The views expressed in this policy brief are those of the authors and do not necessarily reflect those of the European Central Bank or the Banque de France. It is based on the NGFS Conceptual note on short-term scenarios here.

Climate change is one of the most pressing current policy challenges. Notwithstanding the fundamental uncertainty surrounding its underlying processes, there is mounting scientific evidence that the world might surpass an increase in global temperatures (compared to pre-industrial times) of 1.5 degrees Celsius already within the next five years. It is thus of utmost importance that policymakers get a sense of the short-term impact of climate change and mitigation policies and how they interact with cyclical factors and pre-existing vulnerabilities amid this uncertainty. This is what the Network for Greening the Financial System (NGFS) purports to deliver with its short-term scenarios. Five different narratives are proposed to underpin the dynamics associated with different transition and physical impacts over the next 3-5 years.

Climate change is one of the most pressing current policy challenges. Notwithstanding the fundamental uncertainty surrounding its underlying processes, there is mounting scientific evidence that the world might surpass an increase in global temperatures (compared to pre-industrial times) of 1.5 degrees Celsius already within the next five years. It is thus of utmost importance that policymakers get a sense of the complex short-term impacts of climate change, mitigation policies and how they interact with cyclical factors and pre-existing vulnerabilities amid this uncertainty.

NGFS short-term scenarios will paint a more realistic picture of how the near future could look like. The main novelty is that climate risk impacts interact with pre-existing vulnerabilities (e.g., level of indebtedness) as well as cyclical factors (e.g., confidence shocks), that can thwart or enable the low-carbon transition and thus lead to widely different results. There are two key sources of climate risk. Transition risk refers to the risk of disruption due to sudden shifts in mitigation policies, technological innovation, or preferences. Physical risk reflects the risk of disruption due to severe climate disasters (acute) or slow-moving changes in the climate system like ocean surface temperatures (chronic).

Short-term scenarios will overcome some limitations of financial risk analysis and macroeconomic impact assessment based on long-term scenarios. The time horizon of 3-5 years allows for the construction of a more realistic baseline and a sounder use of constant balance sheet or loan portfolio assumptions in the context of climate stress tests. Moreover, the shorter time horizon allows to zoom into the macroeconomic transmission mechanisms, such as sectoral shifts, that might be particularly relevant for analyzing potential monetary policy tradeoffs along the road.

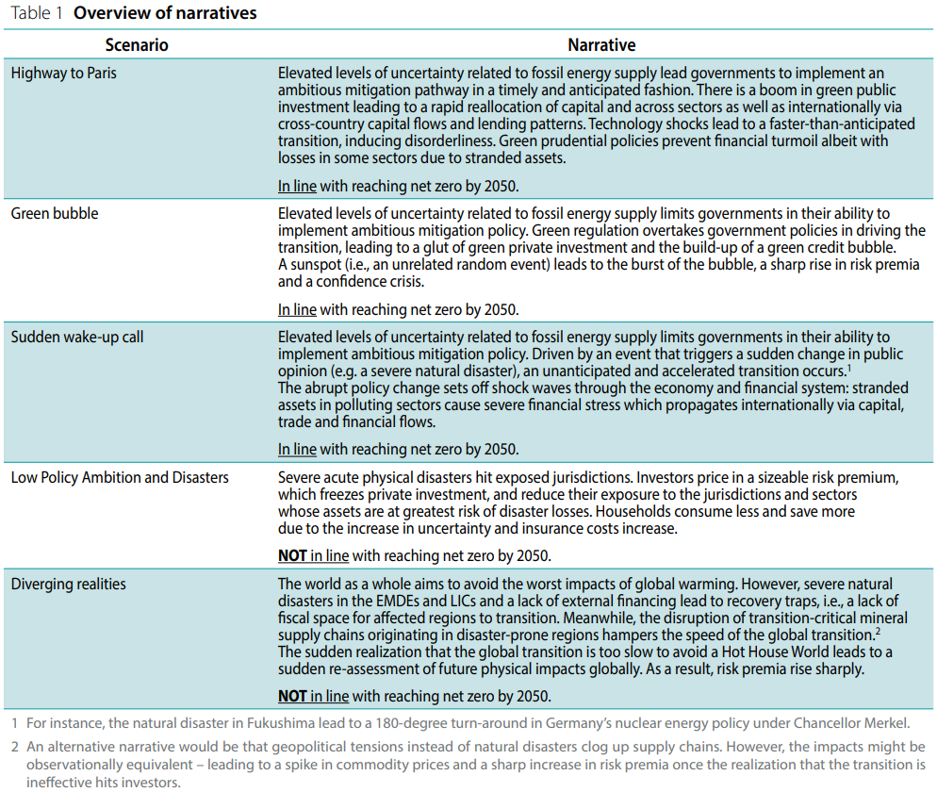

Five different climate scenario narratives describe the short-term dynamics associated with different transition and physical impacts (Table 1). Developing narratives is by no means intended to give a (false) sense of certainty. Rather, the objective is to shed light on a selected set of possible futures to aide in building resilience against what might be ahead. While current narratives serve as a high-level guide to implementing the scenarios, the final scenarios might slightly differ from the suggested narratives due to technical modelling challenges, or to reflect updated policy priorities and commitments.

