Building on the distinction between measurable risk and uncertainty, I analyze the fundamentals of the main regulatory frameworks of the last two decades. The resulting excessive regulatory complexity might turn out to be sub-optimal for crisis prevention. Since modern finance is characterised by uncertainty (rather than risk), rebalancing regulation towards simplicity, a step that has been undertaken with the final Basel III Accord, may encourage better decision making by authorities and regulated entities. As addressing systemic risk in a complex financial system should not entail the replacement of overly complex rules with overly simple or less stringent regulations, the challenge is to define criteria to assess the degree of unnecessary complexity in regulation. To this end, I propose some options affecting the content of the rules, the regulatory policy mix for certain financial sectors, as well as the rulemaking process.

In the last decades the international financial system has shown a tendency towards increasing complexity. Economists have defined this complexity in terms of greater variety of types of financial intermediaries and instruments, longer intermediation chains, greater interconnectedness among sectors, making it difficult to trace and monitor each institution’s network of direct and indirect linkages.

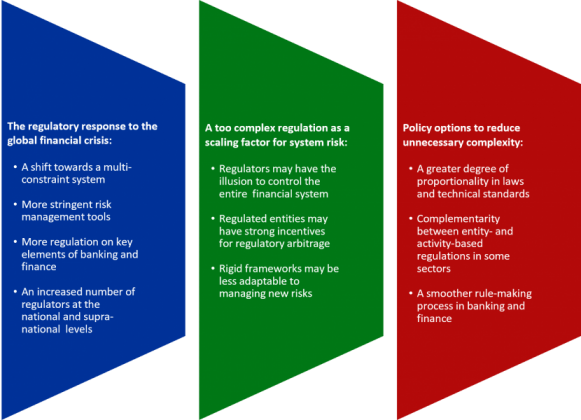

In response to these developments, financial regulation has also become very complex, being based upon sophisticated risk management tools, underpinned by complicated rulebooks. This situation has raised concerns, stemming from a number of factors: regulators may be led into the illusion of fully controlling the entire financial system; intermediaries may have incentives to engage in regulatory arbitrage; excessively complex regulation may produce rigid frameworks, less adaptable to managing fast-changing environments.

Figure 1: How to reduce regulatory complexity: some policy options

The theoretical foundations of these regulatory frameworks can be found in models of decision-making under risk, which assume that the probability distribution of all possible states of the world can be calculated, and decisions can be made rationally with the application of mathematical and statistical tools. This view mainly derives from the model of Arrow and Debreu, according to which there exists a Walrasian equilibrium in financial markets, and from the theory of portfolio allocation, which assumes that decision-makers take optimal choices, since they are able to measure all relevant factors and perfectly price, trade, and hedge risks. In these settings, information can be acquired and processed at a cost close to zero, and the use of more information always increases effectiveness. Unfortunately, the historical experience of the last 50 years shows that quite often these decision tools have neither allowed correct choices nor avoided instabilities.

Contrary to this view, over the years several economists have focused on imperfections in information and knowledge, and suggested that uncertainty, rather than measurable risk, is the normal context of decision-making. This means that assigning probabilities to future events is particularly difficult, especially for rare, high-impact events, such as financial crises, which bear distinctive features that cannot be modelled ex ante. Over the years, the so-called ‘Knightian’ uncertainty has gained increased attraction in shaping theoretical and empirical research in finance, given the limitations of the mainstream view in capturing the key elements of the real world.

The uncertainty prevailing in modern finance refers to a complex system in which the overall effect of a single event cannot be analysed statistically, due to several factors that are likely to operate simultaneously (non-linearity, fat tails, second-order uncertainty, random correlation matrixes, contagion). Combined with the very high number of possible events, these factors do not allow a statistical treatment of risks. Rather, ‘heuristcs’ becomes the only possible way-out.

Since collecting and processing all the information necessary to take complex decisions is costly, and probabilistically calculating the future states of the world is beyond human capacities, heuristics and ‘bounded rationality’ allow to formulate decision making strategies that ignore part of the information and involve limited computation. The viable response to a complex environment is not a fully state-contingent rule; rather, it is to simplify.

