Macroprudential FX regulations are bank measures that discriminate based on the currency denomination of an operation, with the main objective of reducing bank exposure to foreign currency risk.

Tobal, M. (2018). Currency mismatch in the banking sector in Latin America and the Caribbean. International Journal of Central Banking, vol.14(1), pages 317-364, January.

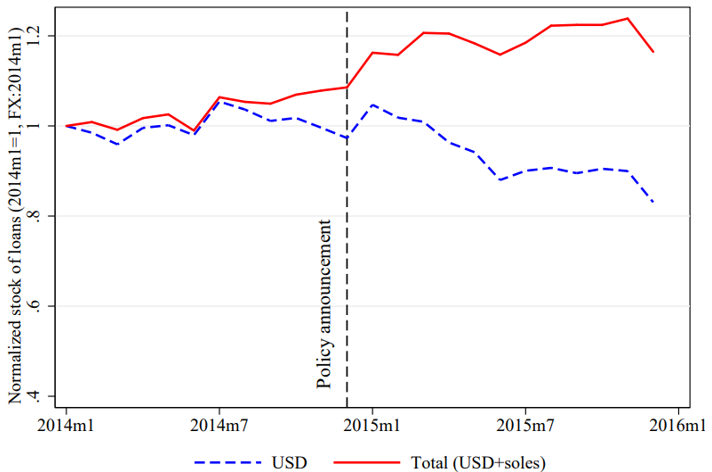

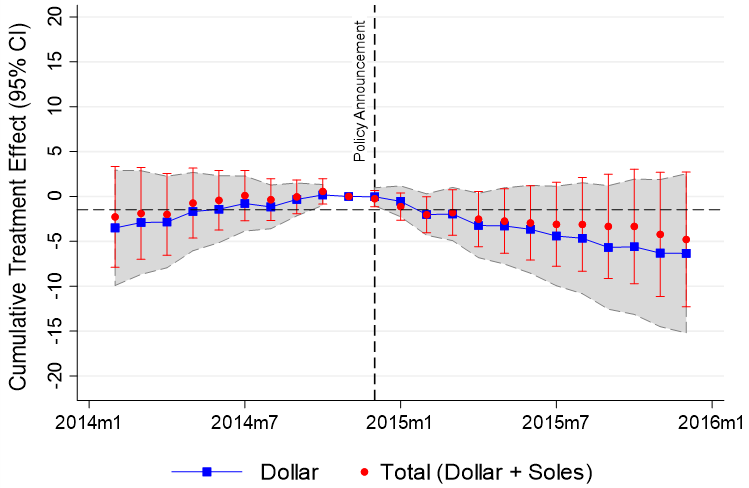

I refer to nontradable firms as those firms not involved in trade activities, that is, non-exporting and non-importing firms.

Bruno and Shin (2015); McCauley, et al. (2015).

Peru, Bulgaria, Croatia, and Romania are four of many examples. (See the IMF 2017 MaP survey).

See Ranciere et al. (2010) for evidence on the relationship between currency mismatch and growth for small firms in emerging countries in Europe.

See for example Ivashina, et al. (2020), DiGiovanni, et al (2020), Salomao and Varela (2022).

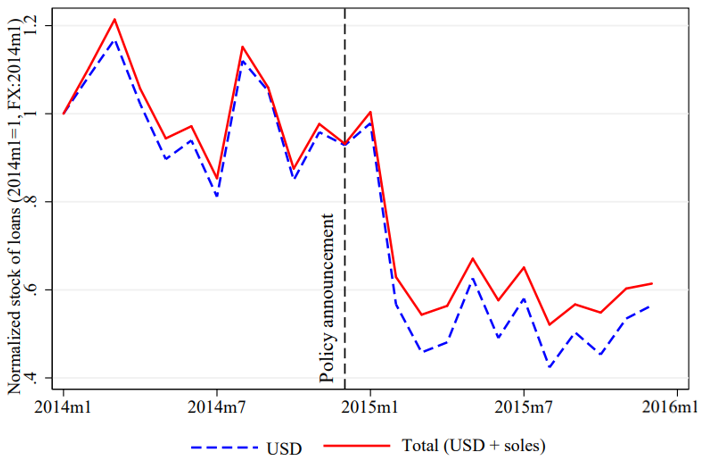

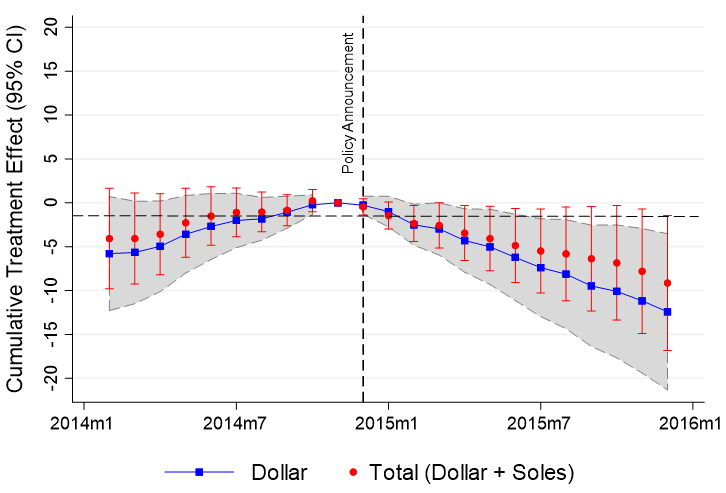

Excluding loans granted to exporters or importers. Excluding loans granted to exporters or importers.

The explanation is on the well documented evidence on banks hedging incentives and the presence of regulatory limits on banks’ FX risk exposure. See Keller (2019) for evidence on Peruvian banks, and Canta et al. (2006) and Tobal (2018) for evidence in emerging economies.