This paper should not be reported as representing the views of the European Central Bank (ECB), the Croatian National Bank or the Eurosystem. The views expressed are those of the authors only.

We propose a new empirical strategy to measure the optimum currency area (OCA) properties for the euro area, with an emphasis on the international business cycle perspective. Building on the measured relative importance of symmetric vs. asymmetric shocks, we obtain a numerical index tracking the degree of optimality of the currency union features over the 20 years of history of the euro area. We argue that the euro area displays stronger OCA properties when the relative importance of common symmetric shocks is high, but, at the same time, is not overly dispersed across euro area member countries. We find that symmetric shocks have been the dominant drivers of business cycles across euro area countries. Our OCA index, however, shows that cyclical convergence among euro area members is not a steady process as it tends to be severely disrupted by crises, especially those not primarily triggered by common external shocks. In the aftermath of a crisis the OCA index embarks on a recovery trajectory catching up with its pre-crisis level. Our OCA index is slow-moving and a good reflection of changing underlying economic structures across the euro area and, in that respect, also informative about the ability of monetary policy to stabilize the euro area economy in the medium run.

The Optimum Currency Area (OCA) theory provides a widely accepted, but rather an illustrative framework to assess under what conditions it would be ideal for a group of economies to form a currency union. It was well known at inception that the euro area did not fully satisfy all the theoretical preconditions of an optimum currency area (OCA) as stated, for example, in Mundell (1961). While expanding further to include Croatia as of 2023, it has not muted the scepticism about its perpetuality. The sustainability of the euro area as a currency union, however, is crucial for the economic, financial and political stability of the region.

There is not a single, consensual way to measure the “optimality conditions” of a monetary union. The theoretical criteria set in the early OCA theory of the 1960s are rather difficult to assess. Later in the 1990s some “empirical” OCA properties were put forward, suggesting that similarity of economic shocks governing economies in a currency union would qualify for a “catch-all” OCA property capturing the interaction between several of these properties. This provides the strategy for considering the concept of “symmetric shocks”, which help business cycles of individual countries synchronize with the aggregate euro area cycle such to enhance the common monetary policy’s potential to stabilize each member country effectively.

The analysis of euro area business cycle drivers can be used to deliver insights on its optimum currency area (OCA) properties. The extent to which the euro area can be considered an OCA depends, inter alia, on the degree to which symmetric shocks impact its regional components (typically countries). Estimating the relative importance (which may change over time) of the symmetric shocks of the euro area business cycle fluctuations thus permits to characterise the evolution of the euro area with respect to its OCA conditions.

Our starting point is an analysis of OCA conditions based on the identification of three underlying business cycle shocks for each euro area country under consideration: common global shocks, shocks of non-global nature but common in the euro area and idiosyncratic country-specific shocks. In the second step, we regroup these three types of shocks into symmetric or asymmetric shocks and construct the OCA index from the importance of symmetric shocks relative to the asymmetric ones.

Country-specific shocks in our analysis cannot affect the rest of the euro area or of the world at any point in time and are by definition all asymmetric. Common shocks may have a symmetric as well as an asymmetric impact on different euro area member states depending on e.g., the economic structures or preferences across the countries. Consequently, asymmetric shocks are defined as including both country-specific (local) shocks and the aforementioned particular type of common shocks.

Relative importance of symmetric shocks for each country is a country-specific measure of net benefits or happiness to be governed by the same monetary policy as the rest of euro area. For example, a shock that affects a country and the rest of the euro area in a similar fashion, i.e., in our analysis “with the same sign” is defined as symmetric from the country’s perspective, irrespective of a possible mixed response among other currency union members. Those countries that react, at the same time, very differently from the rest of the euro area (taken jointly), on the contrary, are hit asymmetrically. In that sense our definition of symmetric shocks departs from a definition where symmetric shock is assumed to affect all the members of a currency union in the same way.

