The views expressed in this article are those of the authors and should not be interpreted as reflecting the official views of Sveriges Riksbank. Based on: Anna Grodecka-Messi, Xin Zhang, Private bank money vs central bank money: A historical lesson for CBDC introduction, Journal of Economic Dynamics and Control, Volume 154, 2023, 104707, https://doi.org/10.1016/j.jedc.2023.104707.

Central banks have been considering the introduction of central bank digital currencies (CBDCs). The theoretical literature indicates that this may influence private banks’ lending activity and their profitability with implications for financial stability. To provide empirical evidence on this debate, we study the effects of the arrival of a new central bank issued currency on commercial banks in a historical setup. We use the opening of the Bank of Canada in 1935 as a natural experiment to provide evidence that banks mostly affected by the currency competition experienced lower profitability but did not decrease their lending compared to unaffected peers.

In recent years, there has been an increased interest from central banks around the globe in central bank digital currencies (CBDCs) issuance. In an increasingly digitalized world, central banks stand in front of a challenge to adapt to the new environment. At this stage, it is difficult to fully identify the advantages and disadvantages of CBDC, given that it may be implemented in several ways, see Bordo and Levin (2017), Mersch (2017) and Keister and Sanches (2023). However, first studies (see Mersch, 2017; BIS, 2018; Stevens, 2017; Mancini-Griffoli, Peria, Agur, Ari, Kiff, Popescu, and Rochon, 2018; Davoodalhosseini and Rivadeneyra, 2018) note that the business model of commercial banks may be affected by the introduction of CBDC, in particular the funding side of the banks (deposits) and their profitability.

Several theoretical papers (Andoflatto, 2021; Chiu et al., 2023; Whited et al., 2022; Williamson, 2021; Keister and Sanches, 2023) consider the effect of CBDC on private banks, studying the impact of new public money on profits, lending, interest rates prevailing in the private market. However, there is a lack of empirical evidence to validate these models, because, as pointed out in Andolfatto (2021), we have no available data to assess the impact of CBDC on commercial banks. First examples of active CBDC projects include quantitative restrictions so that the competition with commercial banking is limited (Söderberg et al., 2022). In situations like this, studying similar events from banking history may provide valuable and insightful factual assessment. In a recent paper (Grodecka-Messi and Zhang, 2023), we draw lessons from a historical experiment in which the central bank introduced a new medium of exchange in competition with the circulating private money. Our findings may shed some light on the impact of new public money (CBDC) issuance on banks’ business models and stability.

We turn our attention to the period when the competition of central and commercial banks over currency issuance played itself out at the cash level. In Canada, which lies at the center of our study, the central bank gained cash monopoly fairly late. Before that, numerous private banks were printing their own money, making it an important part of their funding (Söderberg, 2018). While it may perhaps not be obvious at first, there are many similarities between banknotes and CBDCs. Both central bank cash and CBDC are a form a central bank issued money that should be widely accessible and can be viewed as competition to the commercial banks’ funding sources (private banknotes in the past and deposit money today), see BIS (2018). As Engert and Fung (2017) note, both can be also subject of seigniorage revenue to the central bank. They both can serve as means of payment, unit of accounts and store of value, fulfilling the main functions of money, see Camera (2017).

Of course, some features of CBDC are different than those of cash, e.g. CBDC can be an answer to the zero-lower bound problem, while cash is subject to it. CBDCs are launched in a world with multiple payment technologies and institutions, while notes (and coins) dominated the currency market in the past. The technological challenges of CBDC are clearly different than those of cash. Nonetheless, if CBDC does not pay interest, it is quite similar to cash in its nature, which allows us to make the historical analogy. Our research delivers insights on how central bank’s note monopoly affected commercial banks, focusing on the potential cost side of the implementation of a new form of non-interest bearing central banking money.

