This policy brief presents the key findings of the NBB working paper Boudt et al. (2023) Nowcasting GDP through the lens of economic states.

We propose a new state-based weighted estimation approach for GDP nowcasting models. This approach builds on the intuition that we can learn more about current economic growth dynamics from prior data observed in a similar economic state. For this end, we construct new state variables for measuring the similarity of economic time periods using media news data, in addition to financial variables. We find that the state-based weighting of observations leads to economically significant nowcasting gains for GDP growth in Belgium as compared to traditional unweighted approaches.

Effective economic policymaking requires timely estimates of the economic activity in the ongoing quarter, but the official national accounts data only become available with a certain delay. In particular, the first “flash estimate” of the quarterly gross domestic product (GDP) is only released about a month after the quarter has ended and it is often revised in subsequent months.

A solution is to use more timely economic indicators and econometric ‘now-casting’ models to estimate the GDP growth of the current quarter. Timely economic indicators typically include financial data, consumer and business confidence indicators and monthly hard data on unemployment, temporary work, industrial production, trade, as well as on turnover based on VAT returns. The signals included in these timely indicators for the current economic activity can be extracted by leveraging the historical relationship between these indicators and GDP growth using an econometric nowcasting model.

When estimating nowcasting models, it is standard practice to assume a static relationship between the indicators and GDP growth and to treat all prior data equally, but this is a simplification and may lead to suboptimal estimates for economic activity. First, a large number of researchers have shown the importance of time variation in economic relationships. Second, the parameter estimates of the model can to a large extent be affected by a few outliers in crisis periods, such as the large swings in economic activity during the recent COVID‑19 crisis. In particular, the predictive power of several variables that co-moved strongly with GDP growth during the COVID-19 period, such as the VAT turnover of the accommodation and food services industry, is quite poor outside that particular pandemic period.

While previous research has resorted to regime-switching models or time-varying parameter models to incorporate time variation in economic relationships, we propose a novel state‑based weighted estimation procedure. Instead of treating all prior data equally for the estimation of the model parameters, we start off from the idea that we can learn more about current economic growth dynamics from prior data observed in a similar economic state. For instance, if we are experiencing an economic crisis right now, we can learn more from previous crisis periods than from non-crisis periods and vice versa. We operationalise this idea by using weights based on variables that assess the state of the economy. Comparing the current state to the prior states, we assign appropriate weights to the observations in the sample: a greater weight for observations from periods that are similar to the current state, and lower weight for other observations.

