Disclaimer: The analyses, opinions, and findings expressed in this policy brief are those of the authors and do not necessarily reflect those of the Banco de Portugal or the Eurosystem. The analysis was conducted exclusively during Ana’s tenure at Banco de Portugal, and therefore any views expressed are solely those of the author(s) and cannot be taken to represent those of the Bank of England or to state Bank of England policy. This policy brief should therefore not be reported as representing the views of the Bank of England or members of the Monetary Policy Committee, Financial Policy Committee or Prudential Regulation Committee.

Affiliation of Ana Pereira at the time when the paper was written: Banco de Portugal and Lisbon School of Economics & Management (UL).

Assessing the interaction of structural and cyclical capital instruments under different adverse shocks is paramount for the conduct of macroprudential policy. Our assessment of this interaction is based on the DSGE model of Clerc et al. (2015) calibrated to the Portuguese economy. We show that an increase in capital requirements from a baseline level, regardless of their nature, enhances the resilience of the banking sector and reduces the impact of the shocks on the well-functioning of the banking sector, avoiding amplification effects. Results also indicate that capital requirements can be more effective if distress emerges from within the financial system and countercyclical capital buffers help counter the pro-cyclicality in the financial system during distress. These insights support the conclusion that structural and cyclical capital instruments can be considered strategic complements as they reinforce each other’s policy goals.

Introducing regulatory capital requirements brings about both costs and benefits to the financial system and more broadly to the economy. On the one hand, capital requirements minimise the possibility of bank failure, as they make the banks more resilient and better equipped to absorb losses from adverse shocks originating either in the financial system or in other parts of the economy. Furthermore, those requirements act as a backstop to the banks from taking excessive risk. All in all, higher capital requirements increase banks’ resilience and mitigate the procyclicality of leverage, thereby reducing the economic costs of financial crises. On the other hand, if most banks choose to comply with higher capital requirements chiefly by reducing credit supply instead of effective increases in capital, then more stringent capital requirements may negatively affect economic activity. Nevertheless, it is widely accepted that, up to certain levels, the long-term benefits of capital increments exceed their costs, with a higher marginal benefit from increasing capital requirements when the capital ratios are low. An adequate level of capital requirements depends on the prevailing level of capital requirements and should be set at a level that maximises net benefits.

While the net benefits of increasing capital requirements have been extensively discussed in the literature, there are other policy questions for which research is still limited. One such policy question is the effects of the interaction between prudential policy instruments, in particular, between macroprudential policy instruments that differ in their policy goals. Also, research is limited in what concerns the circumstances in which economic agents may benefit most from imposing higher capital requirements on the banking sector. A better understanding of these issues maximises the effects of macroprudential policy while limiting its unintended effects.

Our work aims to shed light on both these questions by assessing the interaction of structural and cyclical capital instruments in the event of different shocks. The analysis is conducted through the lens of the DSGE 3D model of Clerc et al. (2025) calibrated to the Portuguese economy. The choice of the 3D model is justified by the set of financial distortions embedded in the framework that provides a robust rationale for the introduction of microprudential and macroprudential policies based on capital instruments. Details about the model and the calibration approach can be found in Lima et al. (2023).

In the EU capital regulation framework, all capital-based instruments imply higher absorption capacity. Nonetheless, they are linked to different policy goals, which influences their design and modality of application. While cyclical capital requirements create resilience against risks associated with the financial cycle, structural capital requirements are meant to increase resilience against structural vulnerabilities of the financial system. For example, time-varying capital buffers (e.g. Countercyclical Capital Buffer) should be built up in periods of increasing systemic risk from excessive credit growth and released upon a negative shock that may disrupt the flow of credit to the economy. As such, they are designed to lean against the wind and reduce the likelihood of a worse-than-expected economic outcome. In turn, structural buffers (e.g. Capital Conservation Buffer and G-SII/O-SII buffers) should be applied to mitigate systemic risk of a more permanent nature that makes the financial system more vulnerable to shocks. They are thus designed to reduce the likelihood of a bank failure that could amplify the effects of a shock, which contrasts with the goal of time-varying capital buffers.

Provided with a calibration for the model, we run two policy simulation exercises to assess (i) how strengthening the resilience of the financial system through higher capital requirements mitigates the impact of shocks and limits the potential for amplification effects, and (ii) how the interaction of distinct policy instruments affects the transmission of shocks. In the first simulation exercise, we assess the effects of imposing exclusively higher structural bank capital requirements on a set of financial and macroeconomic variables, while in the second simulation exercise, we assess the effects of imposing simultaneously structural and cyclical capital requirements on the same set of variables.

