To mark the thirtieth anniversary of the European single market on January 1, 2023, we investigate how intra-EU movement of capital has progressed, against a backdrop of incomplete banking and capital market unions. We find that intra-EU movements of capital lag those of goods and workers over the first 30 years of the single market. Private financial claims within the EU have not only stagnated since the global financial crisis, but their geographical scope has also narrowed, shifting from the EU’s south and east to the heartland and the north. One encouraging development is that the COVID-19 pandemic has not led to further decrease in capital flows to the first two regions. The bold and coordinated policy response to the pandemic has helped maintain private risk sharing. Absent the completion of the banking and capital markets union, fiscal redistribution among EU countries might be needed further, after NextGenEU, to counteract the current centrifugal forces of intra-EU private capital flows. Conversely, the completion of the banking and capital markets union would minimize the need for future transfers among EU countries.

Thirty years ago, Europe established a single market, abolishing internal borders to ensure the free movement of goods, workers, and capital across EU member states. There is no doubt that Europe has benefitted from the single market in those first two areas of movement. But has the intra-EU movement of capital progressed in the same way as the movement of goods and workers?

We focus on cross-border movements of financial capital of a private nature, to see whether private sharing of risk is improving: a key metric for the completion of the capital markets union. The low willingness and ability of European banks to lend, and of capital markets to invest in their immediate neighbor countries, have in the past hindered Europe’s ability to form a genuine economic union. We therefore leave aside the aspects of cross-border movement of physical capital–so called foreign direct investments (FDIs)–as well as cross-border flows of financial capital of public nature, such as those resulting from bond purchases by central banks in the context of quantitative easing programs. Our focus is private capital flows among European countries at the constant perimeter of the 27 EU member states. In our assessment, we extend an analysis conducted by the IMF four years ago on cross-border outstanding financial claims between EU countries (see “A Capital Market Union for Europe, IMF Staff Discussion Note,” published September 2019). We look at cross-border outstanding claims in bonds and equity among EU countries from the IMF’s Coordinated Portfolio Investment Survey (CPIS) as well as cross-border outstanding bank loans from the Bank for International Settlements’ (BIS) locational banking statistics (that is, based on bank residency rather than ultimate risk) and bring them in relation to EU GDP.

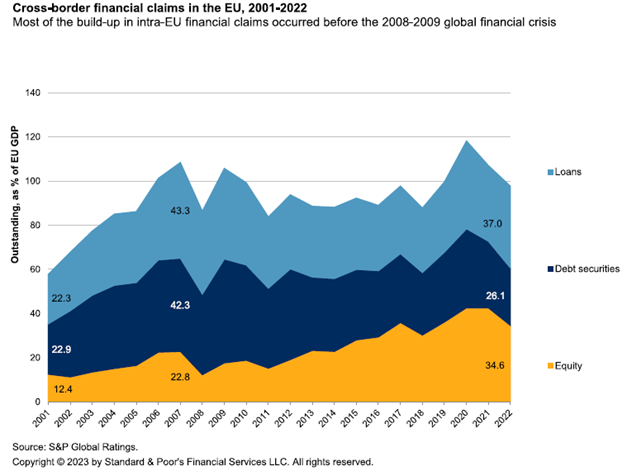

Chart 1: Cross-Border Flows Have Not Declined Since The Pandemic

Outstanding intra-EU private financial claims have increased over the past two decades, accounting for almost 100% of EU GDP in 2022 compared with slightly less than 60% of GDP in 2001 (unfortunately, data is not available for early years of the EU single market in the IMF CPIS). However, part of this increase is due to the valuation of bonds and especially equity–the claims progressing the most over the period–because CPIS data are traditionally marked to market, which is not the case for bank loans in BIS data. For instance, the peak values in cross-border outstanding claims reached in 2020 and 2021 primarily reflect a sharp increase in bond and equity prices because of the global revival of central banks’ quantitative-easing programs and interest rate cuts to address the pandemic. Their valuation is currently receding–bonds more so than equities–as interest rates rise and cross-border outstanding claims tend to return to pre-pandemic levels.