A careful inspection of the current global macroeconomic setting, policy landscape, climate and portfolio of surrounding risks underlies this thinking:

How key macro-financial variables would evolve in the above-mentioned narratives is not straightforward. The low-carbon transition is likely to cause cross-sectoral shifts in production and consumption patterns with knock-on effects on sectoral prices. The sign of the overall effect depends, among other things, on key elasticities of substitution, accompanying fiscal and monetary policy responses and the specific policy design2. Finally, because much of what is described in the short-term scenarios is somewhat unprecedented, calibrating the shocks will be a creative challenge.

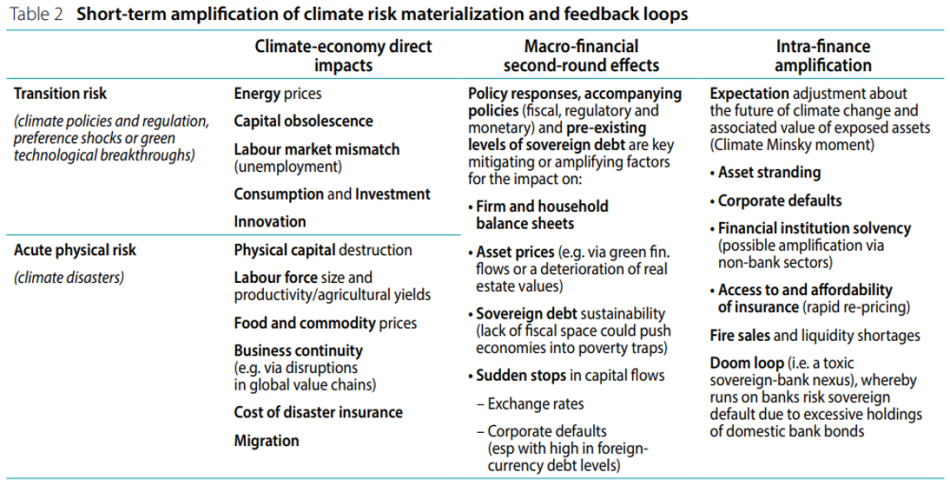

Nevertheless, key transmission channels can be identified. Transition impacts transmit to the economy mainly via energy prices, capital obsolescence and terms-of-trade fluctuations, whereas physical impacts transmit via the destruction of human and physical capital, loss of productivity and agricultural yields, commodity prices, food prices, migration and, possibly, local economic scarring, depending on the nature of the shock. Table 2 classifies these into: (i) climate-economy direct impacts, (ii) macro-financial second-round effects, and (iii) intra-finance amplification following Reinders et al. (2023).

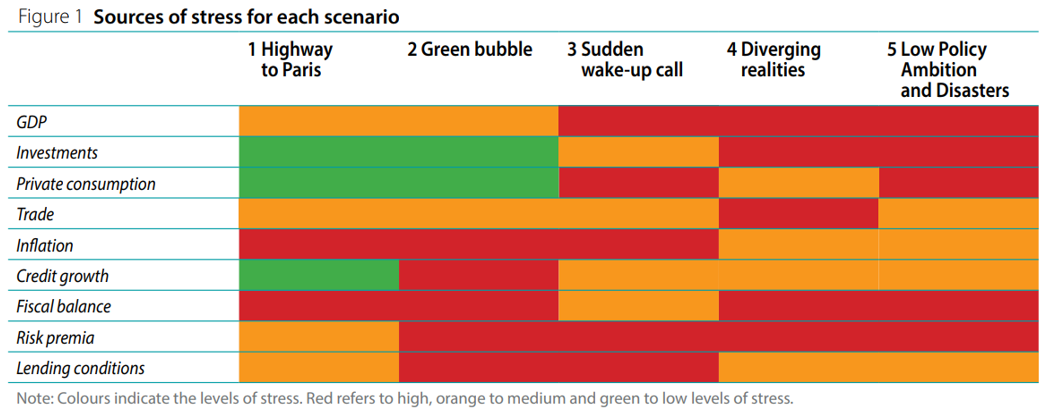

Figure 1 contains a high-level overview of the sources of stress for each scenario. It should not be taken as precise forecasts of what will happen but as an example for how one might think through these narratives. Red refers to a “high” level of stress, yellow to “medium” and green to “low”. Economic activity would be affected under all scenarios, except in the Highway to Paris and Green bubble scenario as investments and private consumption support overall GDP. The source of adversity originates relatively more from the household side in the Sudden wake-up call scenario while the negative investment and trade effects are at the core of the Diverging realities scenario. The transition scenarios are expected to be more inflationary than the scenarios involving physical risks. Financing conditions are likely to be under stress in all scenarios but the Highway to Paris.