Policy simulation exercises are based on two adverse scenarios, each one corresponding to a different shock that impels the financial system and the economy to deviate from an equilibrium state. Firstly, we consider a scenario of financial turbulence that consists of a shock to the risk of banks’ return. This shock will increase the probability of bank default, causing distress in the banking sector. Then, we consider a scenario of economic slowdown unfolding from a shock to the production factors. This shock will reduce economic activity and might undermine the expected returns of economic agents, jeopardising their capacity to fulfill their financial obligations. The aim is to compare the stabilising effect of more resilient financial systems under these two distinct shocks: one that first impacts the financial system and then propagates to the economy vis-à-vis the other shock that starts by directly affecting the economy and then spills over to the financial system.

To assess the effectiveness of structural capital requirements in mitigating the impact of shocks, we compare two economies that differ on the level of structural capital requirements before the shock. A benchmark economy in which capital requirements are set at the calibrated structural level of 4.96% of risk-weighted assets (RWA), and an economy featuring a 1 percentage point higher level of structural capital requirements, set at 5.96% of RWA.

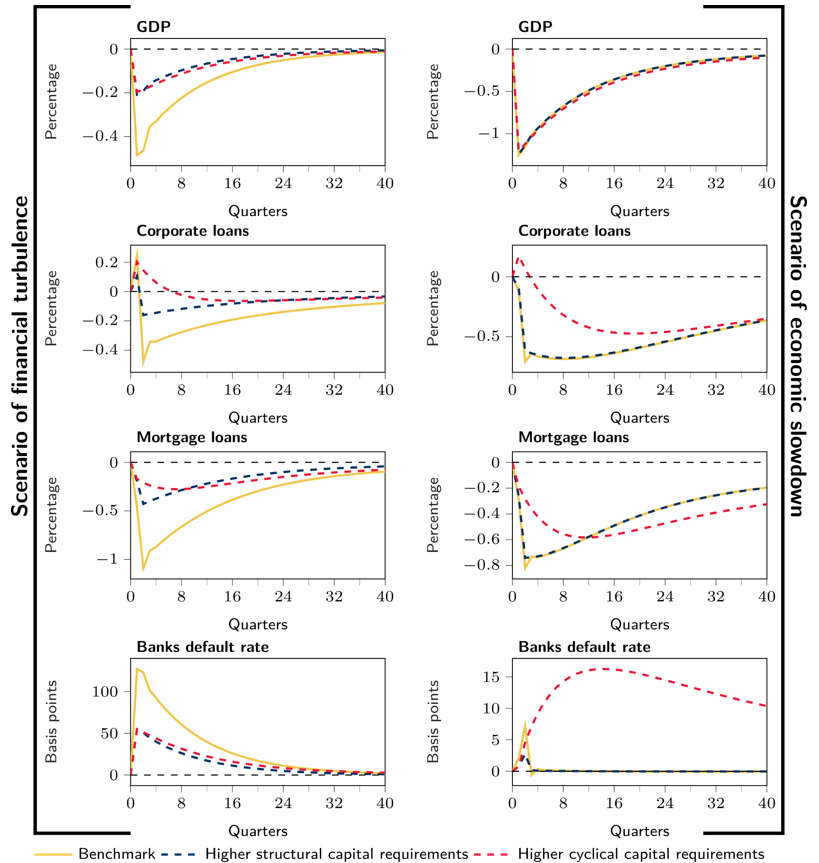

Figure 1 displays the deviation from an equilibrium state for a set of key variables under the scenarios of financial turbulence (left-hand side) and economic slowdown (right-hand side).

Notes: The solid yellow line illustrates how the benchmark economy would evolve under a scenario of financial turbulence or economic slowdown, the dashed blue line displays the response of the economy with higher starting structural capital requirements, and the dashed red line displays the response of the economy with higher starting cyclical capital requirements.

Three main conclusions emerge from our analysis of the impact of higher structural capital requirements.

A more resilient banking sector, i.e., subject to higher capital requirements, is able to better withstand the impact of adverse shocks, regardless of their origin, although it is much more effective in mitigating its impact on the real side of the economy if the distress is triggered by the financial system. In this latter case, the lower probability of bank default in the higher structural capital requirements economy vis-à-vis the benchmark economy brings deposit funding costs down and dominates the higher costs with equity to be borne by the banks following the shock (left-hand side of Figure 1). Consequently, the impact on lending and output is lower and the economy tends to converge faster towards the steady state vis-à-vis the benchmark case.

Second, improving the resilience of banks via a tightening of structural capital requirements helps curbing the spillover effects of economic shocks to the financial system avoiding amplification effects, since the effects on the banks’ default rate are more contained under the higher structural capital requirements case vis-à-vis the benchmark economy (right-hand side of Figure 1).

Third, results indicate that the economy also benefits from a more resilient banking sector, as less constrained total credit moderates, to some extent, the negative impact on output of shocks arising from the rest of the economy. Against this background, there are benefits stemming from a more resilient banking sector. Nonetheless, the source of the disruption is a key aspect to consider when assessing the effectiveness of capital regulation, particularly in what concerns the mitigation of the feedback loops between the financial system and the economy. As clearly shown in the context of the COVID-19 pandemic, a resilient banking sector is also a key condition for the success of other policy measures, such as monetary and fiscal policies.

