We employ a model with labor income risk, housing and long-term defaultable loans to measure the long-run economic impact of loan-to-value (LTV) and debt payment-to-income (PTI) caps on mortgage contracts in an economy without aggregate risk. We calibrate it to Portugal, which implemented a 90% LTV cap and a 50% PTI cap on new mortgage lending. We find that the leverage cap can lower mortgage debt-to-output by one third and eliminate the default rate. The PTI cap slightly increases default and household leverage. This stems from the interaction between labor income risk and the PTI cap: households fear future adverse income shocks may constrain their access to credit markets and borrow earlier with lower down payments. We show alternative policy combinations which achieve similar outcomes.

Household borrowing caps have become widespread as a macroprudential policy tool. Overall, a total of sixty economies have enacted some form of explicit limit on household lending standards since 1990 (Acharya et al. 2020). Despite the prevalence of these policies, there is little research on the pros and cons of setting different cap combinations (e.g., limiting leverage, debt service or both), as well as on their effects throughout the income and wealth distributions.

We build a theoretical model of mortgage debt and default without aggregate risk to investigate the effects of a policy which sets loan-to-value (LTV) and payment-to-income (PTI) caps on new mortgage loans on leverage, default, and welfare, both at the aggregate level and across the income and wealth distributions.

We calibrate the model to Portugal, where such a policy was implemented in July 2018. Its aim was to prevent the accumulation of excessive risk in banks’ balance sheets and ensure households obtain sustainable financing, minimizing the risk of arrears. To that end, the policy set an LTV cap of 90 percent and a PTI cap of 50 percent to be met on household loans at origination, which is the baseline policy experiment we conduct.

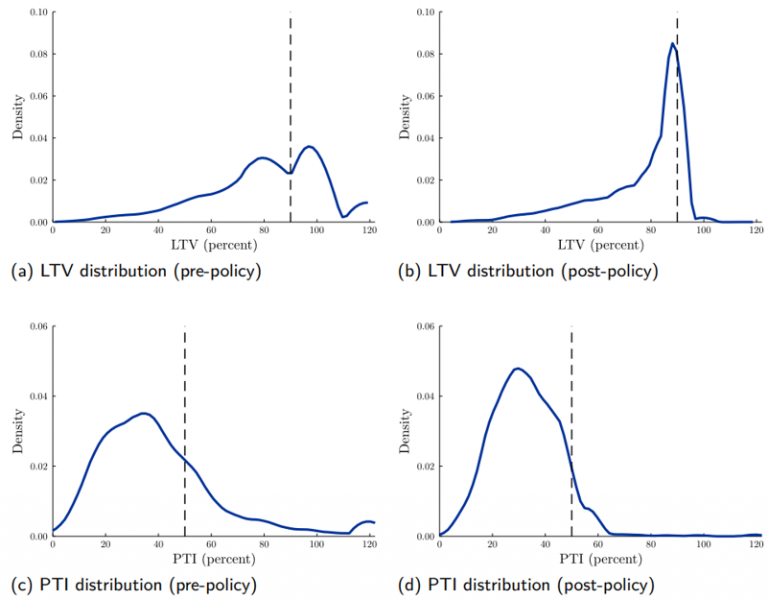

We use micro-data from Banco de Portugal to compute the empirical distributions of the LTV and PTI ratios of new mortgage loans in Portugal. LTV is defined as the ratio between the outstanding loan amount and the value of the house. PTI is defined as the ratio between monthly loan payments (assuming an up to 3 percentage points shock to the interest rate) and after-tax monthly labor income. We find that, in December 2017, before the policy was announced, an LTV cap of 90 percent was binding for around 40 percent of new loans and a PTI cap of 50 percent was binding for 25 percent of new loans (see Figure 1).

In December 2019, after the policy was implemented, more than 50 percent of new mortgages were clustered in the 80-90 percent LTV bucket (compared to 14 percent in December 2017). In contrast, only 25 percent of new mortgages had a PTI higher than 40, indicating less bunching than for the LTV ratio.

Figure 1: LTV and PTI distributions before and after cap implementation.

Half of new borrowers were constrained by the policy.

We find the policy reduces the mortgage debt-to-GDP ratio by one third in the long run. As more equity is needed to satisfy the LTV cap, the homeownership rate is reduced by 7 percentage points. Households take out smaller mortgages, which are paid off quicker, so the share of homeowners with a mortgage drops 10 percent. The average LTV is reduced by 25 percent.

Because the option to sell the house is always available in the model and default leads to its foreclosure by the bank, default is only optimal if the household has negative home equity. Lowering the LTV cap amounts to requiring higher home equity, eliminating the incentive to default in the stationary equilibrium of the economy.