What’s more, the evolution of cross-border private financial claims has not been smooth over time. Most of the build-up occurred before, or more exactly up to, the global financial crisis, with the shares in cross-border loans and bonds almost doubling between 2001 and 2007. This quick build-up was a consequence of the windfall for pan-European savings, which the introduction of the single currency created by eliminating the exchange-rate risk for investments in countries with above-average growth in the region. This episode was not necessarily a success. For example, European private capital flows helped finance the housing boom in Spain and Ireland in the early 2000s and played a role in its crash when they withdrew suddenly. We also remember that several episodes of forced devaluations and revaluations plagued many European economies until a stable solution to the monetary issue was found in the 1990s (see “Making the European Monetary Union, ” by Harold James, published 2014 by Harvard University Press).

The global financial crisis and the following eurozone debt crisis seem to have put a halt to the build-up of intra-EU private capital flows. The post-crises period coincides with a decline in outstanding claims, especially bonds, as their share dropped from 42% in 2007 to 26% in 2022, and it took the launch of the ECB’s quantitative-easing program in late 2014 to reverse this downward trend, at least for cross-border bonds and equity financing. This could be a sign that greater public risk sharing–that is, quantitative easing–encourages private risk sharing.

Intra-EU bank loans’ share of private cross-border financing has not only stagnated since 2007, but is now comparable with that of equities, having halved since 2001. This is all the more surprising given that European banks provide the bulk of funding to the European economy. After the global financial and eurozone debt crises, European banks retrenched from cross-border lending, focusing scarce capital on businesses at home where they had competitive advantage and better understood the risks. In our view, the development of regional branches, which is costly but a practice of some big European banking groups, and the creation of a pan-European deposit insurance scheme (EDIS)–that is, progress in terms of banking union–would create incentives for European banks to increase cross-border lending. Without this, bank lending will retain a national focus and contribute to fragmentation in Europe.

That said, there is also good news regarding the evolution of outstanding intra-EU private financial claims. The pandemic has not led to another decrease in capital flows between European countries from 2020 to 2022, in contrast with the aftermath of the previous two crises. The bold and coordinated response of monetary policy (the ECB’s pandemic emergency purchase program) and fiscal policy (the launch of NextGenEU)–in other words, public risk sharing–prevented a collapse of private risk sharing this time.

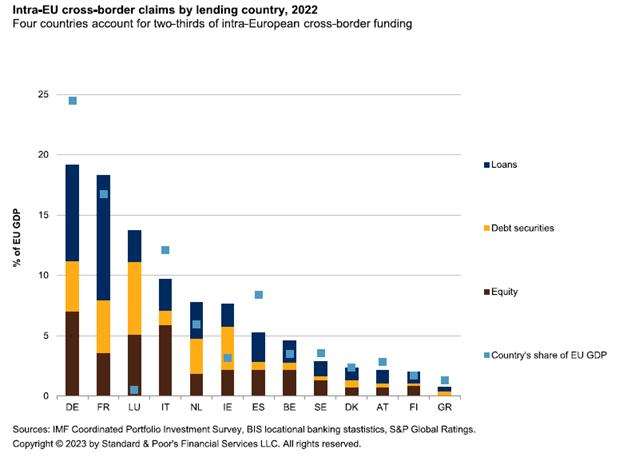

Just four countries account for two-thirds of intra-EU funding (see chart 2). Germany, France, Italy, and Luxembourg are the main lenders to the rest of Europe. Such concentration is not abnormal, given that a country’s lending capacity normally reflects the size of its economy–that is, the depth of its domestic savings pool–and that the size of EU member states’ economies differs considerably. As chart 2 illustrates, the share of cross-border financing from one EU country to another is broadly consistent with that country’s own contribution to EU GDP. For example, the Netherlands contributes 6% to EU GDP and 7% of EU GDP to intra-EU cross-border funding, while Germany contributes 24% to EU GDP and 19% to cross-border funding.

Chart 2:

Luxembourg and Ireland are two noteworthy exceptions to this principle. Both countries fund other EU countries to a greater extent than the size of their domestic economies would suggest. Having been part of the European single market and the European monetary union since inception, Luxembourg and Ireland have developed within Europe as hubs for the investment fund industry, thanks to a competitive legal and regulatory framework. Luxembourg has become the main location for undertakings for collective investment in transferable securities (UCITS) and alternative investment funds in Europe with 27% market share, just ahead of Ireland (19%), Germany (13%), and France (10%), according to the European Fund and Asset Management Association. What’s more, Luxembourg and Ireland are the champions of Europe in terms of true cross-border funds. These are funds investing abroad and promoted by foreign providers–in other words, funded by foreign savings (see “EFAMA Fact Book 2022“). As an example, the Association of the Luxembourg Fund Industry (ALFI) estimated in 2017 that 21% of Luxembourg funds initiators are from the U.S. and 17% from the U.K. (see “Luxembourg: The Global Fund Center,” ALFI, published 2017).

