This Policy Note is based on “The end of free EU ETS rights: Navigating industrial decarbonization”, RaboResearch, 2024.

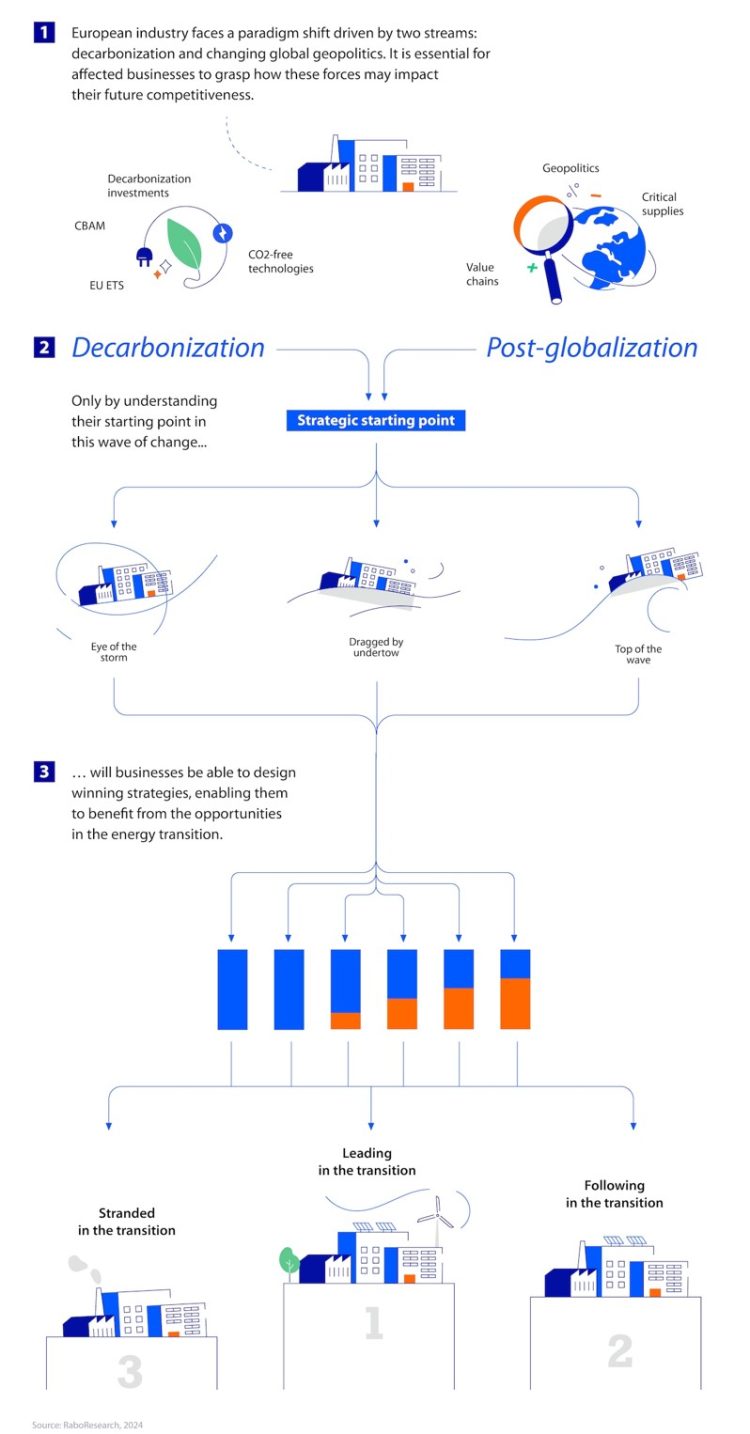

It is an existential period for EU industry, as carbon policies are set to get really serious in the middle of a global geopolitical shift. Navigating these challenging times will require strategic awareness of where companies stand in relation to their competitors and, potentially, new competing sectors. We propose a map for each of the different starting positions that industry firms can adopt by looking at critical industrial decarbonization variables: carbon and energy intensity, investment options, and the expected effects of the Carbon Border Adjustment Mechanism on sectorial trade patterns. We also illustrate how different carbon rights purchases and/or decarbonizing investment strategies may or may not harvest significant savings against a business-as-usual scenario.