The impact of the policy on house prices is minimal due to long-term mortgages and rental markets, as discussed in Kaplan et al. (2020). Long-term mortgages imply borrowing caps only bind at loan origination and therefore only new borrowers are directly affected by them. Furthermore, rental markets offer credit-constrained households access to comparable housing services, dampening the house price-credit market link. In a nutshell, rental demand replaces ownership demand, reducing house prices by only 2%.

Low interest rates in 2018 implied that a smaller fraction of households was constrained by the PTI cap compared to the LTV cap. This, coupled with the fact that all high PTI loans are associated with high LTV loans, implies that the LTV cap is the main driver of the results. The substantial drop in the mortgage debt-to-GDP ratio follows from both the extensive and the intensive margins: a significant fraction of the aggregate mortgage credit flow is granted to young agents, who start their life with relatively low savings and choose loan contracts with lower down payments. The LTV cap restricts access to the ownership market in the absence of a down payment and the flow of high leverage loans, both of which reduce the size of the debt stock.

We find that setting the PTI cap in isolation raises household borrowing via the intensive and extensive margins, as well as the default rate. As agents are subject to labor income risk, the PTI cap implies that a negative labor income shock may constrain households’ access to credit markets, as the PTI increases for the same amount of loan payments. Since agents are risk-averse and caps only bind at origination, they will borrow earlier and with lower down-payments to insure against the possibility of being cut off from the homeownership market. This results in higher leverage and, because leverage is key to the default decision, in a higher foreclosure rate.

The discovery of this mechanism – which we dub pre-emptive borrowing – is one of the main contributions of the paper. The increase in leverage can leave household balance sheets vulnerable to aggregate shocks, so limits on leverage should accompany the introduction of PTI caps if policymakers wish to dampen this effect.

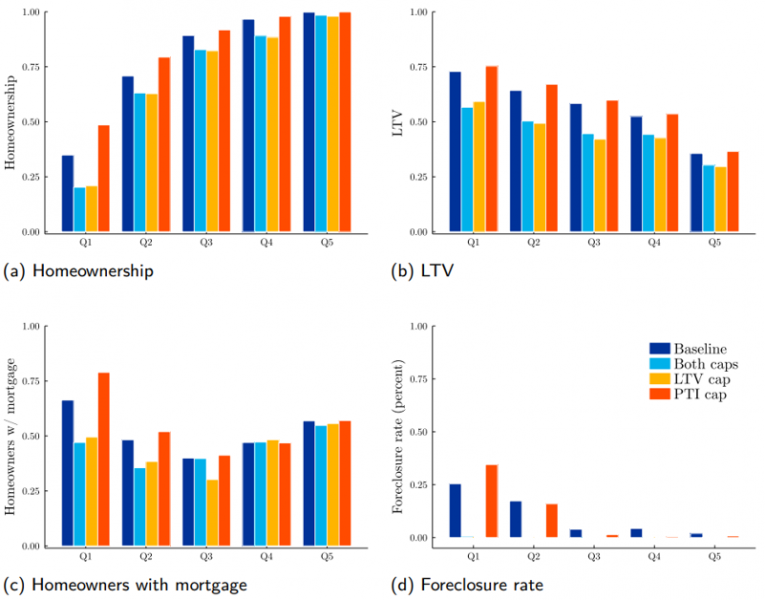

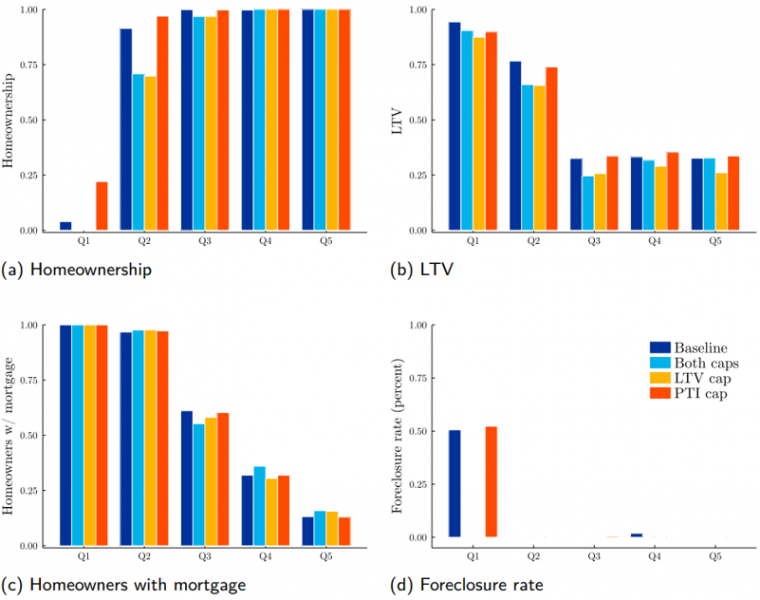

As a result of the policy, homeownership drops across the wealth distribution, but more so in the bottom quintile as poorer households are more constrained by the minimum down payment (see Figure 2). Lifetime LTV drops in all quintiles, as it is less attractive to move to a larger house across the lifecycle. The foreclosure frequency is more severe at the bottom quintiles and disappears with the LTV cap. If the PTI cap is introduced in isolation, the fraction of homeowners with a mortgage increases for the bottom quintiles, due to the pre-emptive borrowing mechanism, which is stronger for wealth-poor households.

