How important is the planning horizon of households for the effects of fiscal plans? We address this question through the lens of a New-Keynesian model where households are boundedly rational and plan over a finite number of periods. We show that the planning horizon affects the medium-run cumulative multipliers significantly. Government spending cumulative multipliers increase with the horizon while labor tax cumulative multipliers drop, in absolute terms. In light of the recent debt crisis in the Euro Area, we look at spending cuts and labor income tax hikes. In line with the empirical literature, we find in our benchmark calibration that spending cuts are less recessionary than tax hikes. Looking at the interaction between the planning horizon and the persistence of the fiscal plans, we find that spending cuts become less recessionary while tax hikes more recessionary when the persistence of fiscal plans rise, and that this effect is amplified by shorter planning horizons. Introducing wage stickiness, we show that for very sticky wages, tax hikes become less recessionary than spending cuts, but that intermediate levels of wage stickiness have the opposite effect on fiscal multipliers when planning horizons are finite.

Over the last two years, major central banks have been undergoing a strategy review. The latter touches upon the efficiency of the various instruments, their alternative specifications as well as the importance of alternative expectations formation mechanisms other than rational expectations. This paper focuses on the importance of expectations and the length of the planning horizon of the private sector. Specifically, we question how does the transmission of shocks change when agents are no longer rational and do not form expectations for the infinite future as is the case in benchmark structural models that have been used traditionally in central banking.

We build a closed economy New-Keynesian model, allowing for monetary and fiscal policy interactions, where agents are boundedly rational. Their bounded rationality amounts to planning over a finite number of periods in the future. Specifically, agents are fully aware that there are periods outside their horizon but their cognitive limitations do not allow them to plan and forecast for the periods outside their planning horizon. Instead, agents can plan and form expectations only for their short- to medium-run horizon and not for the infinite future. For later periods, households use a simple heuristic where they realize that having more wealth at the end of their planning horizon will allow them to consume more in the periods after their horizon. Other than that, agents assume that the economy will be at the steady state after their planning horizon.1 It turns out that the accuracy of agent’s forecast for periods within their horizon crucially depends on the accuracy of this assumption. If their beliefs about the end of their horizon turn out correct then their forecasts are not far from those of a rational agents with an infinite planning horizon. If instead, the economy will actually considerably deviate from steady state at the end of the horizon, then agents will have considerable forecast errors within their planning horizon. Clearly, the more persistent the shocks hitting the economy, the longer stays the economy away from the steady state and the more likely it is that agents make forecast errors. As regards the rest of the model, the central bank sets its policy rate according to a Taylor rule, while the government adjusts lump-sum taxes to stabilize debt.2