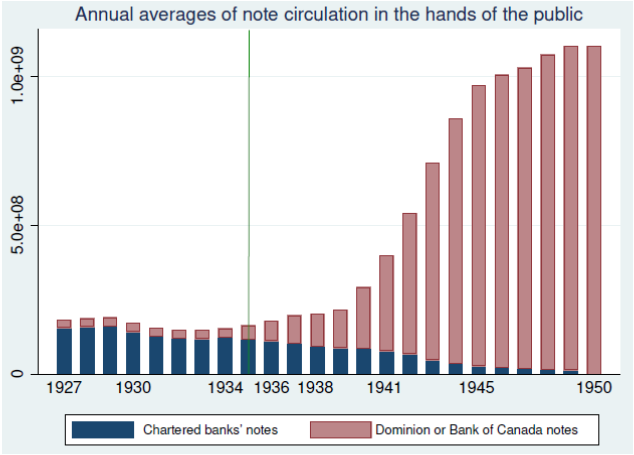

The historic event we studied is the establishment of the Bank of Canada and its money monopoly. In the 19th and the beginning of the 20th century, chartered Canadian banks issued the paper currency in Canada. The right to print money distinguished them from other financial intermediaries in Canada. The majority of the banknotes circulating in the public was issued by commercial banks, as Figure 1 depicts.

The Canadian banking system was operating efficiently without the existence of a central bank, but the economic crisis in Canada and the worldwide economic slump of the 1930s made Prime Minister R.B. Bennett think about establishing a central bank. He set up a royal commission on the 31st July 1933, which advised creating such an institution and the Bank of Canada Act was passed on 3rd July 1934. The Bank of Canada opened its doors on March 11th 1935, and gained banknote monopoly in 1950, but already from 1935 the note-issuing privileges of the commercial banks were restricted. In particular, the Bank Act from 1934 introduced a cap on the maximum issuance of banknotes in relation to the capital and in years 1935-1950, central banks’ and chartered banks’ notes were used in parallel by public. The limit was to be lowered with time by first 5 percentage points (each year) and then 10 percentage points until in 1950 the banks right to issue notes came ultimately to an end.

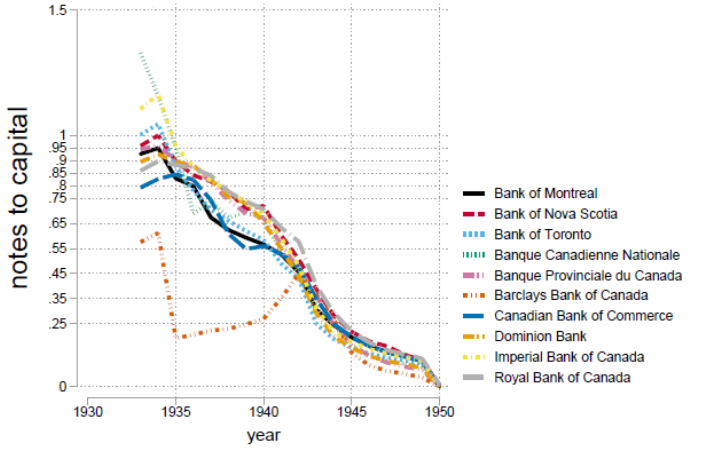

Figure 2 plots the ratio of notes to capital for 10 Canadian chartered banks over the period 1933-1950. The ticks on the y-axis between 1 and 0 indicate different values of the ratio imposed by the law over time. In order to account for expectations, we take into account the distance from the imposed limit in 1933.

Money printing was a cheap way of financing for chartered banks, since it produced seigniorage, while most deposits required paying an interest rate. Despite advantages of using cash as a funding source, the extent to which Canadian banks financed themselves by money printing varied. Those banks that did not rely on banknote printing for their financing would not be immediately affected by the change in the regulation, whilst those with a high reliance on own banknotes would need to change their operating business. We explore this difference between the chartered banks and study how treated (heavily reliant on banknote financing) banks differed from control (not affected by new law) ones in the aftermath of the change using difference-in-differences regressions.

