What are central banks held accountable for by elected officials? In Ferrara et al. (2021), we employ structural topic models on a new dataset of the Monetary Dialogues between the Members of the European Parliament (MEPs) and the President of the European Central Bank (ECB) from 1999 to 2019. Our findings are twofold. First, we uncover differences in how MEPs keep the ECB accountable for its primary objective, i.e., price stability. Second, we show that unemployment is a key explanatory variable for the political voice articulated by individual MEPs in accountability settings. These findings reveal the existence of a “political” Phillips curve reaction function.

Over the past decade, central banks worldwide have significantly expanded the policy toolkit through which achieve their price stability objective. Among the several consequences of the expansion of monetary policy tools, central banks’ recent actions have revived the debate about the relationship between independence and accountability (de Haan et al., 2008; Fraccaroli et al., 2018; McPhilemy and Moschella, 2019; Tucker, 2019), with its implications in term of trust and transparency (Reichlin et al., 2021; van der Cruijsen and Samarina 2021).

Indeed, central banks’ responses to the financial and economic crises of 2008 and 2020 have raised important questions on whether central banks’ accountability frameworks “are well adapted to the new era of highly interventionist central bank policies” (Braun and Hoffmann-Axthelm, 2017) and adequate to the challenge of ensuring that independence does not stand in the way of “the normal public conflict and institutional checking before policy is made” (Jacobs et al., 2021).

While an extensive literature in economics and political science exists on the procedures and mechanisms through which central banks account for their actions (de Haan et al., 2005; Crowe and Meade, 2008; Masciandaro and Quintyn, 2016; Moschella et al., 2020), far less attention has been devoted to the other side of the accountability relationship, namely the political voice through which policymakers keep the central bank accountable (notable exceptions are Schonhardt-Bailey, 2013; Collignon and Diessner, 2016; Fraccaroli et al., 2020).

This neglect is not without consequences. A limited understanding of the standards against which policymakers consider the central bank accountable risks obscuring the informal channels through which politics exerts influence on monetary policy despite the de jure statutory arrangements in place to safeguard central bank independence. This is especially the case at a time when independence looks particularly vulnerable because of populist politics, rising public debt, and dwindling public support for central banks, at least in advanced economies (Goodhart and Lastra, 2018; Rodrik, 2018; Masciandaro and Passarelli, 2019; Peia and Romelli, 2019). Therefore, a key question arises: what are central banks held accountable for by elected officials?

So far most of the literature on accountability, including the one on central banks, has largely focused on examining the procedures and mechanisms through which the agent provides information and explanations of its conduct to its political principals. Put differently, overwhelming attention has been paid to how central banks provide information and justify their decisions before national legislatures in oversight committees (Schonhardt-Bailey, 2013) and to the general public by way of transparency, among the other means (Geraats, 2002; Van der Cruijsen and Eijffinger, 2010; Crowe and Meade, 2008; Hansen et al., 2018).

This focus on the modalities through which central banks account for their decisions has been extremely important to assess central banks’ behaviour. The adoption of this perspective has also led to the conclusion that central banks are “formally accountable to politicians to the extent that politicians can require the agency to provide information on, and explanation of, its conduct on the basis of statutory provisions” (Koop and Hanretty, 2018). This conclusion implies that elected officials hold the central bank accountable against the mandate they delegated to it in the first place.

In practice, however, this might well not be the case. Politicians can voice accountability concerns that are not necessarily based on the statutory goals that a central bank is expected to pursue. For instance, recent evidence indicates that, among other technocratic actors, central banks are subject to scapegoating, with policymakers publicly blaming them for negative economic conditions, especially in the aftermath of crises (Traber et al., 2020). Thus, it is plausible to expect policymakers to hold central banks accountable not just for maintaining price stability, but also for creating the conditions that might favour their re-election.

Evidence of this pattern can be found in populist attitudes towards central banks following the 2008 global financial crisis. Indeed, a growing number of politicians, most notably the former US President Donald Trump, had since then made central banks the target of public criticisms for their alleged failures in sufficiently supporting economic growth (Bianchi et al., 2019). This trend is by no means foreign to Europe. The legality and legitimacy of the ECB’s measures to tackle the European sovereign debt crisis has been increasingly questioned by key policymakers (Stark, 2012; Varoufakis, 2017) and influential scholars (Sinn, 2014; Charles, 2015). This trend has continued well after the financial crisis. Politicians and observers have violently attacked the ECB, and some of them have blamed its expansionary policies for the rise of radical right-wing parties (Financial Times, 2016) and the “expropriation” of European savers (Bild, 2020).