The Highway to Paris scenario narrative is the most optimistic narrative featuring a broad-based low-carbon transition, complemented by disruptive green technological progress, incentivized by carbon prices and public investment policies. The steep carbon price acts as a negative supply shock. This is because energy is a key input to most production processes and energy prices are likely to rise initially due to the carbon price inducing a costly shift from current technology based on fossil fuels to more expensive renewable-based alternatives. On the other hand, there is a boom in green public investment financed by carbon price revenue, acting as a positive demand shock. Depending on the relative size of these shocks, the central bank might face a trade-off between limiting inflation and spurring output in the short run.

The Green bubble scenario narrative reflects a world where carbon prices are politically difficult to implement so governments may rely more on subsidy schemes (e.g. Inflation Reduction Act). Instead of taxing the main source of emissions, they foster sectors who innovate and make processes less carbon intensive. Green (innovation) subsidies, if debt-financed, might lead to a boom in green private investment with the risk of a green bubble emerging in financial markets. A crisis of confidence caused by a sunspot may pop the bubble.3 As a result, the risk premium spikes with possible international contagion via exchange rates reflecting sudden stops to heavily exposed jurisdictions and sectors as well as via terms of trade adjustments.

The Sudden wake-up call scenario narrative reflects a world of widespread climate indifference, which is challenged by a sudden change in policy preferences. Markets do not price in climate risks and the energy sector relies heavily on fossil fuels. A sudden change in policy preferences, triggered for instance by a surprise election result favouring green parties, leads governments to hastily implement an accelerated mitigation pathway. In turn, this leads to a sudden re-allocation of capital from polluting to green sectors. The unanticipated nature of this turn of events leads to asset stranding and localized climate Minsky moments.

The Low policy ambition and disasters scenario narrative reflects the short-run repercussions of insufficient long-term climate ambition and thus a continued reliance on fossil fuel. Severe hazard-specific disasters, such as a battery of different but related disaster types driven by El Niño or otherwise compounding disasters, hit exposed regions leading to a spike in risk premia. Energy prices drop due to the contractionary impact of disasters, especially in the most affected regions. The global response to key import/export commodities, likely affected by physical damages (e.g., food prices), could reflect cross-country spillovers in the form of supply chain disruptions. Risk-free rates drop due to the globally contractionary impact of higher risk premia and disaster losses. Exchange rates may adjust reflecting an elevated fear of default vis-à-vis countries exposed to physical hazards. Real estate prices drop sharply in exposed areas affecting particularly vulnerable communities.

The Diverging realities scenario narrative reflects how a lack of external financing from advanced economies can lead to global divergences. Exposed jurisdictions experience repeated severe natural disasters and get trapped in a perpetual state of recovery, reflecting local disruptions in the form of human and physical capital destruction, migration, and productivity drops, as well as global knock-on effects on food and commodity prices and on the supply of critical minerals. Short of external support from advanced economies, affected countries find themselves unable to finance the low-carbon transition. As the overall ineffectiveness of the low-carbon transition becomes clear, risk premia rise sharply. Specifically, this sudden change in the perception of future acute physical impacts could lead to a run on emission-intensive equities and bonds. Moreover, post-disaster spending in exposed regions leads to a worsening of the fiscal balance and to higher sovereign risk premia there.

A key objective of introducing short-term climate scenarios is to better capture the near-term effects of a disorderly transition and severe natural disasters. The five proposed narratives reflect the diversity of shocks that could arise over time horizons of three to five years with different transition and physical impacts. They could be used for climate stress testing, including more adverse effects that could potentially create systemic risk, and for a better understanding of the macroeconomic impacts of various transition paths, their channels and potential trade-offs that could be useful in the monetary policy decision-making process.

This conceptual work serves as a preparatory step for the calibration and implementation of short-term scenarios that will follow in collaboration with an external modelling team.

Reinders, H J, D Schoenmaker and M A van Dijk (2023). “Climate Risk Stress Testing: A Conceptual Review”, CEPR Discussion Paper DP17921.

Trust, Sandy and Joshi, Sanjay and Lenton, Tim and Oliver, Jack (2023). The Emperor’s New Climate Scenarios: Limitations and assumptions of commonly used climate-change scenarios in financial services. University of Exeter and Institute and Faculty of Actuaries.

Since physical risk is pre-determined in the short-run due to a time lag between climate policy stringency and physical risk impacts, there is no connection between the climate policy stringency assumed in the short-term scenario and the level of physical risk impacts. Rather, this scenario should be interpreted as reflecting the short-run implications of living in a Hot House World (Trust et al., 2023).

Energy prices are directly impacted by climate policies targeting the price of fossil fuels and are a key input for virtually all production technologies and home appliances and therefore directly affect firm and household balance sheets. In addition, the energy sector is highly capital-intensive and thus at the risk of premature loss of value. Whether these are ring-fenced, or macro relevant phenomena would likely depend on the level of preparedness and regulation in place.

A sunspot is an exogenous collapse in confidence, i.e. one not related to economic fundamentals.