EU carbon policies are far from being the only source of change for EU industry. Geopolitical, regulatory, market, and financial forces are converging to trigger a technological shift of a size not seen since the industrial revolution. EU companies are urged to understand the new surroundings as they unfold and whether traditional entry barriers are being diluted or wiped out. Every industry player is going to be affected, one way or the other.

Under the “traditional” competitive pressures, relevant forces of change bloom. Think of increasing restrictions in the transport and global supply chains, ongoing or incipient trade wars, or rising concerns about the spread between input costs. While such dynamics, under what we term a “post-globalization economy,” may become equally or even more relevant than the new carbon policies in the middle term, they exceed the scope of this article.

Focusing on the carbon-related change forces, we see that what used to be the more complex battlefield of the biggest players must now permeate the thinking of every company covered by the European Union Emissions Trading System (EU ETS). Our first article assessed the potential increase that median companies in key industrial sectors can expect in their carbon bills for their emissions under a business-as-usual scenario. In our second piece, we described the different ways in which the new EU industrial carbon policies may affect the competitiveness of EU ETS-covered companies and, as a result, trade.

Ultimately, if companies want to remain active, they need to decide how and when to decarbonize. In this article, we propose a framework to guide companies as they design their answers (see figure 1).

Figure 1: Building a corporative decarbonization path

Source: RaboResearch 2024.

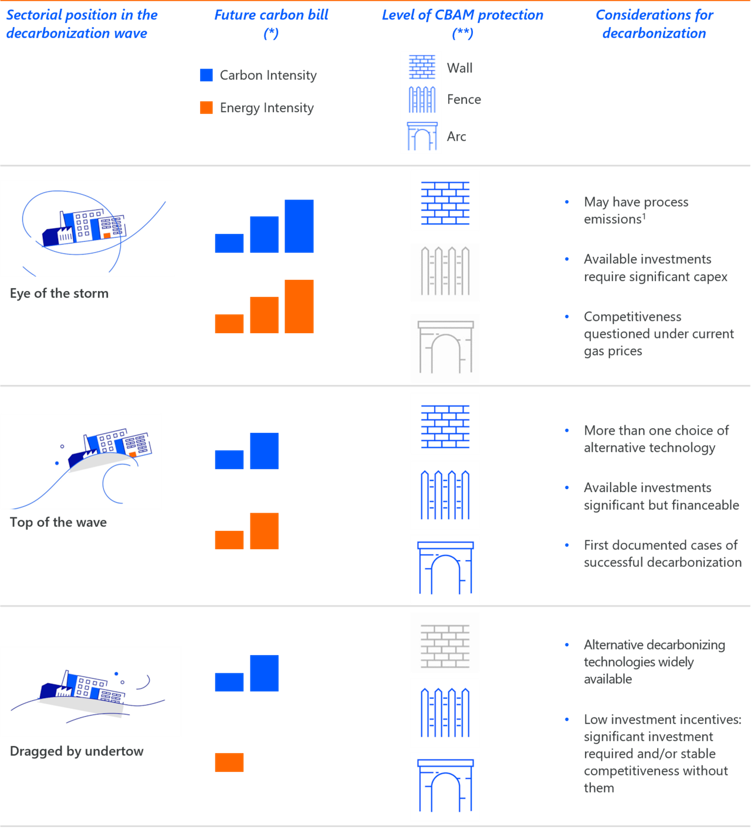

We begin by outlining three different types of starting positions from which companies may face industrial decarbonization, based on key carbon variables and the expected impact of the new EU carbon policies. According to our proposal, firms may find themselves starting in the eye of the storm, likely to be dragged by the current, or surfing on top of the wave. Each type can benefit from a different weighing of the context. We discuss their trademarks and, to complete the overview of choices ahead, assess which savings companies can realize in their carbon bills through several basic strategies.

With both elements in mind, we conclude by discussing the particularities of each starting position’s decarbonization decision-making process. We then wrap up with a summary of this series of articles to clarify the essential perspective on the EU’s industrial carbon policies to help companies navigate the changing tides, at least its carbon currents.