Finally, we evaluate the effectiveness of time-varying capital instruments, together with structural ones in mitigating the effects of distinct shocks. With this purpose, we add to the previous analysis a third economy subject to the calibrated level of structural capital requirements plus time-varying capital requirements (dashed red line in Figure 1). Specifically, we assume that prior to the shock a surge in cyclical systemic risk motivated the accumulation of the countercyclical capital buffer of up to 1%. This additional resilience is time-varying and thereby is now available to be used by the banks following a perturbation to the economy or financial system. To resemble the mechanism introduced in the European macroprudential framework for the countercyclical capital buffer, this time-varying component reacts countercyclically to the deviation of total credit from its long-term average.

The results highlight the drivers for the use of macroprudential capital instruments and the importance of considering countercyclical capital instruments in combination with structural ones.

First, when shocks emerge from inside the financial system, most of the improvements come from the increased resilience that higher capital requirements provide, regardless of their structural or countercyclical nature (left-hand side of Figure 1). Higher capital requirements diminish the potential impact of the shocks on the functioning of banks and consequently on the flow of funds supplied to the economy, thereby reducing the need to use the countercyclical component of capital requirements. This result highlights the strategic complementariness of the two capital-based instruments, but also the presence of substitutability effects.

Second, in the presence of a stress event with origin in the economy, while higher structural capital requirements reduce potential contagious and feedback effects from the financial system, the release of the countercyclical buffer smooths the disturbances in the credit supplied by banks, attenuating the effects on output (right-hand side of Figure 1). Despite the marginal effect on GDP, it helps to alleviate the burden on agents’ financing costs. Nonetheless, the flexibility granted in reducing capital requirements should be wisely used as it might temporarily increase the banks’ default rate with potential costs for households in the form of insurance deposits. Therefore, the transmission effects of countercyclical capital requirements entail both benefits and costs. To mitigate the costs of releasing countercyclical capital requirements, our results suggest that the capitalisation of the banking sector may be improved through the combination of countercyclical capital buffers and structural ones, ensuring that the banks’ default rate remains at low levels, despite its increase as a result of the release of the countercyclical buffer.

Third, the results highlight that the usefulness of countercyclical capital requirements is closely linked to the source of the shocks, similar to what we concluded for the structural capital requirements. If shocks have a root in the economy, their usefulness will be noticed in the mitigation of the pro-cyclical behaviour of banks. If they arise in the financial system itself, their effectiveness is mainly related to the improved resilience of the banking sector along the build-up phase, determining a higher absorption capacity of the banking sector. In case systemic risk materialises within the financial system, banks will be more able to fulfill their role as financial intermediaries, and the need for using the flexibility provided by the release of the countercyclical buffer is reduced.

Overall, our results suggest that the countercyclical capital buffer achieves the policy objective of reinforcing the resilience of the banking sector in the expansion phase of the credit cycle, helping the banks to better withstand the negative effects of adverse shocks. In the contraction phase of the credit cycle, this instrument smooths the crunch in credit flows, mitigating the feedback loops between the banking sector and the rest of the economy.

Our findings have implications for the conduct of macroprudential policy. Foremost, they provide support for combining the two types of policy instruments and reaping the benefits of exploring their substitutability – in increasing resilience in the build-up phase that avoids amplification effects – and complementarity – in smoothing the effect on credit in a crisis event. However, the increase in capital requirements by the policymaker is not unbounded. After a certain capital ratio level, the net benefits of further increases become negative as shown by the literature.

The effectiveness of a better-capitalised banking sector is highly enhanced when the stress event emanates from the financial system itself. The source of distress has important implications for the effectiveness of capital instruments and their potential limitations for the mitigation of feedback loop effects between the financial system and the rest of the economy. Prudential policies are not meant to be the first line of defense to address, for example, the effects stemming from aggregate demand shocks, this is within the scope of other policy areas. Nevertheless, a more resilient banking sector prevents the amplification of shocks reinforcing the effects of other more adequate policies not considered in the analysis.

Finally, the results also suggest that structural and cyclical capital-based instruments are strategic complements. Although they target different policy goals, they both reinforce the resilience of the banking sector and its capacity to withstand shocks. Moreover, if (both micro and macroprudential) structural requirements are set in an appropriate manner, the space for using the countercyclical capital buffer in the event of a shock is wider, since the potential costs associated with an increase in the bank default rate will be lower.

Clerc, Laurent, Alexis Derviz, Caterina Mendicino, Stephane Moyen, Kalin Nikolov, Livio Stracca, Javier Suarez, and Alexandros P. Vardoulakis (2015). “Capital Regulation in a Macroeconomic Model with Three Layers of Default.” International Journal of Central Banking, 11(3), 9–63.

Lima, Diana, Duarte Maia, and Ana Pereira (2023). “Structural and cyclical capital instruments in the 3D model: a simulation for Portugal.” Banco de Portugal Working Paper, No. 15.