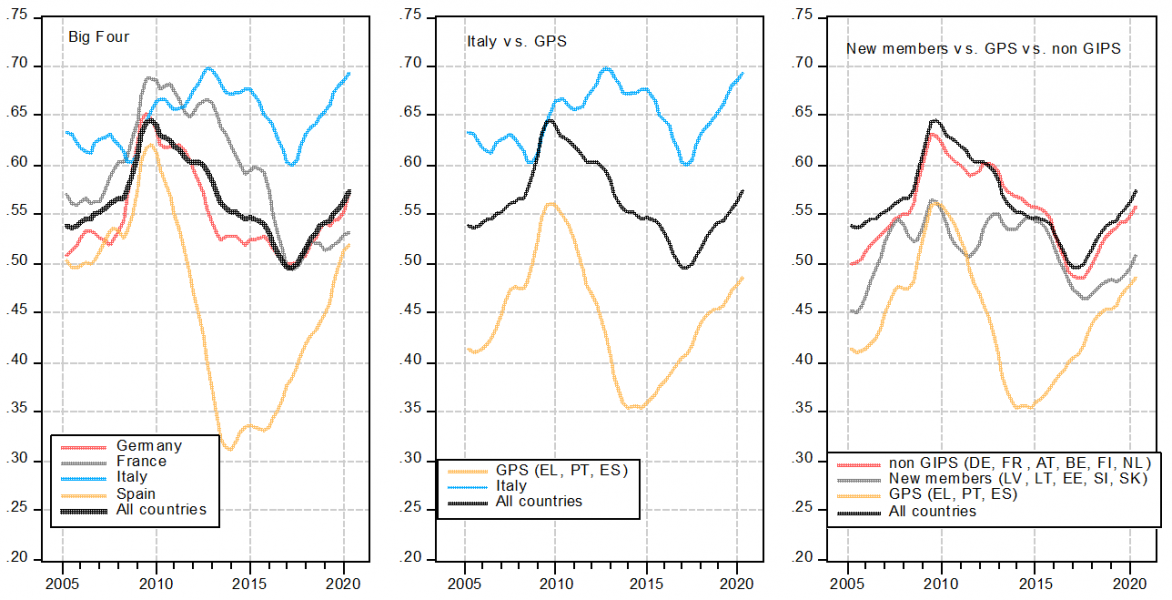

Our analysis points to some interesting cross-country differences in how important symmetric shocks are for their business cycles. Comparing “the Big Four” euro area members, Germany, France, Italy and Spain, Chart 1 (left) shows that Germany and France are usually well aligned with euro area average statistics. In Spain, by contrast, symmetric shocks have been less important. Interestingly, Italy is not only above the average relative importance statistics, but also mostly characterized by the highest share of symmetric shocks among all big countries, in line with findings in related works. In turn, Italy is very different from Greece, Portugal or Spain, even though also heavily stressed countries during the debt crisis (Chart 1 middle). In difference to this group of “stressed” countries, in new member countries, symmetric shocks have gained importance in more recent years and their share is now relatively close to euro area average (Chart 1 right).

Chart 1: Relative importance of symmetric shocks: the big four (left), Italy vs. GPS (middle), some interesting country groups (right)

Note: List of Country Abbreviations: AT Austria, BE Belgium, DE Germany, ES Spain, FR France, FI Finland, EL Greece, IT Italy, NL Netherlands, PT Portugal, EE Estonia, LV Latvia, LT Lithuania, SK Slovakia, SI Slovenia. Relative importance of symmetric shocks is derived from a structural BVAR model identified with a combination of sign and zero restrictions (Kunovac, Rodriguez Palenzuela and Sun, 2022.).

