The views expressed in this brief are solely those of the author and do not necessarily reflect the positions of institutions to which he is affiliated.

In this brief we present the results of a novel framework for the financial assessment of different types of common sovereign debt instruments in the euro area. The instruments under analysis include full and partial mutualisation of sovereign risk, as well as the pooling and tranching of national government debt without mutualisation. The results show that full risk mutualisation can lower financing costs for all participating countries, and that “Eurobonds” would have weathered well the European sovereign debt crisis, even if partial mutualisation remains the most attractive option for the most creditworthy countries. Options involving just the tranching and pooling of Member State debt simply reallocate sovereign risk across instruments, although the “E-Bonds” proposal can approximate the characteristics of mutualised “Blue Bonds” under certain conditions. We conclude by comparing theoretical proposals with the actual experience of large-scale EU issuance under the NGEU and SURE programmes.

The question of joint sovereign debt issuance has been a longstanding one on the minds of the policymakers and architects of the European economic and monetary union. Its possible drawbacks have been recognised early on, notably the fact that it may call for a high level of political and economic integration, around which there may be no consensus. This is particularly true where a common debt instrument involves mutualisation and risk sharing across borders, which could require enhanced mechanisms for containing moral hazard issues linked to excessive debt issuance by a Member State. Concerns about such issues lead to the prohibition of debt mutualisation in the Maastricht Treaty of 1992.

Over the years, however, several advantages have also began to be ascribed to common debt instruments in a currency union such as the euro area, including their ability to: i) break the “diabolic” sovereign-bank loop; ii) finance joint EU projects; iii) bolster the international role of the euro; iv) deepen capital markets; v) and expand the supply of “safe assets”, the relative scarcity of which has been recognized as impairing macroeconomic functioning.1

In addition, from a financial viewpoint, the pooling together of imperfectly-correlated sovereign risk can also potentially lower credit risk premia and financing costs for participating governments, with positive spill-over effects for the private sector and the wider economy. A discussion of the credit risk premia of different types of common debt instruments – as well as the conditions under which these instruments can achieve risk diversification in a manner not already available to market participants – is the focus of this policy brief. In fact, while the interest rate savings or costs associated with different instruments are a matter of relevance on their own, they are also intimately linked to political economy considerations surrounding the common EU issuance debate, given concerns of subsidisation of higher-yield Member States by more creditworthy countries.

Several proposals have been put forward over time as to how EU Member States could jointly issue sovereign debt. These have included fully mutualised instruments, as when a canonical “Eurobond” jointly guaranteed by all participating Member States would finance all of national government debt, and partly mutualised options, such as the “Blue Bond” proposal,2 whereby joint guarantees would extend only to senior sovereign debt worth up to 60% GDP, beyond which limit Member States would have to issue junior “Red Bonds” on their own.

Other proposals have focused on non-mutualised instruments, such as “ESBies”,3 which can be constructed by acquiring a portion of outstanding sovereign bonds and tranching this pool a posteriori into a senior part (the ESBie) and a junior one (the EJBie). Alternatively, sovereign debt can also be tranched a priori, at the time of issuance in primary markets, creating a senior “E-bond”,4 which would coexist with junior national bonds.

The expanding literature on common sovereign debt instruments lacks, however, an integrated framework that can simultaneously analyse and compare the risk properties of all these different options. While much progress has been made regarding instruments that do not involve mutualisation, the properties of fully and partly guaranteed instruments remain essentially unquantified.

In Monteiro (2023), I introduce an integrated framework to assess the credit risk of a wide range of common debt instruments, including mutualised options. The approach is based on the notion that, when read in conjunction with expected debt levels, a market assessment of a sovereign’s debt capacity can be inferred from market data, such as CDS spreads or bond yields, using state-space methods. These national debt capacities change over time and, crucially, are not perfectly correlated, meaning that there is scope to diversify away idiosyncratic risks. Once inferred, the set of national debt capacities can be used to simulate the counterfactual performance of different types of instruments. For instance, under a fully credible Eurobond, national debt capacities are pooled together and compared against pooled national debt, assuming that mechanisms exist whereby debt capacity can be transferred across Member States, if needed. The probability of default is then that of aggregate debt capacity falling below aggregate debt levels at some point in the future.

When interpreting the results of the analysis, it is important to bear in mind its partial equilibrium nature and a ceteris paribus assumption governing moral hazard issues. That is, the focus is on counterfactual credit risk premia, and broader macroeconomic implications of introducing a common safe asset are not considered.5 Moral hazard and government debt issuance are thus assumed to remain unchanged with respect to the historical baseline, while they could either tend to increase (Eurobonds) or decrease (Blue Bonds/Red Bonds and E-bonds).