Notwithstanding the increasing number of political challenges to independent central banks, previous studies have largely ignored the behaviour of the political principals in the formal accountability relationship central banks are subject to. In other words, little systematic analysis has been carried out on the voice of politicians on monetary policy, i.e., on the voice articulated by elected officials in the act of holding the central bank to account for its policies and behavior.

A few studies constitute interesting exceptions in this regard. First, Schonhardt-Bailey (2013) uses quantitative text analysis to investigate the content and quality of hearings of the Fed’s Monetary Policy Report in the US Congress from 1976 to 2008. Her analysis shows that members of Congress have little interest in engaging with technical aspects of monetary policy and have greater appetite to steer the discussion in a way that allows them to look good in the eyes of their constituencies. Second, Collignon and Diessner (2016) make use of evidence from a survey conducted with MEPs to argue that the Monetary Dialogues between the ECB and the European Parliament play a significant role in informing and involving MEPs on monetary policy issues.

Closer to our study, Fraccaroli et al. (2020) analyse the textual content of central bank parliamentary hearings in a comparative perspective, considering the euro area, the UK and the US. Based on dictionary-based approach to text analysis, they aggregate all speeches in each parliamentary hearing and provide evidence that policymakers’ sentiment towards central banks is more negative when economic uncertainty is higher and when inflation is more distant from the central bank’s inflation aim. Moreover, they show that the salience attributed to price stability issues is lower when unemployment in the euro area, the UK and the US is higher.

While the results of our paper appear consistent with part of the evidence offered by Fraccaroli et al. (2020), in Ferrara et al. (2021), we extend the analysis in two important aspects. Methodologically, rather than relying on dictionary-based approaches to distinguish among specific accountability issues, our study employs state-of-the-art topic modelling techniques to provide a more complete picture of the issues discussed by MEPs in their efforts to hold the ECB accountable to the European public. Substantively, compared to previous studies, we investigate the economic determinants of MEPs’ voice on monetary policy at a different level. Focusing on the ECB’s hearings before the ECON Committee of the European Parliament, we analyze MEPs’ speeches at the individual level, rather than aggregating them across all politicians in each parliamentary hearing, as in Fraccaroli et al. (2020). Moreover, our assessment is centred on country-level macroeconomic determinants, rather than aggregate euro area values. This allows us to better explore the reaction function of individual MEPs and study its sensitivity to cross-country macroeconomic heterogeneity within the EU, something that is not possible when aggregating speeches at the hearing level and when focusing on determinants at the euro area level. In the next section, we present the data and method we make use of in our analysis.

We investigate politicians’ voice on accountability by examining the hearings of the European Central Bank (ECB) before the members of the European Parliament (MEPs) in the framework of the quarterly Monetary Dialogues. Studying elected officials’ accountability practices towards the ECB offers a number of important empirical advantages. To start with, as a supranational central bank, the ECB’s performance is subject to the scrutiny of politicians whose preferences vary along different country and political dimensions. Thus, zooming on the political voice articulated within the European Parliament allows us to analyse the effect of economic heterogeneity among the different constituencies represented by elected officials. A further advantage of studying the ECB stems from the fact that the institution has a primary mandate that singles out price stability as the central bank’s primary objective and subordinates the pursuit of other objectives. These governance features allow us to clearly ascertain whether politicians emphasize the principal or secondary objectives in keeping the central bank accountable. Our empirical analysis of political voice relies on a novel dataset of the ECB’s Monetary Dialogues and state-of-the-art quantitative text analysis techniques. Two major findings derive from the analysis.

