This Policy Brief is based on Latvijas Banka Working Paper 6/23. The views expressed herein are solely those of the authors and do not necessarily reflect the views of Latvijas Banka or the Eurosystem.

Mitigating climate change requires decarbonizing production processes. However, this might render assets stranded, impacting not only the relevant sector but also causing a ripple effect across all sectors. Using a calibrated two-sector New Keynesian model with green and brown capital and input-output linkages, we find that stranded brown capital in the brown sector yields an economic relocation to the green sector and lower emissions with small economic costs. Brown consumption taxes also facilitate the green transition, while brown investment taxes or green investment subsidies are less favorable policies in this respect. Doubling the brown sector’s carbon tax yields significant relocation activities at small economic costs. If monetary policy responds strongly to the short-run inflationary pressures of carbon tax increases, larger output losses in the short run and higher output gains in the long run are the consequence.

Mitigating climate change is a formidable task at both the global and the local level, which requires substantial ambition and effort in decarbonizing production processes. The objective of achieving a climate neutral world by 2050 necessitates significant reductions in greenhouse gas emissions which come with considerable costs. While some of these costs are incurred directly through policymaking efforts to restructure economies such as carbon pricing mechanisms and policies to promote energy efficiency and requirements for renewable energy investments, a significant portion results from the phenomenon of asset strandedness which unfolds over the medium to long run. Asset strandedness refers to a situation where existing economic assets are rendered incapable of generating intra-sector value added to the full extent, leading to negative inter-sectoral interactions (Caldecott et al., 2014; Cahen-Fourot et al., 2021; Godin and Hadji-Lazaro, 2022).

Utilizing advancements in economic modelling that integrate production networks via input-output linkages in general equilibrium models (Ghassibe, 2021; Hinterlang et al., 2021, 2022; Frankovic, 2022; Ernst et al., 2023), we seek to quantify the equilibrium effects of stranding assets in one sector, taking into account the network propagation effects that might even be larger than the direct effect in the originally affected sector. Since public policies are likely to interact with the effects of stranded assets, we also delve into the analysis of several tax and subsidy policies belonging to governmental toolkits. In addition, we incorporate monetary policy interventions in our model, as the aforementioned shocks and policies might lead to inflationary pressures, especially in the short run.

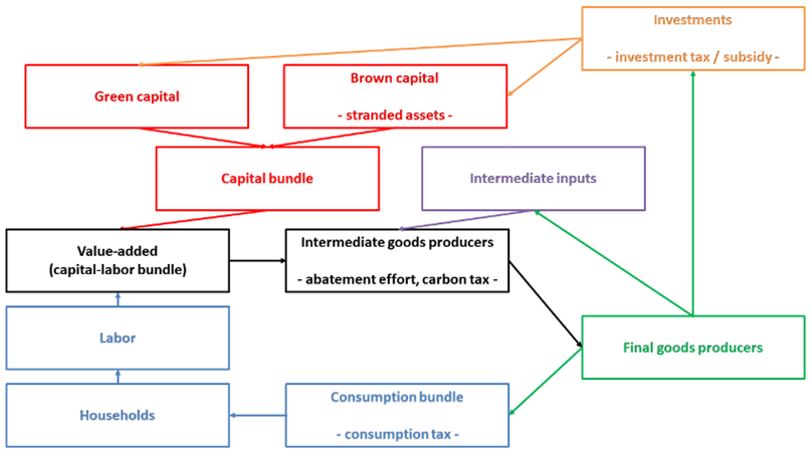

To provide a quantitative assessment of the formulated research questions, we develop a two-sector New Keynesian DSGE model with green and brown capital and input-output linkages. The two sectors are labelled as green and brown, using the green taxonomy of the European Union as a guide to categorize the sectors at the NACE-2 level as either green or brown. The model is calibrated to the euro area, using detailed data on aggregate consumption composition, input-output linkages, and capital types at the NACE-2 level. Figure 1 provides a bird’s eye’s view of the key agents, flows of goods, and public policy instruments in our model.

We proxy for a situation where assets become stranded by simulating a negative shock to the brown capital utilization rate in the brown sector and studying the economic and environmental effects of such a shock. The environmental dimension of the problem is considered by computing emissions as a by-product of production processes (the brown sector’s emissions intensity is several times higher than the green sector’s emissions intensity, in line with the data). The stock of emissions in the atmosphere disrupt production processes by means of a damage function in the spirit of integrated assessment models, pioneered by Nobel Laureate William D. Nordhaus (e.g., Nordhaus, 2017).

Figure 1: Model overview

In addition, various public policies are being used by governments to reduce emissions and assist with the transition to a greener economy, which could either cause or appear contemporaneously with the emergence of stranded assets. In particular, we add multiple fiscal instruments to the governmental toolkit in our model. Therefore, the government can levy a tax on the consumption of each good (in particular, a consumption tax on the brown good), a carbon tax on firms in each sector, or it can subsidize or tax green or brown investment efforts. Moreover, monetary policy is active in our model to keep inflation under control, and we will analyze how the strength of the response to the short-run inflationary pressures of carbon tax increases affect the economic dynamics.

