institutional investors drive corporate social responsibility? International evidence. Journal of Financial Economics, 131(3), 693-714.

Gillan, S. L., Koch, A., & Starks, L. T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66, 101889.

Krueger, P., Sautner, Z., & Starks, L. T. (2020). The importance of climate risks for institutional investors. Review of Financial Studies, 33(3), 1067-1111.

Schumacher, D. (2018). Home bias abroad: Domestic industries and foreign portfolio choice. Review of Financial Studies, 31(5), 1654-1706.

Van Nieuwerburgh, S., & Veldkamp, L. (2009). Information immobility and the home bias puzzle. Journal of Finance, 64(3), 1187-1215.

Boermans and Galema (2019) show that Dutch pension funds were actively decarbonizing their portfolios over the period 2009-2017, however, they did so mainly by divesting from carbon-intensive industries.