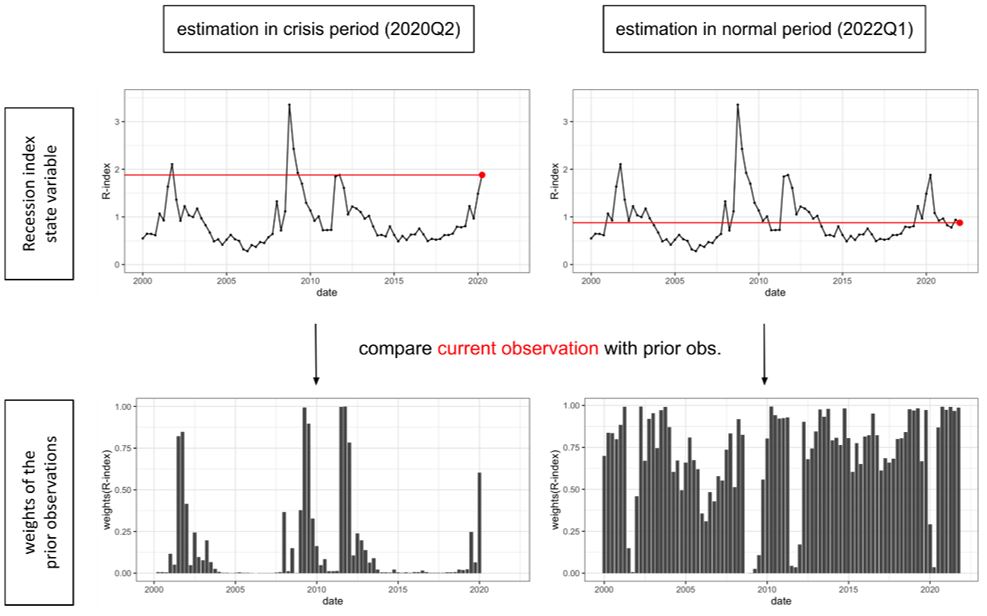

Graph 1 shows an example of the computation of the state-based weights using the Belgian recession-index as state variable. This recession index is an indicator for the attention to recession in Belgian newspapers (see also below). The weight of an observation is a decreasing function of the absolute gap between the current value of the state variable and its value at the time of the observation. The weights for the nowcast performed in the second quarter of 2020 were high for the prior observations with a high recession-index and low for the other observations (see left-hand graphs). The opposite is the case for the nowcast performed in the first quarter of 2022 (see right hand graphs).

Graph 1: Illustrative example: calculation of the state-based weights for the nowcast performed in 2020Q2 and 2022Q1 using the recession-index as the state variable1

1The top graphs show the Belgian Recession-index time series as available at the moment of the nowcast. The red dot shows the value of the state variable at the time the nowcast is performed: 2020Q2 in the left-hand graph and 2022Q1 in the right-hand graph. The bottom graphs show the weights of the prior observations used to fit the nowcasting model using past GDP growth data, namely 2000Q1-2020Q1 and 2000Q1-2021Q4, respectively.

While the idea of state-based weighted estimation is new in a nowcasting context, the value added of state-based weighting has already been shown in investment and risk-management contexts. In particular, a popular practice among tactical investors is to tilt their position towards the asset classes that have performed best in economically similar periods, based on the “Investment Clock” of Greetham and Hartnett (2004). In the context of risk analysis, Meucci (2010) proposes risk-based simulation analysis, in which prior observations receive a higher weight when they correspond to observations that are closer to the current economic situation.

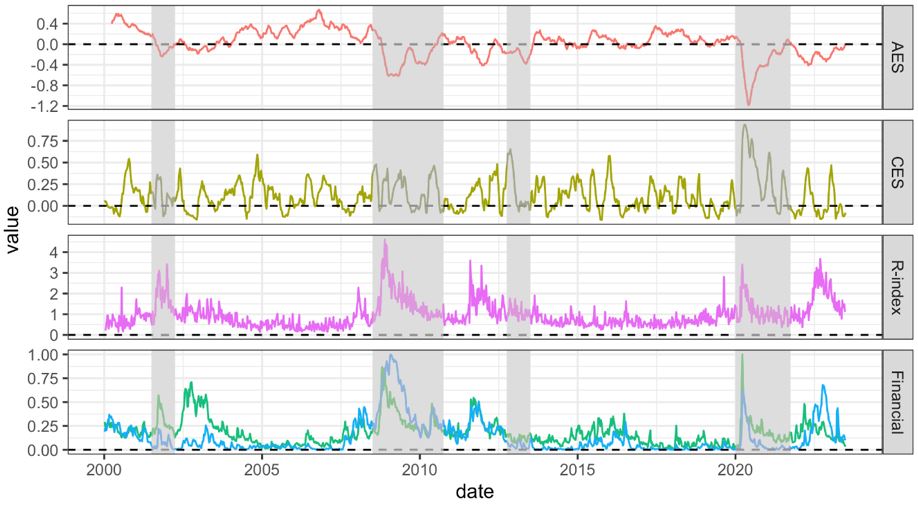

In this study, we capture the state similarity using a combination of complementary timely indicators, in particular media news data and financial variables (see Figure 2). Indicators derived from media sources are important for at least three reasons. First, the qualitative information of news articles (e.g., attention to recession, the tone about the economy) can be expected to be a source of information about the current state of the economy. Second, those media reports could also have a causal effect on economic activity, via their impact on the economic decision-making process of households and firms (Hollanders and Vliegenthart, 2011; Larsen et al., 2021; Gambetti et al., 2023). Third, the media news articles are available in real time and at a daily frequency, enabling us to extract timely information about the current state. Likewise, financial market variables, such as stock market volatility and indicators for systemic stress, are also very timely indicators and they may contain coincident and forward-looking information about the state of the economy.