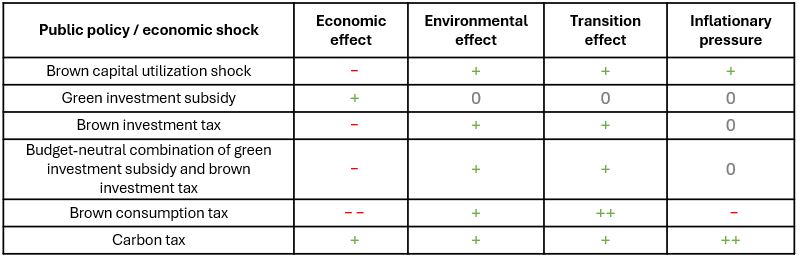

In Table 1, we summarize the equilibrium effects of our analyzed scenarios with respect to the economic effect (i.e. how aggregate output reacts to the policy or shock), with respect to the environmental effect (i.e. whether emissions decline or increase in response to the introduction of the policy or the realization of the shock1), with respect to the transition effect (i.e. whether the green sector grows at the expense of the brown sector or not, and with respect to the inflationary pressure (inflation or deflation observed).

Table 1: Impacts of public policy and economic shocks on economic performance, inflation, and environment

Firstly, a brown capital utilization shock is overall negative news for the aggregate economy as aggregate output decreases while at the same time creating inflationary pressure. However, it is good news for environmental dynamics as the green sector expands its production output and the brown sector scales down production, which implies that emissions decrease. Secondly, the government supplying subsidies to green investment (i.e. via the government paying for a part of green investment expenditures of firms in the green sector) does not yield significant effects on the dimensions of the environment, the green transition, or inflation. However, it generates an economic expansion in the aggregate. Thirdly, a tax on brown investments in both sectors impairs the accumulation of brown capital in the economy by reducing investments in brown capital, which leads to an economic recession but also reductions in emissions and the share of the brown sector in the economy, while not generating any inflationary pressure. Fourthly, a tax on the consumption of the final goods of the brown sector, borne by households, yields the largest recession among the considered policies, while also creating the largest relocation of production activities to the green sector. The environmental benefit due to the lower emissions intensity of the green sector is significant as well, while it also creates some deflationary pressure due to the economic recession dominating the price increase due to the new consumption tax. Finally, doubling the carbon tax in the brown sector from 40 euros per ton of carbon to 80 euros per ton of carbon creates significant inflationary pressure in the short run, a significant reduction in emissions, and a sizeable movement of production activities away from the brown sector to the green sector. Although the aggregate economic effect is not positive throughout the horizon considered ̶ indeed, a recession is observed in the medium run ̶ overall the aggregate economy seems to benefit in most quarters due to the reduction of climate damages.

Due to the strong but short-lived increase in inflation, we also perform an additional analysis of the carbon tax scenario by varying the strength of the response of the monetary policy interest rate to inflation. We find that the stronger the central bank reacts to the inflation surge, the more detrimental are the economic effects in the short run (lower consumption and output) but the better are the economic dynamics in the medium to long run. This is due to a larger nominal interest rate in the short run (as the nominal interest rate increases more at times when inflation is high) that makes the transition more costly initially but a smaller nominal interest rate in the medium to long run (i.e. during a time where deflation is observed) that reduces the costs of transitioning to a greener economy then.

We have also looked at a budget-neutral combination of the investment policies (i.e. a subsidy to green investment in the green sector and taxes to brown investment in both sectors such that the government does not need to run a fiscal deficit). This analysis demonstrates that a significant environmental benefit and a sizeable relocation of production activities can be achieved by using investment-related fiscal instruments. The downside to this policy mix is the observed small, yet non-negligible reduction in aggregate output.

Our analysis provides evidence of a significant risk for the aggregate economy from stranded assets. It creates inflationary pressure and reduces aggregate output of the economy, while being beneficial for facilitating the transition to a greener economy and for the environment.

In a situation where brown assets become stranded, an expansionary fiscal policy such as subsidies to green investment can alleviate the economic costs of stranded assets effectively. However, if the fiscal space is constrained and such an investment policy needs to be implemented in a budget-neutral manner, the policy might lose its expansionary nature.

Cahen-Fourot, L., Campiglio, E., Godin, A., Kemp-Benedict, E. and Trsek, S. (2021). Capital stranding cascades: The impact of decarbonisation on productive asset utilisation. Energy Economics, 103, 105581.

Caldecott, B., Tilbury, J. and Carey, C. (2014). Stranded Assets and Scenarios. Stranded Assets Programme Discussion Paper – January 2014.

Ernst, A., Hinterlang, N., Mahle, A. and Stähler, N. (2023). Carbon pricing, border adjustment and climate clubs: Options for international cooperation. Journal of International Economics, 144, 103772.

Frankovic, I. (2022). The impact of carbon pricing in a multi-region production network model and an application to climate scenarios. Deutsche Bundesbank Discussion Paper No. 07/2022.

Ghassibe, M. (2021). Monetary policy and production networks: an empirical investigation. Journal of Monetary Economics, 119, 21–39.

Godin, A. and Hadji-Lazaro, P. (2022). Identification des vulnérabilités à la transition induites par la demande: application d’une approche systémique à l’Afrique du Sud. Revue économique, 73 (2), 267–301.

Hinterlang, N., Martin, A., Röhe, O., Stähler, N. and Strobel, J. (2021). Using energy and emissions taxation to finance labor tax reductions in a multi-sector economy: An assessment with EMuSe. Deutsche Bundesbank Discussion Paper No. 50/2021.

Hinterlang, N., Martin, A., Röhe, O., Stähler, N. and Strobel, J. (2022). Using energy and emissions taxation to finance labor tax reductions in a multi-sector economy. Energy Economics, 115, 106381.

Nordhaus, W.D. 2017. “Evolution of Assessments of the Economics of Global Warming: Changes in the DICE model, 1992–2017”. Climatic Change 148 (4): 623-40.

Writing + or ++ in this column denotes a decrease of emissions, i.e. an increase in environmental quality, and writing ̶ or ̶ ̶ denotes an increase of emissions, i.e. a decrease of environmental quality, while writing 0 denotes a negligible reaction in emissions dynamics.