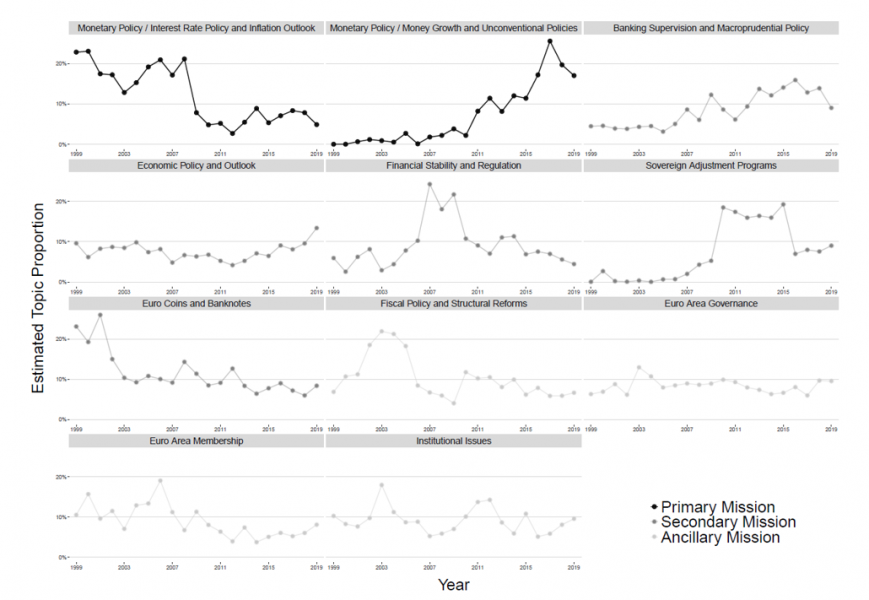

First, we show that political voice on central bank accountability significantly varies over time and across policymakers. In particular, we find that Members of the European Parliament do not always keep the central bank accountable for the primary objective of price stability that has been delegated to the ECB (Figure 1). European politicians also attempt to keep the central bank accountable for a broader set of issues that are connected with, but distinct from, the central bank’s primary goal.

Figure 1. Political voice on ECB by topic and mission (1999–2019)

Source: Ferrara et al. (2021).

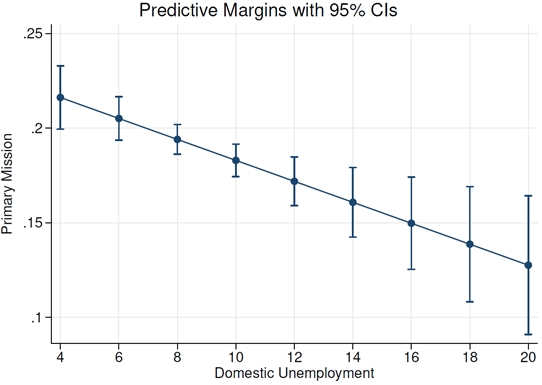

Second, employing panel data, we provide evidence that MEPs react to differentials in unemployment in their constituencies: the higher is the domestic unemployment rate in the country where they have been elected, the lower is policymakers’ attention to price stability (Figure 2). These results reveal the existence of a “political” Phillips curve reaction function that enriches our understanding of the principal-agent accountability relationship between politicians and central bankers.

Figure 2. Marginal Effect of Unemployment on the Predicted Share of MEPs’ Voice on Primary Mission

Source: Ferrara et al. (2021).

Specifically, our results suggest that elected policymakers are less likely to hold the central bank accountable for its primary objective of price stability when labour market conditions are worse in their home country.

The evidence offered in our paper speaks to a lively debate on the mandate of the ECB. Our study has shown that the secondary objectives of the ECB have consistently captured politicians’ attention over the past decade, and more so in contexts facing labor market deteriorations. Despite the increasing importance of the ECB’s secondary mandate, it remains unclear whether and how to provide a ranking of the relative importance of the secondary objectives, and who should be in charge of doing so. This debate has been recently stimulated by the proposal of a group of notable scholars and observers arguing that the European Parliament and the ECON committee should be put in charge political guidance on the ECB’s secondary objectives (Beres et al., 2020). From a normative perspective, by shedding light on the prominence of discussions related to the secondary objectives of the ECB in the Monetary Dialogues, our results support the idea of strengthened and more formalized accountability practices regarding the ECB’s secondary mandate, an issue that has not been extensively addressed by the recently concluded ECB’s strategy review.

In future research, it will be fundamental to ascertain whether and to what extent political voice affects monetary policy. Political voice can indeed be regarded as an informal channel to pressure central banks: politicians may strategically use the voice they articulate in accountability settings to pressure the central bank to focus on some policy issues instead of others. Future research is thus warranted to examine how central banks react to political voice, especially at a time when many forces combine to challenge central bank independence, such as populist politics, weakening levels of public support for technocratic central banks, and worsening public finances following the Covid pandemic.

Bianchi, F., T. Kind, and H. Kung (2019). Threats to central bank independence: High frequency identification with twitter. Technical report, National Bureau of Economic Research.

Bild (2020, Oct). Ezb-chef Mario Draghi: Wie gruselig war graf draghila wirklich?

Braun, B. and L. Hoffmann-Axthelm (2017). Two sides of the same coin? independence and accountability of the European central bank. mimeo.

Charles, W. (2015). Grexit: The staggering cost of central bank dependence. Vox EU 29, 06.