Households in the lowest quintiles of the labor income distribution have lower access to the ownership market, as they are often younger and at the beginning of their lifecycle of earnings.1 The foreclosure frequency is more severe at the bottom of the distribution and is eliminated whenever the LTV cap is introduced, as the possibility of negative equity is virtually eliminated, so negative income shocks no longer generate default.

Figure 2: Impact of caps across the wealth distribution for different policy experiments.

Caps reduce access to homeownership more for poorer households.

Note: Q1 to Q5 indicate the quintiles of the wealth distribution. LTV is the lifetime leverage of households. For the color blind, the bars are in the same order as the experiments indicated in the legend. The foreclosure rate is computed as the ratio between the value of defaulted loans per quintile and the value of total outstanding loans at the beginning of the period.

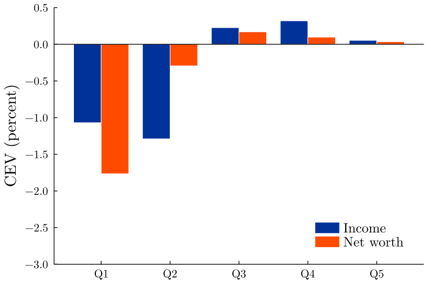

We define aggregate welfare as the expected utility of an agent entering the economy when the policy is implemented. We measure welfare improvements (costs) as the change in annual consumption that would be necessary to produce the same increment (reduction) in utility as that resulting from the policy (the so-called consumption-equivalent variation).

Without accounting for its effects on aggregate risk, the trade-off in this policy can be summarized as follows: on the one hand, caps cut poorer households off from the ownership market, driving them into the rental market, until they save enough for a down payment, which yields lower utility. On the other hand, lower housing demand reduces prices which increases affordability (in both rental and ownership markets) and lowers maintenance costs and property taxes, and fewer defaults reduce the inefficient extra depreciation of foreclosed properties.

Quantitatively, the first effect dominates, on average, for all policy experiments we conduct. We estimate that the 90 percent LTV cap and 50 percent PTI cap reduce welfare by 2 percent. Savings in property taxes and maintenance costs from lower house prices and lower housing stock depletion from accelerated depreciation of foreclosed properties are not enough to offset the costs of excluding a portion of younger and poorer households from the mortgage market (Figure 3). This is fully explained by the LTV cap at origination, as the PTI cap is less binding. For households already in the economy, on average, welfare is mostly unchanged.2 However, it does increase for those at the top of the income and wealth distributions, as they benefit from lower property taxes and maintenance costs.

However, including aggregate risk in the model would be necessary to perform a complete welfare analysis of the policy. In this setup, the market equilibrium can result in overborrowing, as households ignore the effect of borrowing decisions on asset sales and prices during an adverse aggregate shock, leading to fire sales (Lorenzoni, 2008). By limiting debt ex-ante, borrowing caps might mitigate this effect. As such, the benefits of the policy are not yet fully accounted for.

Figure 3: Welfare impact of the main policy experiment by labor income and wealth quintile.

Poorer households are the most negatively affected.

Note: The figure shows the consumption-equivalent variation computed for each quintile of the income and net worth distribution accounting for the transition to a new steady state after the policy is implemented.

Using the model as a laboratory to conduct further experiments with different LTV and PTI caps, we find that the more restrictive the LTV cap is, the lower debt, welfare and default become. In the latter case, the reason is that a large fraction of pre-policy home equity was negative (i.e., loans were larger than housing values) and households with negative home equity are more likely to default. Therefore, having a minimum positive down payment is enough to eliminate foreclosures if house prices remain unchanged. The model predicts that an LTV cap of 95 percent eliminates foreclosures at only half the welfare cost of the main policy experiment.