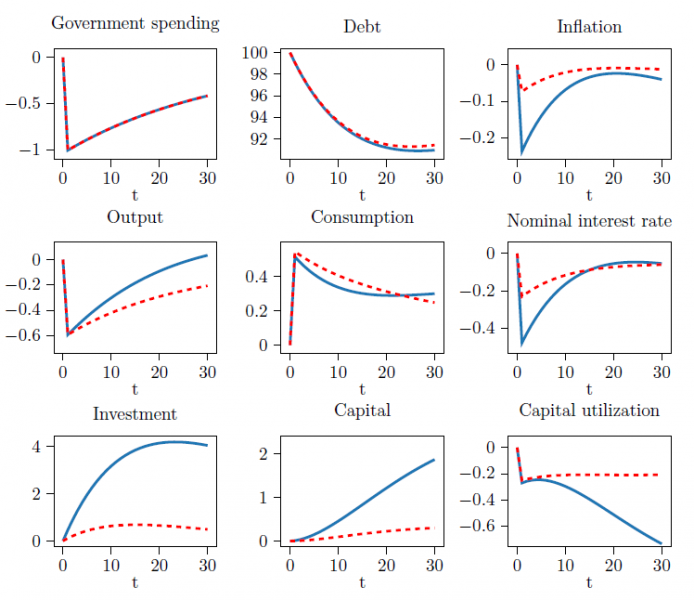

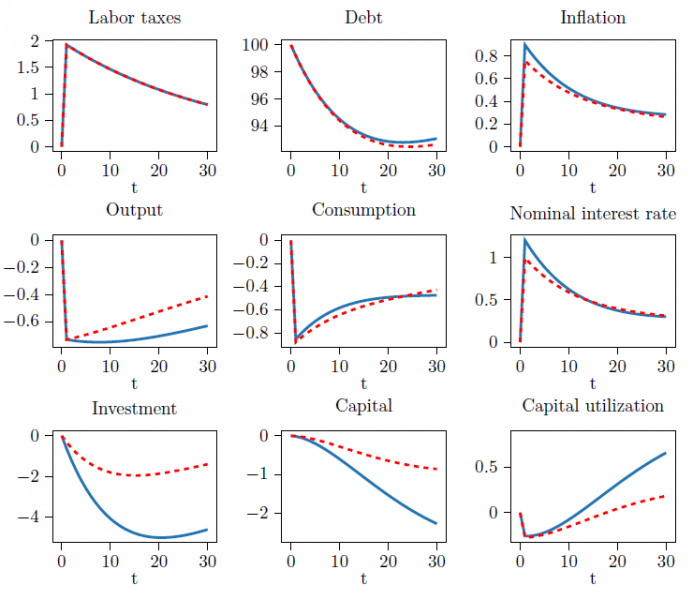

We restrict our focus on the effects of a cut in government spending and on a rise in labor income tax. In each case, we consider two scenarios, namely one where agents plan for the next 20 quarters (blue solid lines) only and another where they plan for the next 100 quarters (red dashed lines).

In Figure 1, we consider a one standard deviation cut in government spending. The cut in spending is assumed to be persistent.3 Independently of the planning horizon, the drop in government spending leads to a persistent fall in output and to a reduction in the debt level. At the same time, there is an increase in consumption and a fall in inflation and the nominal interest rate. Even though capital utilization falls as a consequence of the recession, lower real interest rates lead to a slight increase in investment and capital. In Figure 2, we consider a rise in labor income tax. The size of the increase is scaled so that the impact effect of the tax hike on the primary balance is equal to that of a one standard deviation cut in government spending. The persistently higher labor income taxes reduce the stock of debt, but lead households to cut on consumption and on their labor supply, and firms to increase prices. Given an active monetary policy, the central bank raises the interest rate to combat the inflationary pressures.

Figure 1: Cut in government spending. Blue solid lines depict the impulse responses when planning horizon is 20 quarters. Red dashed lines depict the impulse responses when planning horizon is 100 quarters.

The resulting increase in the real interest rate and in capital utilization reduces investment, so that the capital stock goes down. These eventualities lead to a persistent fall in output.

Next, we turn to the comparison between the impulse responses of long planning horizons and those of shorter (20 quarters) planning horizons. The differences that arise here, are mainly driven by the differences in the expectations of agents with different planning horizons. A finite planning horizon not only limits an agent’s ability to make optimal decisions but also her ability to form rational expectations. This is because forming fully rational expectations requires taking account of the future evolution of all variables up to infinity. Households with a planning horizon of 100 quarters form more accurate expectations as they process more information by sophistically deliberating on the evolution of the economy over the coming 100 periods.

Figure 2: Increase in labor income tax. Blue solid lines depict the impulse responses when planning horizon is 20 quarters. Red dashed lines depict the impulse responses when planning horizon is 100 quarters.

In particular, a planning horizon of 100 is so long that the shock and its effects are likely to have already dissipated long before the end of the planning horizon. Therefore, their assumption that the economy lies at the steady state after the end of their horizon proves to be correct and their expectations almost coincide with rational expectations.