We find that before the change in law, treated and control banks were quite similar and it was their reliance on banknotes that was the most differentiating feature. We run a difference-in-differences regression that shows that banks that were bound by the note issuance limit, experienced 8-24% lower Z-scores and 10-25% lower ROAs. No evidence on changes in lending or provision of services to the public can be noted.

To add robustness to our results, we also consider the development of the Canadian banking system in comparison with international peers over the considered time period. In particular, we apply the synthetic control method to test how the Canadian chartered banking would have evolved in the absence of the monetary reform. We use bank-level data from individual Swedish banks that did not undergo such a reform to construct the synthetic control units. The new results confirm our earlier findings. The arrival of the new central bank money affected Canadian banks’ profits, but not their provision of credit.

Central banks embark on a new journey considering the issuance of CBDCs. Theoretical models can provide guidelines on the new topic considering different forms of CBDC designs. It is important to remember that historical episodes, too, can deliver important insights for the current debates. Our research suggests that commercial banks’ profits may be affected once a new central bank currency is launched in competition to the private money created by commercial banks. This does not have to be accompanied by a decrease in lending. What distinguishes CBDC from banknotes in the past is that while central bank banknotes were natural competitors of private bank notes, CBDC would also compete with other payment instruments. Hence, more research is needed on the potential effects of implementing CBDCs in the modern economies, including the potential implication of CBDC as a new payment technology.

Andolfatto, D. (2021): “Assessing the Impact of Central Bank Digital Currency on Private Banks,” Economic Journal, 131, 525–540.

BIS (2018): “Central bank digital currencies”, Bank for International Settlements.

Bordo, M. D. and A. T. Levin (2017): “Central Bank Digital Currency and the Future of Monetary Policy”, NBER Working Paper.

Camera, G. (2017): “A perspective on electronic alternatives to traditional currencies”, Sveriges Riksbank Economic Review, 1, 126-148.

Chiu, J. and S. M. Davoodalhosseini, and J. Jiang and Y. Zhu, (2023): “Bank Market Power and Central Bank Digital Currency: Theory and Quantitative Assessment”, Journal of Political Economy 2023 131:5, 1213-1248.

Davoodalhosseini, M. and F. Rivadeneyra (2018): “A Policy Framework for E-Money: A Report on Bank of Canada Research,” Bank of Canada Discussion Paper.

Grodecka-Messi A. and X. Zhang (2023): “Private bank money vs central bank money: A historical lesson for CBDC introduction”, Journal of Economic Dynamics and Control, Volume 154, 104707.

Engert, W. and B. Fung (2017): “Central Bank Digital Currency: Motivations and Implications”, Bank of Canada Discussion Paper.

Keister, T., Sanches, D., (2023): “Should central banks issue digital currency?” Rev. Econ. Stud, Volume 90, Issue 1, Pages 404–431.

Mancini-Griffoli, T., M. S. M. Peria, I. Agur, A. Ari, J. Kiff, A. Popescu, and C. Rochon (2018): “Casting Light on Central Bank Digital Currency”, IMF Staff Discussion Note, 18/08.

Mersch, Y. (2017): “Digital Base Money: an assessment from the ECB’s perspective,” Speech by Yves Mersch, Member of the Executive Board of the ECB, at the Farewell ceremony for Pentti Hakkarainen, Deputy Governor of Suomen Pankki – Finlands Bank, Helsinki, 16 January 2017 [acessed 12-03-2019].

Stevens, A. (2017): “Digital currencies: Threats and opportunities for monetary policy”, NBB Economic Review.

Whited, T. M., Wu, Y., Xiao, K. (2022): “Central bank digital currency and banks.” Available at SSRN 4112644.

Williamson, S.D. (2021): “Central bank digital currency and flight to safety”, J. Econ. Dyn. Control 104146.

Söderberg, G. (2018): Why did the Riksbank get a monopoly on banknotes?”, Sveriges Riksbank Economic Review, 3, 6-16.