We constructed novel media news indicators for Belgium based on a dataset of over 20 million media news articles from Belgian newspapers. First, a simple but effective way to detect recession-periods in real time is to look at the attention given to recessions in the news. We make use of a slightly modified version of the Recession index of The Economist (The Economist, 2001). In particular, we count how many articles contain the word “recession” in the Belgian newspapers and divide it by the total number of economic articles (while the Economist divided by the number of all newspaper articles). The Recession index clearly indicates the dot-com bubble, the financial crisis and the COVID-19 crisis. It also spikes for the European debt crisis, at the time a recession was expected, before the actual recession took place.

Two other media news indicators are based on the economic news sentiment, which captures the mood in newspapers articles: does the coverage of the economic situation come with a positive or negative tone? For each newspaper, we use a lexicon-based approach to transform news articles into sentiment scores. The Sentometrics Economic Sentiment lexicon covers finance, economics and business in both Dutch and French and has proven to be very effective in previous research in a now- and forecasting context (Algaba et al., 2023; Ardia et al., 2019). We then construct two aggregate indicators, namely the average economic sentiment of all newspapers and the correlation of the economic sentiment across newspapers. The latter is expected to be able to detect very important economic events as such events will likely be extensively covered by all newspapers and have a similar sentiment, hence leading to a high correlation of the economic sentiment. Chart 2 shows that both indicators are able to detect the four crisis periods in real time.

Graph 2: The media news and financial state variables1

1 State variables from top to bottom: (i) the Average Economic Sentiment in Belgian newspapers (AES) (ii) the Correlation between Economic Sentiment in Belgian newspapers (CES) (iii) the Recession index capturing attention to recession in Belgian newspapers (R-index) (iv) the Euro Stoxx 50 implied volatility (green) and the Belgian Composite Indicator for Systemic Stress (blue). Crisis periods with at least two consecutive quarters of negative GDP growth are marked by the grey areas: (i) the dot-com bubble, (ii) the financial crisis, (iii) the European debt crisis and (iv) the COVID-19 crisis. The start of the crisis period is the first quarter of negative GDP growth and the end is when GDP is again above its pre-crisis level.

By using media news data, our paper also builds on the recent nowcasting literature on the gains from using media news data. However, in the current literature, the news-based variables are mostly added as predictors in an existing model, without adapting the estimation procedure. In this paper, we keep the prediction model and the predictors as they are in the benchmark approach – without news-based variables. Instead, we study the use of news data for improving the estimation of the model parameters.

We show the gains of our state-based weighted estimation for nowcasting Belgian GDP growth. We specifically build on the “BREL” nowcasting model (Piette, 2016) that is routinely used by the National Bank of Belgium. It combines the use of bridge equations to solve the mixed-frequency problem, and the use of elastic net for handling the high-dimensionality.

