Disclaimer: This brief is based on the paper entitled “BEAST: A model for the assessment of system-wide risks and macroprudential policies” by Katarzyna Budnik, Johannes Gross, Gianluca Vagliano, Ivan Dimitrov, Max Lampe, Jiri Panos, Sofia Velasco, Louis Boucherie, Martina Jancokova, and was first published as ECB Working Paper No 2855. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank and the Eurosystem.

The Banking Euro Area Stress Test (BEAST), a semi-structural macro-micro model, has been designed to fulfil tasks imposed by the macroprudential mandate of the ECB. The BEAST encapsulates 19 euro area economies, 90 largest euro banks, and dynamic interdependencies between the real economy and the banking sector. Banks are subject to system-wide and bank-specific capital requirements and buffers, liquidity standards, and can be impacted by conventional and unconventional monetary policies. Finally, the model permits stochastic simulations that can infuse its projections with scenario and parameter uncertainty. With its innovative design, the model enhances the methodological toolkit of the ECB, allowing it to conduct sophisticated risk and policy assessment without direct involvement from financial institutions.

In the aftermath of the global financial crisis, regulators set their sights on a more holistic approach to financial supervision, commonly known as the macroprudential perspective. In line with this ambition, the new Basel III regulatory framework has overhauled capital and liquidity requirements, introduced a host of new macroprudential tools and embraced stress testing to examine the labyrinthine balance sheets of financial institutions.

Central banks and supervisory agencies, which have adopted these expanded prudential mandates, have encountered a dual analytical challenge: monitoring risks and shaping policies within the realm of financial stability. Systemic risks are inherent in and exacerbated by the financial system. Consequently, to stay ahead of evolving risks, regulators have implemented regulatory stress testing, casting a wide net over many financial institutions. To set the right course for prudential requirements and buffers, regulators assess policies both before (ex-ante) and after (ex-post) implementation. It is a precondition to fine-tune individual interventions and evaluate their success.

At the crossroads of these two analytical tasks lies macroprudential stress testing, a domain focused on detecting and measuring systemic risks. It also can infuse a financial stability perspective into the selection of prudential instruments.

This analytical gap has been addressed by various structural and data-based models, each leveraging its strengths in explanation and forecasting. Structural models excel at elucidating when and why systemic risks may emerge and how policies can mitigate them (Darracq Pariès et al., 2011, Clerc et al., 2015, Darracq Pariès et al., 2019). However, they often lack the realism and level of detail expected from forecasting models. Data-driven stress testing models can reliably translate macro-financial scenarios into future banks’ balance sheets. They are realistic but tend to have a narrower focus, missing the broader picture of interactions within the financial system. Structural and data-informed models have sometimes been combined in large-scale macroprudential stress testing platforms (Feldkricher et al., 2013, Henry and Kok, 2013, Figure, 2017, Dees et al., 2017, Correia et al., 2022). Nonetheless, these platforms have grappled with issues of consistency and being solved sequentially, module by module, have struggled to replicate two-way feedback mechanisms that give rise to systemic risks.

The BEAST model stands for a brand-new vision of modelling for financial stability purposes. It is a single multi-purpose forecasting and simulation model designed to tackle varied policy questions within the scope the ECB macroprudential mandate. To achieve this, it melds decades of central banks’ forecasting experience from semi-structural models with the goal of analysing the interplay between economies and many often-dissimilar banks.