Companies should develop an awareness not only of their future decarbonization challenges, but also those of their competitors and connected sectors. There will be as many decarbonization processes as there are companies. But by looking at certain variables, one can identify common threads and patterns that can prove an insightful frame for any decarbonization strategy. Valuable data for this purpose (such as the carbon dioxide emissions intensity of key industrial sectors, or metric ton CO2/metric ton product) is publicly and widely available from leading organizations, such as the World Economic Forum, the International Energy Agency, and the Joint Research Center.

More specifically, by exploring the carbon and energy intensities (the main drivers behind the expected increase in corporate carbon bills) and the likely effect of the Carbon Border Adjustment Mechanism (CBAM) on the sector’s trade patterns, and by contrasting both of them with the available decarbonization investments, we can distinguish three main starting points and subsequent decarbonization processes:

Table 1: Landscape of industrial decarbonization positions

(*) As illustrated in the first chapter of this trilogy, the carbon bill of a median EU ETS-covered company under a BAU scenario can be expect to grow between 2.5 and 20 times. The extent of the increase is mainly driven by the company’s carbon and energy intensity. These two factors are a good first indicator of the level of challenge that decarbonization may entail for the company.

(**) The level of CBAM protection is analyzed in the second chapter. Depending on the relevance of the external market and on the comparative carbon intensity for the covered products, the CBAM will result in different levels of protection against trade-related carbon leakage. We named these levels as “wall” (very significant), “fence”(variable depending on the carbon intensity of extra-EU manufacturers), and “arc” (unlikely to be a critical factor to sustain competitiveness).

Source: Rabobank 2024.

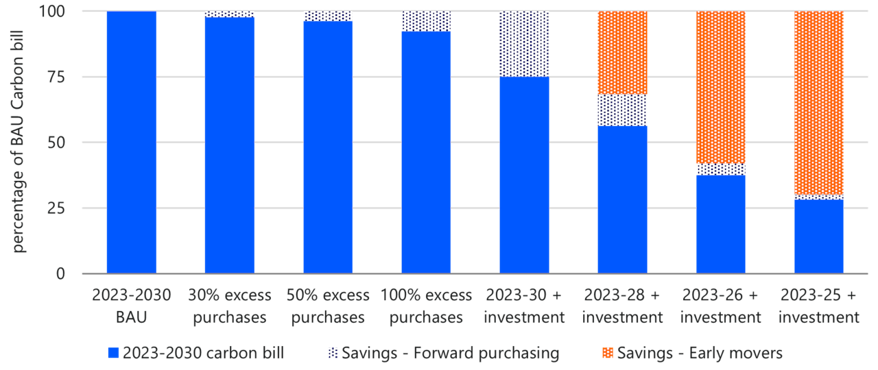

While critical investment decisions to be taken by industry players pile up, the ironing out of small details may result in a later decisive advantage. For example, in our view, an optimized carbon-purchasing strategy should be considered by any company affected by EU industry carbon policies. To illustrate the relevance of such an approach, we have tested the savings that different carbon strategies might achieve.

Consider the EU ETS corporative bill for the 2023-2030 period for an example company. Let’s call it the business-as-usual or “BAU bill.” The BAU bill includes the expected value of the EU ETS carbon emission rights (called EU allowances, or EUAs) that our example company will need to purchase to sustain its activity under the “BAU scenario” every year throughout the 2023-2030 period. The BAU scenario implies a continuity of the pre-Covid activity levels without any decarbonizing investment happening and the implementation of the just-approved phaseout of free EUAs, as described in our previous article. We have tested the effects of two types of strategies:

We ran a scenario analysis comparing the potential reductions in the example company’s carbon bill for the 2023-2030 period from the two types of strategies relative to the BAU bill (see figure 2). Forward purchasing was tested at 30%, 50%, and 100% excess rights acquired annually, and early movers were tested for decarbonization investments carried out in full in 2030, 2028, 2026, and 2025. Companies following the latter strategy could benefit from two saving components: a reduced price for anticipated EUA purchasing (dotted blue) and a volume reduction in the credits that the company would be required to buy (dotted orange).