Collignon, S. and S. Diessner (2016). The Ecb’s monetary dialogue with the European parliament: efficiency and accountability during the euro crisis? JCMS: Journal of Common Market Studies 54(6), 1296–1312.

Crowe, C. and E. E. Meade (2008). Central bank independence and transparency: evolution and effectiveness. European Journal of Political Economy 24(4), 763–777.

de Haan, J., S. C. Eijffinger, and S. Waller (2005). The European Central Bank: Centralization, Transparency, and Credibility. MIT Press.

de Haan, J., D. Masciandaro, and M. Quintyn (2008). Does central bank independence still matter? European Journal of Political Economy 24(4), 717–721.

Ferrara, F.M., D. Masciandaro, M. Moschella and D. Romelli (2021). Political Voice on Monetary Policy: Evidence from the parliamentary hearings of the European Central Bank, European Journal of Political Economy, forthcoming.

Financial Times (2016, Apr). Germany blames Mario Draghi for rise of right wing and party.

Fraccaroli, N., A. Giovannini, and J.-F. Jamet (2018). Accounting for accountability at the ECB, Vox, October, 4.

Fraccaroli, N., A. Giovannini, and J.-F. Jamet (2020). Central banks in parliaments: a text analysis of the parliamentary hearings of the Bank of England, the European Central Bank and the Federal Reserve. ECB Working Paper Series, 2442.

Geraats, P. M. (2002). Central bank transparency. The Economic Journal 112(483), 532– 565.

Goodhart, C. and R. Lastra (2018). Populism and central bank independence. Open Economies Review 29(1), 49–68.

Hansen, S., M. McMahon, and A. Prat (2018). Transparency and deliberation within the FOMC: a computational linguistics approach. The Quarterly Journal of Economics 133(2), 801–870.

Koop, C. and C. Hanretty (2018). Political independence, accountability, and the quality of regulatory decision-making. Comparative Political Studies 51(1), 38–75.

Jacobs, L., D. King, et al. (2021). Fed power: How finance wins. Oxford University Press, USA.

Masciandaro, D. and M. Quintyn (2016). The governance of financial supervision: recent developments. Journal of Economic Surveys 30(5), 982–1006.

Masciandaro, D. and F. Passarelli (2019). Populism, political pressure and central bank (in) dependence. Open Economies Review, 1–15.

McPhilemy, S. and M. Moschella (2019). Central banks under stress: Reputation, accountability and regulatory coherence. Public Administration 97(3), 489–498.

Moschella, M., L. Pinto, and N. Martocchia Diodati (2020). Let’s speak more? how the Ecb responds to public contestation. Journal of European Public Policy 27(3), 400–418.

Peia, O. and D. Romelli (2019). Central bank reforms and institutions. Technical report, ifo Institute.

Reichlin, L., K. Adam, W.J. McKibbin, M. McMahon, R. Reis, G. Ricco, B. Weder di Mauro (2021). The Ecb’s tools: Transparency is needed, Vox, December, 3.

Rodrik, D. (2018). Is populism necessarily bad economics? In AEA Papers and proceedings, Volume 108, pp. 196–99.

Schonhardt-Bailey, C. (2013). Deliberating American monetary policy: A textual analysis. MIT Press.

Sinn, H.-W. (2014). The Euro trap: On bursting bubbles, budgets, and beliefs. Oxford University Press.

Stark, J. (2012). The Ecb’s OMTS (out-of-mandate transactions). The International Economy 26(4), 52.

Tucker, P. (2019). Unelected power: The Quest for Legitimacy in Central Banking and the Regulatory State. Princeton University Press.

Traber, D., M. Schoonvelde, and G. Schumacher (2020). Errors have been made, others will be blamed: Issue engagement and blame shifting in prime minister speeches during the economic crisis in europe. European Journal of Political Research 59(1), 45–67.

Van der Cruijsen, C. and A. Samarina (2021). Trust in the ECB during the pandemic. Vox, October, 3.

Van der Cruijsen, C. and S. C. Eijffinger (2010). The economic impact of central bank transparency: A survey. In Challenges in central banking: The current institutional environment and forces affecting monetary policy, pp. 261–319. Cambridge University Press, New York.

Varoufakis, Y. (2017). Adults in the room: My battle with the European and American deep establishment. Farrar, Straus and Giroux.

Author contacts: Federico M. Ferrara, f.m.ferrara@lse.ac.uk; Donato Masciandaro, donato.masciandaro@unibocconi.it; Manuela Moschella, manuela.moschella@sns.it; Davide Romelli, romellid@tcd.ie.