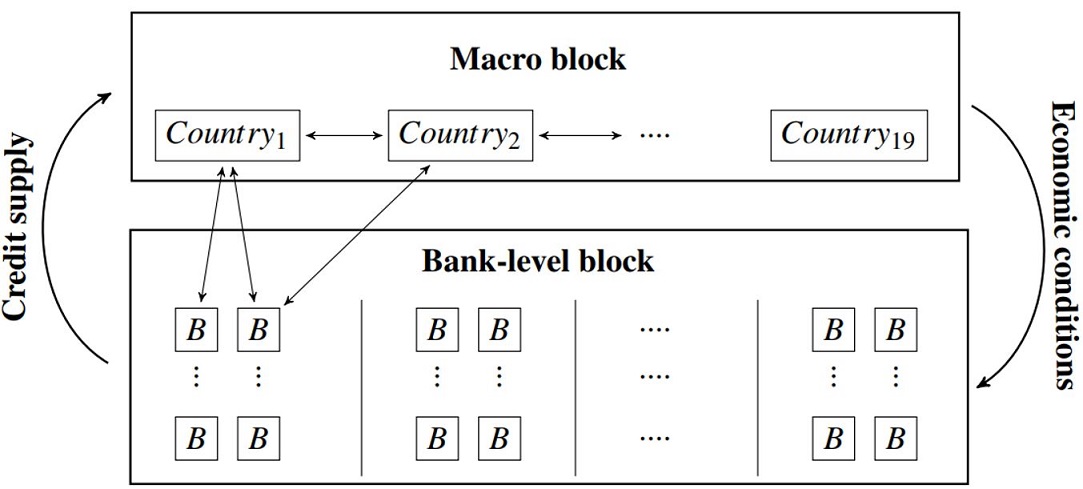

The BEAST is a semi-structural model that encompasses individual economies and banks. The model includes 19 individual euro area economies and additional 18 economies from the rest of the world with strong financial ties to the euro area. Each economy is represented by macroeconomic and financial variables such as GDP, inflation, house prices, and government bond yields. Euro area countries are connected by a common monetary policy and bilateral trade linkages.

Notes: Country1 −Country1 represent individual euro area economies, B represents an individual bank. Straight arrows connecting countries highlight the presence of cross-border trade spillovers. Banks headquartered in a country are positioned below the country label. The straight arrows connecting countries and individual banks indicate the two-way interactions between banks and economies, where these banks have exposures or source funding. The two curved arrows on the sides of the figure represent the direction of the two components of the interactions between banks and economies.

The model includes approximately 90 of the largest euro area banks, collectively accounting for around 70% of euro area bank assets. Each bank has a unique balance sheet with a detailed breakdown of assets and liabilities. They operate within a monopolistic lending market competition while acting as price-takers in funding markets. Banks adjust loan volumes and interest rates based on loan demand, which changes with the business cycle and market interest rates. However, they also encounter supply constraints rooted in their own solvency, leverage, profitability, asset quality, and funding costs. When a bank faces a capital shortfall or experiences persistent asset quality deterioration, it tends to deleverage, especially in loans to foreign markets and the non-financial private sector. Banks’ equity can be increased through profit retention, and their debt structure reflects the availability and relative costs of different funding sources.

Banks’ lending and funding activities give rise to cross-border financial spillovers. Simultaneously, their lending decisions impact the macroeconomic outlook, introducing a banking sector – real economy feedback loop.

Finally, banks must comply with system-wide and bank-specific capital and liquidity regulation. Their regulatory capital targets consider requirements and buffers under Pillar I and Pillar II, supplemented by the leverage ratio requirement. The regulatory capital targets tighten the belt on banks’ profit retention and lending. Additionally, banks calculate two liquidity ratios: the liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR). These ratios influence banks’ choices regarding market funding.

A semi-structural setup of the BEAST model combines data and structural elements. Most of its behavioural equations, which express how macroeconomies and banks respond to changes in their environments, are estimated using country-, bank-, or transaction-level data. However, their empirical specifications are firmly grounded in theoretical foundations. Other structural elements of the model include aggregating identities, regulatory limits, and accounting rules. These structural components ensure that the model can “tell a story” and provide a coherent narrative for each of its results.

Moreover, the BEAST is the first of its kind with the inclusion of individual banks and their feedback into the real economy. This feature adds value compared to structural models that consider the aggregate banking system. By jointly solving its equation, the BEAST maintains greater consistency and offers deeper insights into systemic risks compared to large-scale macroprudential stress test platforms. The model’s stochastic simulations can measure the uncertainty of forecasted economic or banking outcomes, supply at-risk measures, or produce alternative and possible future macro-financial scenarios, such as recessions or financial crisis.

