This Policy Brief is based on DNB Working Paper No. 789. Views expressed are those of the authors and do not necessarily reflect official positions of De Nederlandsche Bank.

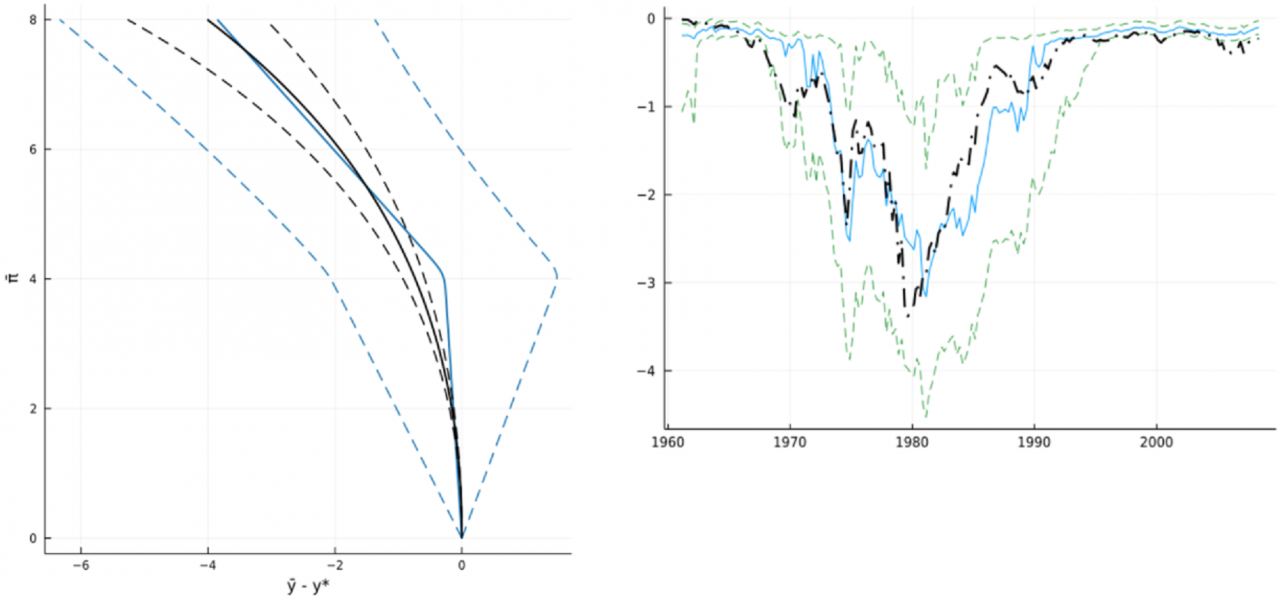

Is there a relation between inflation and output in the long run? The answer is no, according to undergraduate macroeconomics textbooks. In a recent DNB working paper (Ascari et al. 2023) we question this view by showing that, in US data, inflation and output are negatively correlated in the long run: persistently high inflation is associated with sizeable output losses. Under the natural rate hypothesis introduced by Phelps (1967) and Friedman (1968), there is a short-run tradeoff between inflation and output (or the unemployment rate), but this tradeoff disappears in the long run. This idea has been playing a cornerstone role in macroeconomics, inspiring the development of modern monetary theories and becoming one of the working assumptions of central banks in the implementation of monetary policy.

See Ascari and Sbordone (2014).