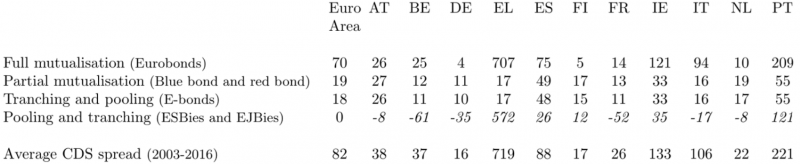

We focus on the years running from the early days of the euro area up to the post-sovereign debt crisis period, when quantitative easing was already at play. The sample period includes therefore a veritable stress test of the different debt instruments by covering the critical years from 2009 to 2013. Table 1 provides an overview of the results: it shows, for each Member State and for each instrument, the counterfactual gains and losses in terms of changes in average credit risk premia, to be discussed in the following sections.

Table 1: Average risk premium savings (+) and losses (-) per common debt instrument

(basis points, January 2003 to April 2016)

Note: the euro area figures refer to the total gains accruing to the euro area aggregate composed of the 11 Member States considered in the simulations. The cut-off level of the senior tranches was set at 60% of GDP, where applicable. Gains under tranching and pooling are realisable only under a sequential default assumption. The national figures in italics shown under pooling and tranching are the gains and losses of a hypothetical common debt agency associated with transacting different sovereign bonds in the market. From the viewpoint of Member States, this option has a neutral impact.

It can be observed from Table 1 that Eurobonds are the instrument that provide, by far, the largest gains for the euro area aggregate, lowering its average risk premium by 70 basis points in the counterfactual simulations.6 This is because they allow for i) the full diversification of idiosyncratic risk and ii) the bringing together of different safety buffers, in the form of different fiscal spaces. The result that the whole of euro area debt can theoretically be turned into a true safe asset with negligible risk premia should not be surprising. The euro area is a large, rich and diversified economy, with an aggregate debt ratio that compares favourably with that of other advanced economies.7 That it can potentially match the quality of the best existing international safe assets is something to be expected.

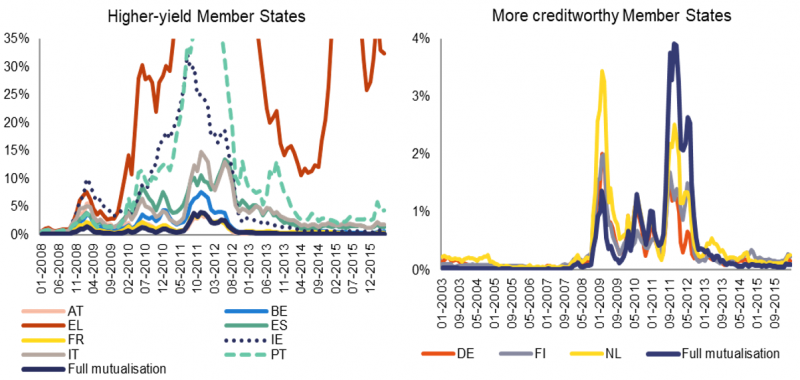

A perhaps less anticipated result is that Eurobonds can deliver gains for all Member States in the long run, not just for the less creditworthy sovereigns, where gains are largest. This is observable in Figure 1, where a counterfactual Eurobond is seen to have weathered the sovereign debt crisis relatively well. It is true that the most creditworthy countries would have somewhat overperformed Eurobonds during a few months, in times of acute market stress. Over the long haul, however, Eurobonds can provide modest gains even for this set of countries.

Figure 1: Probabilities of default: historical vs. full mutualisation counterfactual

Note: Two-year probabilities of default. Vertical axis of the left-hand chart truncated for visualisation purposes, given the outlier dynamics of EL.

Partly-mutualised Blue Bonds deliver the second highest gains for the euro area aggregate. In this case, only senior sovereign debt up to 60% of GDP is mutualised. Any amounts beyond that threshold are considered junior debt and are subject to the credit risk of the issuing Member State. The Blue Bond proposal was first made by Delpla and Weizsäcker (2010) and requires particular consideration. Its main source of appeal lies in combining mutualisation with the possibility of maintaining market discipline through the junior Red Bonds, which command a heightened risk premium,8 thereby providing incentives for Member States to keep debt-to-GDP within the 60% Maastricht reference figure. In Monteiro (2023), I introduce a novel mathematical framework that formalises the proposal and allows for its quantification.