The BEAST has worn many hats throughout its lifetime as a policy model, continuously evolving in response to ever-changing policy questions. It has assessed risks, serving as the primary tool for the ECB macroprudential stress tests of the banking sector (Budnik et al. 2019, Budnik et al., 2021a), or delivering the first euro area climate stress test (ESRB, 2020). From these applications, the model has derived its meticulous representation of banks’ balance sheets and profit and loss accounts. The BEAST has also provided the backstage pass to evaluating regulatory reforms (Budnik et al., 2021c, 2022a), dissecting prudential policies (Budnik et al., 2021b, 2022b), and understanding their interactions with monetary policies. These applications are the reason behind its in-depth knowledge of prudential and monetary instruments.

Most significantly, the BEAST serves as a “guinea pig” for testing the capabilities and limitations of semi-structural models in the realm of financial stability. Its journey has demonstrated that a single-system model with individual banks can be effectively created and beneficially utilised within a policy institution. This experiment has also underscored the unique advantages of such models, including their ability to capture many facets of banks’ heterogeneity, explore various data sources, and facilitate internal and external communication by producing narratives for each result.

Budnik, K., M. Balatti, I. Dimitrov, J. Groß, I. Hansen, M. Kleemann, F. Sanna, A. Sarychev, N. Sinenko, M. Volk, G. Covi, and di Iasi (2019), Macroprudential stress test of the euro area banking system. Occasional Paper Series 226, European Central Bank, July 2019.

Budnik, K., L. Boucherie, M. Borsuk, I. Dimitrov, G. Giraldo, J. Groß, M. Jancoková, J. Karmelavicius, M. Lampe, G. Vagliano, and M. Volk (2021a). Macroprudential stress test of the euro area banking system amid the coronavirus (COVID-19) pandemic. Report, European Central Bank, October 2021.

Budnik, K., I. Dimitrov, J. Groß, M. Jancoková, M. Lampe, B. Sorvillo, A. Stular, and M. Volk (2021b), Policies in support of lending following the coronavirus (COVID 19) pandemic. Occasional Paper Series 257, European Central Bank, May 2021.

Budnik, K., I. Dimitrov, C. Giglio, J. Groß, M. Lampe, A. Sarychev, M. Tarbé, G. Vagliano, and M. Volk (2021c). The growth-at-risk perspective on the system-wide impact of Basel III finalisation in the euro area. Occasional Paper Series 258, European Central Bank, July 2021.

Budnik, K., I. Dimitrov, J. Groß, P. Kusmierczyk, M. Lampe, G. Vagliano, and M. Volk (2022a), The economic impact of the NPL coverage expectations in the euro area. Occasional Paper Series 297, European Central Bank, July 2022.

Budnik, K., I. Dimitrov, J. Groß, and A. Caccia (2022b), Using the ECB macroprudential stress testing framework for policy assessment – lessons learned from the COVID-19 pandemic. Macroprudential Bulletin, 17, 2022.

Clerc, L., A. Derviz, C. Mendicino, S. Moyen, K. Nikolov, L. Stracca, J. Suarez, and A. Vardoulakish (2015), Capital regulation in a macroeconomic model with three layers of default, International Journal of Central Banking, 40th issue, June.

Correia, S., M. P. Seay, and C. M. Vojtech (2022), Updated primer on the forward-looking analysis of risk Events (FLARE) model: A top-down stress test model, Finance and Economics Discussion Series 2022-009, Federal Reserve Board, 2022.

Darracq Paries, M., Ch. Kok, and E. Rancoita (2019), Macroprudential Policy in a Monetary Union with Cross-Border Banking, Working Paper Series No. 2260, European Central Bank, March 2019.

Darracq Pariès, M., Ch. Kok, and D. Rodriguez-Palenzuela (2011), Macroeconomic Propagation under Different Regulatory Regimes: Evidence from an Estimated DSGE Model for the Euro Area, International Journal of Central Banking, vol. 7(4), pages 49-113, December.

Dees, S., J. Henry, and R. Martin (ed.) (2017), STAMP€: Stress-Test Analytics for Macroprudential Purposes in the euro area, e-book, European Central Bank, February 2017.

Henry, J. and C. Kok (ed.) (2013), A Macro Stress Testing Framework for Assessing Systemic Risks in the Banking Sector, Occasional Paper No. 152, European Central Bank, March 2013.