Moving from risk to uncertainty, it can happen that complex decision rules can underperform if compared with rules based on simple averages or less information. Uncertainty may imply potential benefits to more simplicity over greater complexity, given the higher degree of flexibility allowed. There are a number of channels through which uncertainty may make the financial system more fragile. To the extent that regulatory complexity may add to uncertainty (as a minimum, there is uncertainty on the reactions by banks and other financial institutions to the multiple constraints imposed by a complex regulatory framework) complexity in regulation can increase the amount of risks hidden in the system.

The global financial crisis (GFC) of 2007-08 has forced central banks and regulators to reconsider the scale of systemic risk and its contagion mechanisms, triggering a severe revision of financial regulation, thus creating a multi-layered system with a high number of constraints (i.e., more intrusive rules, more stringent risk management tools, and more regulators).

The reasons for this regime change stem from the failure of the old regulatory framework, mainly centred upon a single tool (i.e., capital requirements on banks), to address the economic externalities arisen during the GFC. In fact, attempting to make the system safe by ensuring the safety of individual banks may overlook a fallacy of composition: in trying to make themselves safer, banks may collectively undermine the system. Risk becomes endogenous to bank behaviour, and the increasing role of markets intensifies such endogeneity.

This is why macro-prudential regulation has been introduced, and the regulatory toolkit has been revised to include the non-bank financial intermediation sector. This multi-layer framework is more robust, as each measure offsets the potential shortcomings and adverse incentives of the others, and has allowed the international banking system to increase its solvency and liquidity conditions, enhancing its resilience to external shocks, such as the COVID-19 emergency.

The overall policy response to these externalities/frictions seems to be the materialization of the Tinbergen’s rule, which states that to achieve the desired levels of a certain number of objectives for the policy maker needs to control an equal number of tools. In the post-GFC regulatory framework, as many regulatory instruments have been defined as the number of externalities to be dealt with. Limiting the analysis to banks (i.e., not considering markets, infrastructures, non-bank financial entities) and to the most significant externalities, one can refer to the following tools: liquidity standards, leverage ratio, revised risk-based capital requirements (including the systemic capital surcharge), total loss absorbing capacity requirements, capital conservation and counter-cyclical buffers, and resolution regimes. In other words, the post-GFC regulatory repair has proceeded on a friction-by-friction (and rule-by-rule) basis.

However, the post-financial crisis framework has increased the density and complexity of financial regulation. This excessive complexity may create barriers to entry for newcomers, limiting competition and innovation; the burden imposed on the regulated entities encourages the transfer of risks outside the regulatory perimeter. And supervision may become a mechanic tick-box exercise, rather than a comprehensive assessment of the riskiness of each individual entity.

In this context, I study the regulatory pendulum involving different degrees of complexity and/or simplicity in banking regulation with reference to sequence of Accords finalized by the Basel Committee on Banking Supervision (BCBS) over the years, starting in 1988. In this context, the issue of complexity derives mainly from banks’ use of internal models for calculating capital requirements, and from the widening of the regulatory coverage of risks over time.

The final 2017 Basel III Accord recognizes the need for simple models and simpler regulatory rules and practices. These reforms contain several amendments addressing complexity in financial regulation, especially in the calculation of risk weighted assets, in order to improve the comparability of banks’ capital ratios. These reforms have been built upon the strategic review of the risk-weighted capital framework, performed by the BCBS to achieve a right balance in terms of simplicity, comparability and risk sensitivity. They have been grounded into three broad categories: enhancing the risk sensitivity and robustness of standardized approaches; reviewing the role of internal models in the capital framework; finalizing the design and calibration of the leverage ratio and capital floors. This package has been completed through a ‘fundamental’ revision of the rules affecting the market risk framework, tailored to reduce excessive complexity and opacity, through more stringent criteria for the use internal models and enhanced risk sensitivity overall.

It is by no means simple in itself, of course; but it does contain comparatively simple backstops to avoid some of the pitfalls of complexity. It is important to outline that regulators are confronted with a trade-off: simple rules are transparent, robust to model risk and more difficult to ‘game’, but they may fail to measure risks adequately; complex rules may be risk-sensitive, but they are more likely to determine model failures. Furthermore, both are subject to the Lucas critique, since banks and markets adapt to the rules, and this makes the task of the regulators very hard.

