Historically high inflation prompted central banks all over the world to tighten monetary policy. However, their ability to reduce inflation will depend, among many other things, on the behavior of fiscal policy. We estimate the effects of monetary policy shocks across contractionary and expansionary fiscal regimes in the euro area. We find that a contractionary monetary policy shock only has a statistically significant downward effect on inflation when it occurs in the contractionary fiscal regime. When fiscal policy is expansionary, the inflation response to a monetary tightening is statistically insignificant. Similarly, a monetary expansion only raises inflation in the expansionary fiscal regime. These results underline the importance of the fiscal stance for the monetary transmission mechanism and emphasize the need for more enhanced coordination between monetary and fiscal policy in order to return inflation from its current high level down to the ECB’s inflation target.

The monetary and fiscal policy mix in the euro area varied strongly in the past two decades, with different economic results.1 In response to the global financial crisis of 2008-9, the ECB engaged in a prolonged spell of expansionary monetary policy, while many member states (especially those confronted with high levels of public debt) pursued contractionary fiscal policies. This asynchronous mix of monetary and fiscal policies coincided with a slow economic recovery and inflation often running below target. The policy response to the COVID-19 pandemic has been much more harmonious, with fiscal and monetary policy having been both expansionary, which aided the rapid economic recovery. Today, as inflation is running far above the ECB’s inflation target, monetary policy started its tightening cycle, whereas fiscal policy seems to be expansionary, as governments seek to protect household’s purchasing power from rising energy costs through broad fiscal support programs (Schnabel, 2022). Therefore, in pursuing their own respective goals, fiscal and monetary policy have not always been in sync and occasionally worked against each other, which has important implications for the performance of monetary policy (see also Reichlin et al., 2023).

In order to assess if and to what extent the fiscal stance undermines or supports monetary policy in ensuring price stability, we estimate the effects of monetary policy shocks on inflation and output growth in the euro area across two distinct fiscal regimes (Kloosterman et al., 2022). These two fiscal regimes are labeled as either ‘contractionary’ or ‘expansionary’, and their characterization is based on the change in the structural primary budget balance. We use a logistic function to assign a probability that a member state finds itself in the expansionary and contractionary fiscal regime in any particular point in time. Then, using the monetary shocks identified by Jarocinski and Karadi (2020) and quarterly data from 1999Q1 to 2019Q4, we estimate a smooth transition local projection model (as suggested by Jordá (2005)) for a panel of 10 euro area countries.2 This model allows us to estimate the response of inflation and output growth to the monetary policy shock conditional on being in one of the two fiscal regimes.

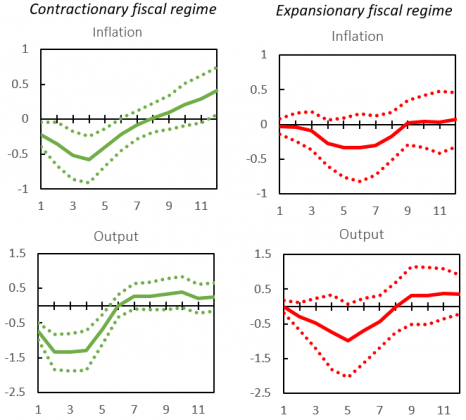

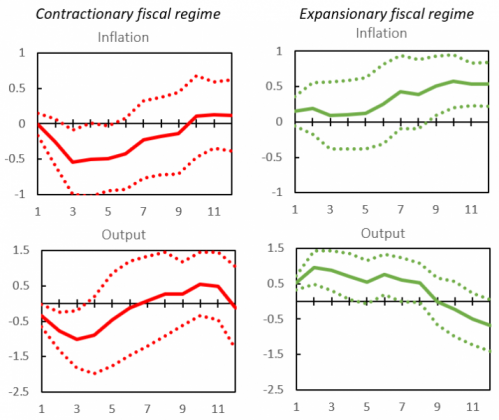

Our empirical results show that a contractionary monetary policy shock (i.e. an exogenous rise of the policy interest rate) only has a statistically significant downward effect on inflation and output growth when the shock occurs in the contractionary fiscal regime (Figure 1, left column). If, instead, the contractionary monetary policy shock occurs in the expansionary fiscal regime, the responses are statistically insignificant (Figure 1, right column). Similarly, an expansionary monetary policy shock only has a statistically significant positive effect on inflation and output growth when the fiscal stance is expansionary as well (Figure 2, right column). Interestingly, an expansionary monetary policy shock conducted in times when fiscal policy is contractionary actually results in a reduction of inflation and output growth (Figure 2, left column). These empirical results underscore the importance of coordination between monetary and fiscal policy for the transmission of monetary policy: only when monetary and fiscal policy move in tandem does monetary policy have the expected effects.

Figure 1: Responses to a contractionary monetary policy shock

Notes: The figure shows the estimated impulse response functions to a contractionary monetary policy shock, conditional on being in the contractionary fiscal regime (first column) and expansionary fiscal regime (second column). The dashed lines reflect the 90% confidence interval based on Driscoll-Kraay standard errors. The horizontal axis measures quarters.

Figure 2: Responses to an expansionary monetary policy shock

Notes: The figure shows the estimated impulse response functions to an expansionary monetary policy shock, conditional on being in the contractionary fiscal regime (first column) and expansionary fiscal regime (second column). The dashed lines reflect the 90% confidence interval based on Driscoll-Kraay standard errors. The horizontal axis measures quarters.