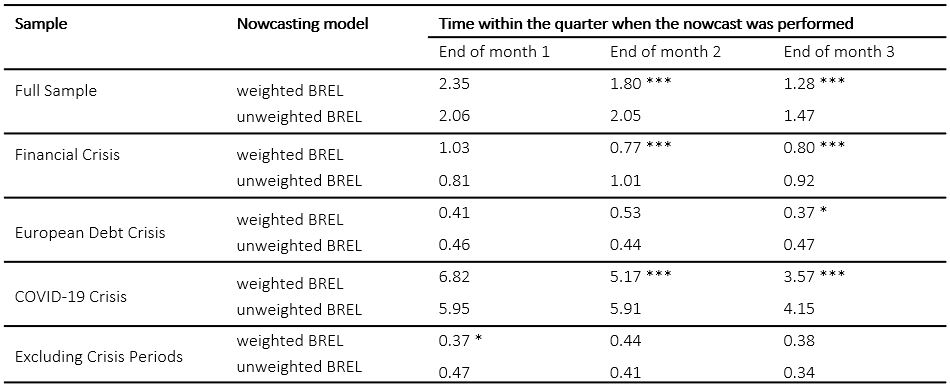

We find that the state-based weighting of observations leads to economically significant nowcasting gains for predicting GDP growth in Belgium as compared to the traditional unweighted approach (see Table 1). Especially during crisis periods and towards the end of the quarter, we find that our weighted approach outperforms the unweighted BREL model.

Table 1: Root mean squared forecast error for the unweighted and state-based weighted nowcasting model for different subsamples1

1 The weighted BREL model in Table 1 uses a combination of the state variables “Recession index”, “Euro Stoxx 50 implied volatility” and “correlation of newspaper economic sentiment correlation” for the computation of the weights. The full out-of-sample period is from Q1 2008 to Q2 2023, the financial crisis period is from Q3 2008 to Q3 2010, the European debt crisis is from Q4 2012 to Q2 2013 and the COVID-19 crisis is from Q1 2020 to Q3 2021. The *, **, *** indicate respectively the statistical significance level 0.05 < p ≤ 0.1, 0.01 < p ≤ 0.05, and p ≤ 0.01 for state-based weighted BREL being superior to unweighted BREL.

Nowcasting models allow to make estimates for the GDP growth of the current quarter by using the information included in timely indicators of economic activity. We propose a new state-based weighted estimation approach of these nowcasting models, building on the idea that we can learn more about current economic growth dynamics from prior data observed in a similar economic state. We find that our state-based weighted estimation leads to economically significant nowcasting gains for GDP growth in Belgium as compared to traditional unweighted approaches.

A challenging question is to select the adequate state variable. We recommend using a combination of timely financial and media news-based indicators. For our nowcasting application for Belgium, we used a combination of the correlation between economic sentiment of popular newspapers, a news-based Recession-index and the implied stock price volatility of the Euro Stoxx 50.

Finally, while the focus of our paper is on nowcasting models, our state-based weighted estimation approach could also provide an elegant and easy to implement solution to deal with extreme observations in other time series models.

Algaba, A., Borms, S., Boudt, K., Verbeken, B., 2023. Daily news sentiment and monthly surveys: A mixed-frequency dynamic factor model for nowcasting consumer confidence. International Journal of Forecasting 39, 266–278.

Ardia, D., Bluteau, K., Boudt, K., 2019. Questioning the news about economic growth: Sparse forecasting using thousands of news-based sentiment values. International Journal of Forecasting 35, 1370–1386.

Gambetti, L., Maffei-Faccioli, N., Zoi, S., 2023. Bad news, good news: coverage and response asymmetries. Finance and Economics Discussion Series 2023-001. Washington: Board of Governors of the Federal Reserve System.

Greetham, T., Hartnett, H., 2004. The investment clock special report# 1: Making money from macro. Merrill Lynch.

Hollanders, D., Vliegenthart, R., 2011. The influence of negative newspaper coverage on consumer confidence: The Dutch case. Journal of Economic Psychology 32, 367–373.

Meucci, A., 2010. Historical scenarios with fully flexible probabilities. GARP Risk Professional, 47–51.

Larsen, V.H., Thorsrud, L.A., Zhulanova, J., 2021. News-driven inflation expectations and information rigidities. Journal of Monetary Economics 117, 507–520.

Piette, C., 2016. Predicting Belgium’s GDP using targeted bridge models. Working Paper 290. National Bank of Belgium.

The Economist, 2001. The R-word URL: https://www.economist.com/finance-and-economics/2001/04/05/the-r-word.