The complexity embedded in the regulatory framework developed so far may not represent the optimal response to the uncertainty prevailing in the markets and to the externalities/frictions resulting from the GFC. A higher degree of complexity in the regulatory framework is justified if it enhances the intermediaries’ capability to withstand unexpected losses, and at the same time improves the objective function of regulators, thus improving financial stability overall.

A substantial amount of applied economic research has compared the performance of simple vs complex rules on issues of strategic importance for regulators and banks (e.g., bank weakness, crisis forecasting) in a variety of samples and periods, in normal as well as in crisis times, collecting evidence that in banking regulation “less” may become “more”.

These strands of research have shown that less complex rules could sometimes do a better job in dealing with Knightian uncertainty and in meeting supervisory objectives. Moreover, theoretical and empirical studies have documented that the complexity of rules may impact the ability of regulators to oversee them, while simpler rules may increase the incentives for their enforcement from the perspective of both regulators and financial institutions.

Simpler rules can also perform better with respect to changes in the incentives of regulated entities. When banks modify their structure and business models over time, internal models based upon the use of past data may become a not viable option to calculate current risks, even if we leave aside their inherent complexity.

In principle, this situation seems to call for greater simplicity in regulation. However, even if simple rules can be attractive, they cannot be considered a supervisory goal per se. Addressing risks in a complex financial system should not entail the replacement of overly complex rules with overly simple or less stringent regulations. There are many instances – even in the reforms finalized after the GFC – where simple rules may not have helped in practice to reduce regulatory complexity.

In designing a balanced approach to regulation, a feasible way-out should be to reduce complexity in financial rules whenever it is deemed unnecessary. Two key objectives would be: 1) to give regulators an increased capacity to address unknown contingencies in a flexible way, possibly by recalibrating a few basic tools, and by adopting policy responses in a smooth and timely way; 2) to reduce regulated entities’ incentives to game the system and to move risks outside the regulatory perimeter, as well as their compliance costs.

The real (and difficult) challenge would be to define criteria and methods to assess the degree of unnecessary complexity in regulation. To this end, I propose some options affecting the content of the rules, the regulatory policy mix for certain financial sectors, as well as the rulemaking process.

Aikman D., Galesic M., Gigerenzer G., Kapadia S., Katsikopoulos K., Kothiyal A., Murphy E., and Neumann T., (2014), “Taking uncertainty seriously: simplicity versus complexity in financial regulation”, Bank of England, Financial Stability Paper Series, No. 28

Duffie D., and Sonnenschein H., (1989), “Arrow and General Equilibrium Theory”, Journal of Economic Literature, 27 (2), pp. 565-598.

Knight F. H., (1921) “Risk, Uncertainty, and Profit”, Boston, Houghton Mifflin.

Simon H. A., (1955), “A Behavioural model of rational choice”, Quarterly Journal of Economics, 69, pp. 99-118;

European Systemic Risk Board, (2019) “Regulatory complexity and the quest for robust regulation”, Reports of the Advisory Scientific Committee, No. 8, June.

Haldane A. G., and Madouros V., (2012), “The Dog and the Frisbee.” Speech given at the Federal Reserve Bank of Kansas City’s 36th economic policy symposium, Jackson Hole, Wyoming, August 31.

Signorini L. F., (2017), “Of dogs, black swans and endangered species: a perspective on financial regulation”, Laudatio of Andrew G. Haldane, Palermo, December.

Trapanese M., (2022), “The international efforts to manage non-bank financial intermediation risks: where do we stand?”, Central Banking, Volume XXXII, Issue 4, June, pp. 38-44 (also published online on April 26).

Trapanese M., (2022), “Regulatory complexity, uncertainty, and systemic risk”, Bank of Italy, Occasional Papers, No.698, June.

Visco I., and Zevi G., (2020), “Bounded rationality and expectations in economics”, Bank of Italy, Occasional Papers, No. 575, July.