Restricting the PTI cap has a minimal impact on homeownership or the fraction of homeowners with a mortgage, but it reduces foreclosures. The reason is that a binding PTI cap is less restrictive than an LTV cap, given that households without savings can adjust to the cap by lowering housing demand, rather than being excluded from the market altogether. However, a lower PTI cap reduces the incentive to default, as most households only do so if they are hit by a very adverse labor income shock. Therefore, limiting mortgage payments with respect to risky labor income ensures that the shock required to trigger default is much larger, limiting foreclosures. Lowering the PTI cap to 45 percent reduces the foreclosure rate by three-fifths relative to the baseline policy at only a fraction of the welfare cost.

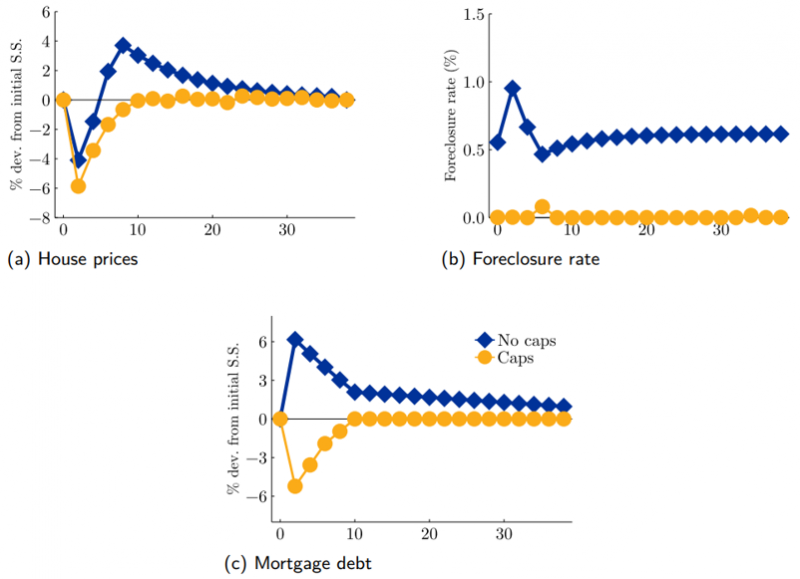

One of the main arguments for the introduction of borrowing caps is their effectiveness in dampening the effect of shocks to the economy. We compare the responses of the economy with and without the borrowing caps to an unexpected and persistent house price decline. It is modelled as a sudden influx of housing into the market. Figure 4 indicates the results.

In the absence of caps, a house price drop is followed by a surge in default, as the fraction of starting high leverage loans is significant. Then, households entering the economy borrow to take advantage of lower house prices and older households upsize the quality of their homes, leading to an increase in credit and a quick rebound in house prices. The increase in house prices reduces the incentive to default and the foreclosure rate quickly returns to its initial level.

With caps in place, the effects are different. First, for the same volume of houses flowing into the market, house prices drop by more and take much longer to recover. Second, credit drops instead of rising due to the borrowing restrictions in place, which explains why it takes longer for the housing market to recover from the shock. Third, the caps successfully prevent any surge in foreclosures, which was one of the main goals of the policy.

Figure 4: Impact of a sudden influx of housing into the market on house prices, foreclosures, and credit, with and without caps in place. The policy prevents a temporary surge in foreclosures, but at the cost of a slower recovery of the housing market.

Note: The x-axis in each subplot are the periods, measured in years.

Our findings suggest that different caps have different impacts in terms of the results of the policy. We highlight that the linkages between credit, ownership and rental markets are essential in understanding the effects of borrowing caps on aggregate variables and across the income and wealth distributions.

Due to the complexity of the model, we are not yet able to provide a picture which includes the intertemporal trade-off between credit access ex-ante and aggregate volatility ex-post. Our next step will be to introduce this key ingredient.

Figure A1: Impact of caps across the labor income distribution for different policy experiments.Caps reduce access to homeownership for younger and poorer households.

Note: Q1 to Q5 indicate the quintiles of the labor income distribution. LTV is the lifetime leverage of households. For the color blind, the bars are in the same order as the experiments indicated in the legend. The foreclosure rate is computed as the ratio between the value of defaulted loans per quintile and the value of total outstanding loans at the beginning of the period.

Acharya, V. V., Bergant, K., Crosignani, M., Eisert, T., and McCann, F. (2020). The Anatomy of the Transmission of Macroprudential Policies. IMF Working Papers 20/58, International Monetary Fund.

Kaplan, G., Mitman, K., and Violante, G. L. (2020). The housing boom and bust: Model meets evidence. Journal of Political Economy, 128(9):3285–3345.

Lorenzoni, G. (2008). Inefficient Credit Booms. The Review of Economic Studies, 75(3):809–833.

The Appendix shows a chart for the impacts across the labor income distribution.

For agents in the economy at the time of the introduction of the policy, welfare is also defined as expected utility. The change in welfare by quintile of the income or wealth distributions is derived from the average expected utility of the agents in that quintile.