A relevant result worth noting at this point is that different Member States prefer different levels of mutualisation. While full mutualisation delivers the biggest benefit for higher-yield Member States, the more creditworthy countries stand to benefit the most from high, but incomplete, levels of mutualisation. This is a consequence of the existence of the junior Red Bonds in the Blue Bonds proposal, which absorb excessive national risk.

Non-mutualised common debt instruments have the appeal of potentially producing a safe asset while sidestepping political concerns surrounding risk sharing. However, they cannot in principle generate risk premia gains at aggregate euro area level. Due to their financial engineering nature, these instruments tend to simply displace existing credit risk when analysed in a partial equilibrium context. This does not mean, however, that they cannot generate net gains in a broader macroeconomic context as they may still be able to help deliver the multifaceted advantages of a common debt instrument listed in the introduction to this brief.

Focusing on the results for E-bonds in Table 1, it can be seen that they can potentially deliver gains that approach those of the Blue Bonds proposal. However, these gains are contingent on the assumption that sovereigns only default on senior E-bonds if their debt capacity remains insufficient even after junior bonds have been wiped out. This assumption tends to lower the loss given default (LGD) on total debt outstanding below a conventional 60% figure, thereby reducing overall expected losses, which in turn lowers overall risk premia. If, alternatively, a 60% LGD continues to apply on overall sovereign debt, E-bonds cannot generate gains on aggregate.9

Finally, ESBies are seen to be very safe instruments, even at high volumes such as those produced by the chosen threshold, which was set at 60% of GDP for direct comparison with other options. EJBies can, however, be highly risky as their default probabilities are directly driven by the worst sovereign performers. When taken together, ESBies and EJBies are neutral for Members States and do not generate risk premia gains on aggregate. A European debt agency involved in their construction would make profits from acquiring cheaper sovereign bonds and losses from acquiring more expensive ones, while breaking even overall.

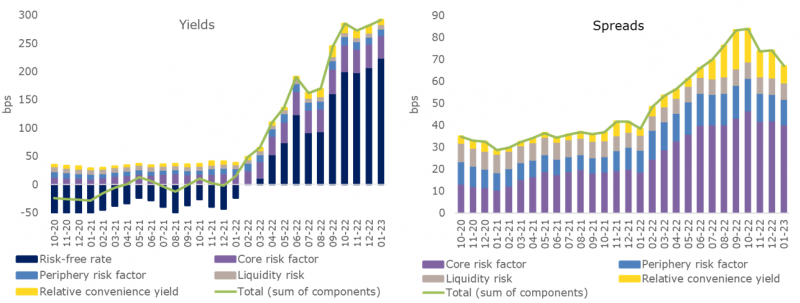

The European response to the covid-19 crisis saw an important institutional breakthrough in the form of large-scale joint debt issuance. Starting in October 2020 with the SURE programme and followed up in June 2021 with the NextGenerationEU (NGEU) programme, EU Member States empowered the European Commission to issue up to € 900 bn in debt markets to fund policies protecting jobs, fostering investment and promoting structural reforms. The market performance of NGEU and SURE bonds was quite positive up until early 2022: an AAA rating; large demand, including from foreign investors; spreads comparable to those of France; and relatively high and increasing market liquidity.10 Throughout 2022, monetary policy normalisation and the Russian war of aggression against Ukraine increased macrofinancial risks, with some repercussions for the performance of EU bonds (defined here as the NGEU, SURE and other bonds issued by the EU as an entity).

While joint issuance under NGEU and SURE is large by historical standards, it is temporary and small when compared with the theoretical proposals reviewed in this brief. It is also different in nature, as the mutualised proposals that we have seen rely on unlimited joint and several guarantees (Eurobonds) or on joint and several guarantees coupled with explicit seniorisation (Blue Bonds), either case implying a very high degree of credit enhancement that has no parallel in existing EU bond issuance.11 A decomposition of the drivers of the yields and spreads of EU bonds illustrates how they are fundamentally exposed to the perceived credit risk of Member States through the loan and budgetary claims of the EU vis-à-vis national governments. Figure 2 summarises the result of an analysis of more than 100 EU bonds tracked over time. It shows how yields on bonds issued by the EU have been driven up since early 2022 by monetary policy normalisation and, to a smaller extent, by increased riskiness in “core” and “periphery” EU countries. The relative convenience yield12 disadvantage of EU bonds is also seen to have edged up temporarily in the second half of 2022, as investors increased their demand for German and other reference sovereign bonds for use in collateral and repo markets.