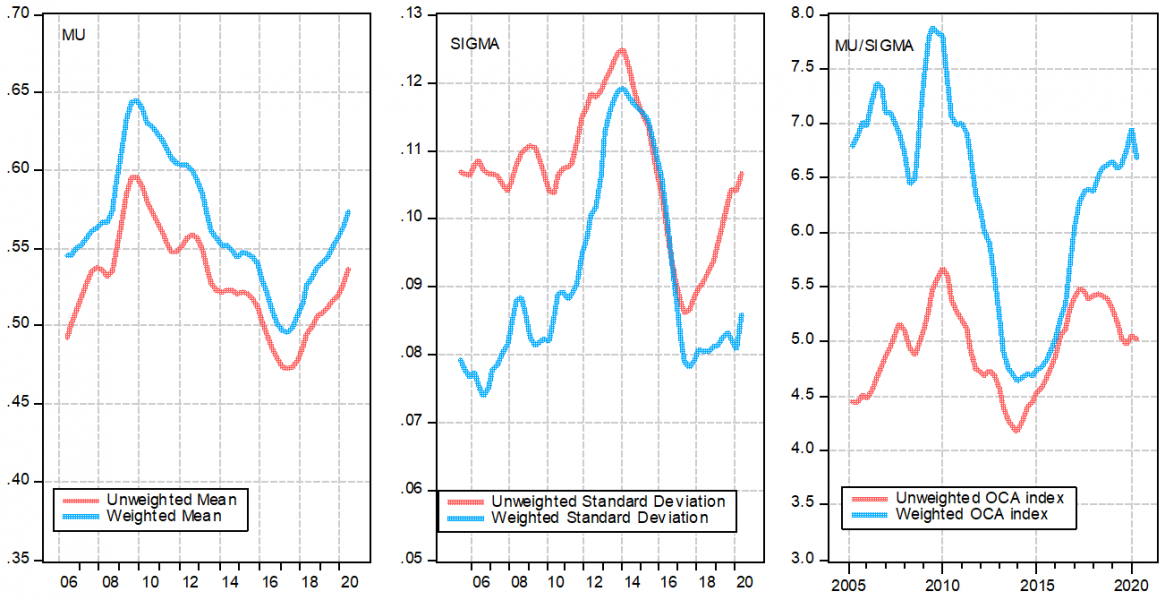

The above analysis of relative importance of symmetric shocks has already been employed in related literature. We take another step and argue that the euro area may be considered as “optimal” if two conditions on cross-country importance of symmetric shocks are met jointly. First, it is preferable for OCA conditions of a union if the cross-country average of relative importance of symmetric shocks (µ) is high (Chart 2 left), as monetary policy in a currency union is more challenged the more the specific regional shocks predominate. Second, it is preferable from the OCA perspective if a high average value of importance of symmetric shocks is attained in a landscape of more homogeneous country structures, i.e. it is desirable that symmetric shocks are of similar importance for all euro area countries. It follows that the cross-country standard deviation of relative importance of symmetric shocks (ơ) should be low (Chart 1 middle) in terms of a sound OCA indicator. Our OCA indices for euro area thus reflect the view that cross-country heterogeneity in business cycle fluctuations makes the common currency not equally desirable for all which could create tensions between countries and eventually even threaten the political viability of EMU (Orphanides, 2020).

A straightforward candidate for such an intuitive time-varying OCA index that embeds the two requirements simultaneously is the signal-to-noise ratio (SNR), µ/ơ. Chart 1 (right) compares two versions of that ratio. The first version assumes equal weights attached to each country (unweighted OCA index), while the second version uses country GDP to calculate pertaining weights (weighted OCA index) when calculating µ and ơ. The weighted index has always a higher value than the unweighted one, reflecting relations between weighted and unweighted cross-country average and standard deviations (weighted µ is always larger than unweighted and the opposite holds for ơ, left and middle panel).

The indices in Chart 2 (both left and right), improved over the first decade following the creation of the EMU. Both weighted and unweighted OCA features tended to surge in times of global crises, as cross-country co-movement was generally high. By contrast, the subsequent sovereign debt crisis, which brought considerable fragmentation levels within the euro area (reflected in increased ơ, middle panel), meant that the OCA features weakened significantly. In the recovery period since 2014 the OCA indicators broadly picked up. However, this pattern was interrupted again in the runup to the COVID-19 pandemic of which the impact on the divergence between country groups was yet uncertain. Overall, the unweighted OCA measure (Chart 2 right) suggests improved OCA conditions for euro area member countries compared to 20 years ago despite unsteady trends and varied speed of progress across different phases. The weighted index, on the other hand, shows little improvement in OCA conditions after the monetary union had to go against various headwind episodes.

Chart 2 also illustrates how the mean of relative importance, µ, alone occasionally points to different dynamics in OCA properties, compared to ratio µ/σ, confirming that both µ and σ are useful for tracking business cycle coherence. For example, rising µ during the last years of our sample, starting from 2017 (Chart 2 left), does not provide clear signal of increased synchronization within euro area as measured by our framework (Chart 2 right) because elevated cross-country dispersion of relevance of symmetric shocks σ (Chart 2 middle).

Chart 2: Weighted and unweighted OCA index

Note: Left panel shows cross-country average of relative importance of symmetric shocks (“signal” µ), middle panel shows cross-country standard deviation of relative importance of symmetric shocks (“noise” ơ) and right panel is signal-to-noise ratio µ/ơ. Unweighted statistics are in red and GDP weighted statistics are in blue. Relative importance of symmetric shocks is derived from a structural BVAR model identified with a combination of sign and zero restrictions (Kunovac, Rodriguez Palenzuela and Sun, 2022.)

Overall, the optimality of the euro area as a currency union remains difficult to assess. Any perception that the European Central Bank (ECB) stabilizing effectiveness may be challenged by business cycle disparities, however, tends to translate into destabilising political signals, not least due to the absence of such an appropriate and unified measure of ’optimality’ for the euro area as a currency union. To counter the risks of a solely sentiment-driven (mis)trust in the euro, we propose a quantitative measure of the OCA properties of the euro area to help anchor perceptions about the ability of common monetary policy to stabilise the aggregate economy, underpinned by the degree of economic cohesion among its constituent member states varying across time. The overall findings broadly confirm gradual – but uneven – progress observed in terms of the co-movement of country-level business cycles in the euro area and the slowly increasing role of common structural factors behind the trend in business cycle alignment.

Kunovac, Davor, Diego Rodriguez Palenzuela, and Yiqiao Sun (2022). “A new optimum currency area index for the euro area.” ECB Working Paper Series No. 2730.

Mundell, Robert A. “A theory of optimum currency areas.” The American economic review 51.4 (1961): 657-665.

Orphanides, Athanasios. “The ECB’s Instruments for Crises and Normal Times: Considerations for the Policy Strategy Review.” (2020).