Figure 2: Example of different hedging strategies’ potential to reduce the full 2023-2030 EUA bill

Source: European Commission, BNEF, Rabobank 2024.

In view of figure 2, some qualitative and tentative conclusions can be drawn regarding purchasing strategies:

It should be noted that both purchasing and hedging strategies should be carefully considered, as there are also risks associated with them. The most prevalent one is that the actual price of future EUAs turns out lower than what a company hedged against. We do note that most trends point toward an upward price curve for EUAs in the medium term, which might make hedging a relatively safe option in this case. However, as recent events in the UK illustrate, policy changes can alter the direction of a policy-dependent market. The purpose of this exercise is to illustrate the importance of understanding how different strategies influence results and decision-making processes. Firms should conduct their own assessments tailored to their unique conditions and not limit themselves to the proposed approaches here.

Once the choices for industrial decarbonization are well understood, foresight analyses, such as those described in our previous articles, will frame the decision-making process for how and when to decarbonize. Naturally, such decisions will differ depending on the starting point:

As described throughout this series of articles, recent regulatory, technological, and geopolitical events cast a wave of unavoidable change over European industry.

One of the main elements of this change on the way to 2030 will certainly be the expected EU ETS-related increasing cost for EUAs. We have illustrated what the financial impact of the proposed regulation could look like and how it may differ across sectors depending on their critical driving factors. While there are common considerations for industrial subsectors as a result of these driving factors, the subsequent decision-making will define what the process results in for each industrial player.

The pricing of carbon in the EU will also affect the trade competitiveness of EU industries. The CBAM may provide some shielding against more carbon-intensive imports from outside the EU. We have also analyzed how this regulation may or may not shape industrial players’ cross-border trade balance. The CBAM might not provide the desired protection in all instances.

Weighing the impact of the EU ETS and the CBAM, we have sketched three types of starting positions for industrial decarbonization. Common grounds can be identified across industry players based on their carbon and energy lock-ins, their trade patterns, and the appeal and maturity of the available decarbonizing investment options. This article has provided guidelines to contextualize the decision-making for each type of situation, explaining the types of dynamics that the different markets will go through in the coming years.

Finally, we have illustrated the convenience and potential expected return for different carbon-purchasing strategies in the 2023-2030 period, working under the assumption that the price of EUAs will continue to increase. In general, in a context of increasing prices, hedging looks like a highly useful complementary tool for those affected by the EU ETS and CBAM, though players shouldn’t forget there are also risks associated with it. Forward purchasing strategies seem to lead to a lower level of potential savings versus early direct investments in decarbonization. Such assessments can help fine-tune the timing of certain investments.

Combining all these elements together results in an overview of the way ahead that no industrial player can afford to ignore. European industry has extremely dynamic years ahead. Internally, the transformation is unavoidable in the current climate and political context. Externally, the survival of an essential element of Europe may be questioned, depending on how geopolitical events develop and, in a broader sense, how Europe finds its place amid the ongoing repositioning.

Decarbonization of European industry is far from a simple isolated puzzle that one can easily assemble. Its resolution requires structured thinking as an essential ingredient for success. Decarbonization is also not the only dynamic that will define the outcome of the transition. In this series of articles, we have illustrated how to deploy the “new carbon-related” strategic factors, but traditional ones (such as transport and global chains, trade wars, spread between input costs, and the impact of climate change on commodities’ yields) will continue to define the playing field. Europe’s quest for strategic autonomy amid post-globalization extends the need for strategic thinking that considers all systems and encompasses the whole economic development and welfare of Europe.

A poorly managed transition may seriously affect the survival of a critical element of European wealth and employment, but properly heading the decarbonization of the economy can unlock historical growth opportunities for a European Union searching for its place in a constantly moving world.

A company’s carbon lock-in can be structural if it’s a chemical result of their production processes, such as the extraction of calcium from limestone. These are the referenced “process emissions.”

Call options are one of the basic hedging tools. They are essentially financial contracts providing the right to buy a certain product (EU ETS emission rights in this context) at a certain price, at a certain point in time.