Figure 2: Main drivers of the average yields and spreads of bonds issued by the EU

Source: based on an update of the methodology described in Monteiro (2022).

Note: yields and spreads in simple average terms, covering all active EU bonds in sample at a given point in time. Spreads are calculated with respect to the yield curve of AAA euro area sovereigns.

In this brief we have looked at different types of common debt instruments and reviewed their credit risk through the lens of a novel analytical framework. We have seen how fully mutualised Eurobonds provide the largest counterfactual benefit in terms of a reduction in funding costs of the euro area aggregate. We have also seen how Blue Bonds deliver the second highest aggregate benefit and how they may be the preferred option for the most creditworthy countries by allowing for high but incomplete levels of mutualisation. Both Eurobonds and Blue Bonds are seen to be attractive options from a financial viewpoint for all Member States, thus allowing for a Pareto movement, subject to the proper handling of moral hazard issues.

Non-mutualised options based on the tranching and pooling of sovereign debt displace credit risk across debt instruments. They tend to be neutral from an overall expected loss perspective, except under the assumption of a change in default behaviour.

The recent experience in large-scale issuance with the temporary NGEU and SURE programmes is different in nature from the theoretical constructs previously proposed in the literature. Still, NGEU provided an important signal of commitment to the European project, which immediately lowered perceived sovereign risk when announced in 2020. A successful implementation of these programmes will help shape views concerning the merits of common issuance to finance pan‑European projects and initiatives.

To conclude, mutualised debt instruments cannot be approached in a naïve manner: they are not weighted averages of the credit risk of the constituent sovereigns. The results explored in this brief highlight a point often missed in the adversarial debate between risk sharing and risk reduction: that risk sharing can be risk reduction, when properly implemented.

Brunnermeier, M. K., S. Langfield, M. Pagano, R. Reis, S. V. Nieuwerburgh, and D. Vayanos (2017), “ESBies: Safety in the Tranches”, Economic Policy, 32, 175–219.

Delpla, J. and J. von Weizsäcker (2010), “The Blue Bond Proposal,” Bruegel Policy Brief.

Caballero, R. J. and E. Farhi (2018), “The Safety Trap,” The Review of Economic Studies, 85, 223–274.

Giudice, G., M. de Manuel, Z. G. Kontolemis, and D. P. Monteiro (2019), “A European Safe Asset to Complement National Government Bonds,” available at SSRN.

Monteiro, D. P. (2022), “The Market Performance of EU Bonds,” Quarterly Report on the Euro Area, 21, 31–42.

Monteiro, D. P. (2023), “Common Sovereign Debt Instruments in the Euro Area”, European Economy Discussion Paper 194, European Commission.

Monteiro, D. P. (2023b), “Macrofinancial Dynamics in a Monetary Union,” European Economy, Discussion Paper 188, European Commission.

See Caballero and Farhi (2018).

See Delpla and Weizsäcker (2010).

See Brunnermeier et al. (2017).

See, e.g., Giudice et al. (2019).

For a general equilibrium simulation of a Eurobond in the particular context of a capital flight, see Monteiro (2023b). Consideration should also be given to the event of an actual national default, which is always disruptive irrespective of the existence of common issuance. For a discussion of this point, see Section 4 of Monteiro (2023).

Results can be compared with the figures in the last row, “average CDS spread”, which provide an upper bound to the maximum realisable gains.

For example, the 2022 general government debt-to-GDP ratio of Japan, the US and the UK was 261%, 121% and 101%, respectively. The same figure was 92% for the euro area.

The heightened risk premium of junior tranches is taken into account in the calculations shown in Table 1 for all instruments involving tranching.

Annex C in Monteiro (2023) further discusses this distinction between a “sequential default” assumption (whereby the senior instrument is preserved unless there is a precipitous drop in debt capacity) and a “simultaneous default” assumption (whereby a 60% LGD is always applied to total debt, implying losses on the senior bond whenever the share of junior bonds is less than 60%).

See Monteiro (2022).

NGEU debt benefits from a credit enhancement in the form of an expansion in the EU’s own resources headroom while SURE loans benefit from a system of voluntary guarantees from Member States.

By convenience yield we denote a security’s price component that reflects the services provided by that security such as the possibility of using it under favourable conditions in collateral and repo markets, or to fulfil regulatory requirements.