Agents with a planning horizon of 20 quarters, on the other hand, have the cognitive ability to sophisticatedly think about what will happen for the next 20 quarters only. Therefore, when forming expectations about what happens 20 quarters from now, they ignore any effects on period 20 variables that arise due to expectations formed from period 20 onwards. This is because they lack the cognitive ability to form accurate expectations about what will happen in these periods and hence on what expectations formed in period 20 about periods 21 to 40 should be. Since the model is highly persistent, all variables are likely to deviate from the steady state in periods 21 through 40 significantly. Not being able to take this into account biases the expectations of agents with short planning horizons. In particular, it turns out that households with a planning horizon of 20 periods overestimate the effect that fiscal shocks will have on inflation and the nominal interest rate. Therefore, for the case of a negative shock to government spending, they expect a lower path for the real interest rate than the agents with rational expectations. That explains why the recovery is faster when planning horizons are shorter. The opposite holds under labor income tax hikes. Agents with shorter planning horizons overestimate the inflationary impact of tax hikes, and hence expect even higher interest rates. This makes tax hikes more contractionary when planning horizons are shorter. But, there are also differences in the intertemporal effects. Agents with longer planning horizons take into account a longer future path of the interest rate. That is, they also account for the fact that the interest rate will be lower in the longer-run. In other words, they account for the fact that the present value of their wealth will rise in the longer-run. As a result, they frontload these future events in their current decisions. Consequently, their consumption recovers faster while investment contracts less. This allows for a milder contraction compared to the case of shorter horizons.

The paper shows that the planning horizons of households matter to a great extent for the transmission of shocks. The shorter the planning horizons, the stronger the effects of shocks on inflation and thereby the more de-anchored inflation (and output) expectations. This effect makes the policy objective of the central bank more challenging, especially in times when it seeks to boost the economy through expectational effects. Structural models featuring agents with planning horizons that are finite can lead to results that are closer to the salient features of actual data. This is because, they allow for forecast errors that affect economic behavior substantially. However, the results should be treated with caution as the persistence of shocks plays a key role for the magnitude of the effects.

Angeletos, George-Marios, and Chen Lian. 2018. “Forward Guidance without Common Knowledge.” American Economic Review 108 (9): 2477–512.

Farhi, Emmanuel, and Iván Werning. 2019. “Monetary Policy, Bounded Rationality, and Incomplete Markets.” American Economic Review 109 (11): 3887–928.

Gabaix, Xavier. 2020. “A Behavioral New Keynesian Model.” American Economic Review 110 (8): 2271–327.

García-Schmidt, Mariana, and Michael Woodford. 2019. “Are Low Interest Rates Deflationary? A Paradox of Perfect-Foresight Analysis.” American Economic Review 109 (1): 86–120.

Iovino, Luigi, and Dmitriy Sergeyev. 2017. “Quantitative Easing without Rational Expectations.” Unpublished manuscript.

Lustenhouwer, Joep, and Kostas Mavromatis. 2021. “The Effects of Fiscal Policy when Planning Horizons are Finite.” De Nederlandsche Bank Working Paper No. 717.

This assumption is not very far from the answers of respondents in surveys. In particular, in many surveys, when asked about what they believe inflation will be in, say, 5 years from the current date, respondents believe inflation to be at the target of the central bank.

There is a growing literature on models where agents plan and forecast over a finite number of periods to the future. Our approach is very close to Woodford (2018) who also introduces agents that plan over a finite number of periods. The key difference between his approach and ours is that agents in our framework plan about the same number of periods at every date. In Woodford instead the end of planning horizon is kept fixed. As such, agents planning horizons are assumed to shorten as time moves closer to the end of the planning horizon. Other similar approaches in the literature include cognitive discounting (Gabaix, 2020) or level k-thinking (see, Angeletos and Lian, 2018; Fahri and Werning, 2019, Garcia-Schmidt and Woodford, 2019 and Iovino and Sergeyev, 2017).

Government spending follows an AR(1) process with autoregressive parameter set to 0.8. This number falls within the posterior intervals from similar structural models estimated for the US.