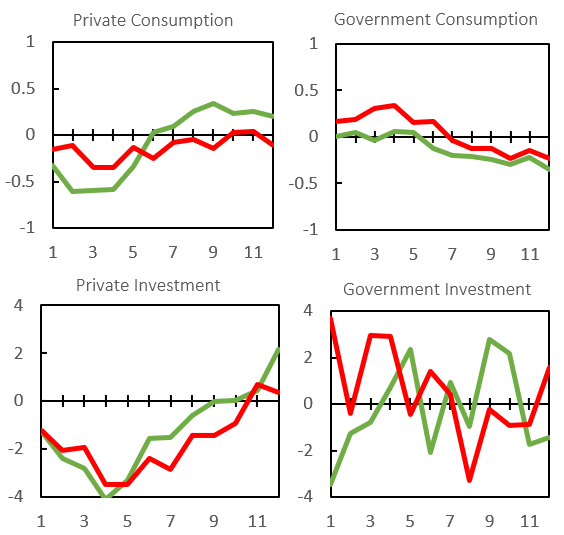

Our empirical findings can be explained by the fact that fiscal policy can affect aggregate demand and inflation, both directly and indirectly, in ways that either amplify or offset the effects of monetary policy. Beyond this type of interaction between monetary and fiscal policy, which can be illustrated using the well-known static IS-LM model, additional channels through which monetary and fiscal policy interact arise in more elaborate and dynamic macroeconomic models. For instance, in standard New Keynesian models, a temporary interest rate hike triggers an intertemporal substitution effect that induces households to save more today and consume more tomorrow. However, Caramp and Silva (2022) show that, in isolation, this effect only affects the timing of consumption, but not its present value. What causes inflation to fall in most dynamic macroeconomic models is an accompanying fiscal contraction (explicitly modelled or not) that yields a negative wealth effect (e.g. a rise in taxes that lowers labor income) which in turn lowers consumption in present value terms. Without this (sufficiently large) fiscal contraction, inflation could actually rise due to a positive wealth effect arising from an increase in households’ interest receipts that raises expected lifetime income and, thereby, consumption (provided the revaluation effect of the interest rate hike on households’ assets is not too strong).3,4 We find some support in favor of this wealth channel explaining the interaction between monetary and fiscal policy shown in Figures 1 and 2: whereas the response of private consumption to a monetary policy shock depends strongly on the fiscal regime, the responses of public consumption and (public and private) investment are not significantly different across the two regimes (Figure 3). Therefore, the asymmetric responses to the monetary policy shock across fiscal regimes are most likely driven by private consumption, which is consistent with the predictions of the wealth channel.

Figure 3: Responses of private and public consumption and investment to a contractionary monetary policy shock

Notes: the horizontal axes measures quarters. The green lines show the response in the contractionary fiscal regime and the red lines show the response in the expansionary fiscal regime.

Without being properly aligned with fiscal policy, monetary policy may find it more difficult to achieve price stability. Our empirical results imply that the recently announced and implemented fiscal measures in the euro area aimed to safeguard households and firms against surging energy costs can significantly undermine the central bank in achieving its inflation target if these measures translate into an overall (and persistent) expansionary fiscal stance. From that perspective, it would be more prudent for governments to engage in more targeted and temporary fiscal policies, implement support measures that are budget-neutral or at least sufficiently backed by future primary surpluses, and/or pursue fiscal policies that support and expand the supply-side of the economy (e.g. public capital investments and labor market policies).

Caramp, N. and Silva, D. H. (2022). Fiscal policy and the monetary transmission mechanism. Mimeo.

Corsetti, G., Dedola, L., Jarociński, M., Maćkowiak, B., & Schmidt, S. (2019). Macroeconomic stabilization, monetary-fiscal interactions, and Europe’s monetary union. European Journal of Political Economy, 57, 22-33.

Jarociński, M. and Karadi, P. (2020). Deconstructing monetary policy surprises— The role of information shocks. American Economic Journal: Macroeconomics, 12(2):1–43.

Jordà, Ò. (2005). Estimation and inference of impulse responses by local projections. American Economic Review, 95(1):161–182.

Kloosterman, R., Bonam, D. and van der Veer, K. (2022). The Effects of Monetary Policy across Fiscal Regimes. De Nederlandsche Bank Working Paper No. 755.

Reichlin, L., Ricco, G., and Tarbé, M. (2023). Monetary-fiscal crosswinds in the European Monetary Union. European Economic Review, 151: 104328.

Schnabel, I. (2022). Finding the right mix: monetary-fiscal interaction at times of high inflation. Keynote speech by Isabel Schnabel, Member of the Executive Board of the ECB, at the Bank of England Watchers’ Conference.

See Corsetti et al. (2019) for a discussion on the recent mixes of monetary and fiscal policy in the Eurozone.

The countries in our sample are Austria, Belgium, Netherlands, Germany, France, Spain, Portugal, Luxembourg, Italy and Finland.

The bond revaluation effect is more likely to dominate the effect arising from higher interest rate receipts if the duration of the households’ bond portfolio (or of other types of assets, such as equities and real estate) is relatively long.

Since the direct wealth effects of monetary policy work through changes in asset prices and returns, they will mostly affect high-income households and/or households that are not liquidity or credit constrained. Lower- to middle-income households and/or households facing binding credit constraints are likely mostly exposed to the indirect wealth effects of monetary policy that work through changes in aggregate demand, employment and labor income.