In addition, the geographical breakdown of lender countries differs by asset class. Among the main lenders, French banks top the list of cross-border intra-EU lenders. France has more global systemically important banks (G-SIBs) than any other European country (four out of 30 G-SIBs are French credit institutions according to the Financial Stability Board (FSB). We also find that Luxembourg is more exposed than other European countries in terms of cross-border debt securities. This seems to confirm EFAMA’s estimate that Luxembourg has an impressive 41% market share in UCITS fixed-income funds.

European households still deposit a large share of their financial assets (about one-third) with banks, compared with only 10% with investment funds and 28% with life insurance funds. We saw in the previous section that the share of cross-border funding provided by European banks to other countries has stagnated since the financial crisis, while cross-border equity has improved. The third dimension of the EU single market would benefit from a democratization of investment funds among retail investors, or a democratization of life insurance and pension products among these same retail investors, since the proceeds of life insurance and pension funds products is largely invested in cross-border UCITS funds. By democratization of fund products, we mean a broader dissemination of financial culture among retail investors and the reduction of fees on fund shares, which many in Europe find high (see “Costs and Performance of EU Retail Investment Products 2023,” published by ESMA in January 2023). By comparison, U.S. households have only 14% of their financial assets as checkable and savings deposits at credit institutions, 10% in mutual fund shares, 24% in corporate equities, and 27% in pension entitlements, according to Federal Reserve data.

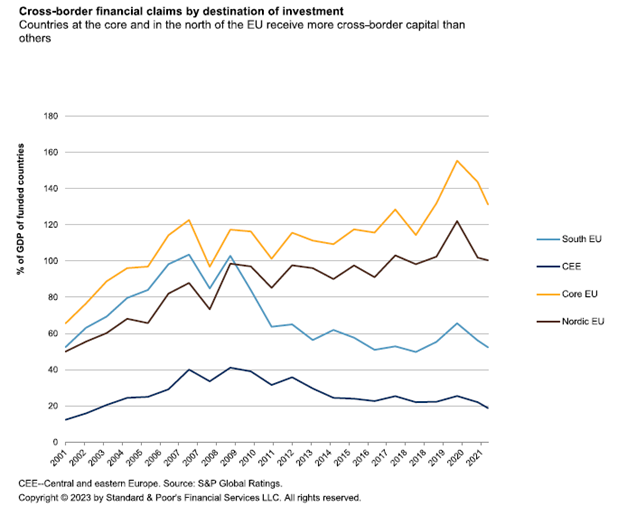

Countries at the core and in the north of the EU receive more capital from other EU countries. Chart 3 reveals a clear divide, which has been growing since 2008 in the wake of the global financial crisis and the eurozone debt crisis: while intra-EU private capital flows had progressed uniformly between EU regions until these two episodes of financial crisis, they have been directed mainly toward the core countries of the EU and the northern countries since then, leaving the southern and eastern countries behind. However, southern and eastern countries of the EU are needing increased investment–that is, more capital to flow in–to catch up with the more mature EU economies. In other words, the current orientation of intra-EU private capital flows does not contribute significantly to the real convergence of EU economies.

Chart 3:

Southern Europe receives roughly 50 percentage points of their own GDP less financing from other European countries compared with pre-global financial crisis. There is a noticeable difference by type of instrument: cross-border equity has been a much more stable source of cross-border funding than loans and bonds. Unfortunately, it is also the most marginal source of funding compared to the others. Europe would benefit from a rebalancing in favor of equity financing, a key priority of the CMU initiatives.

The resulting capital divide can barely be filled by foreign non-EU private capital. In a perfect world, the opposite would be true: intra-EU capital should flow more to the south and east of the EU, where the return on capital is higher than in the north and core of the union, because of higher potential growth.

Could intra-EU public investment play a role in reducing the capital divide? This is a traditional role of the EIB and the EIF, and exactly what the NextGenEU plan of the European Commission is newly intended to do: invest more in the southern and the eastern part of the EU, to foster the green and digital transition in that area. But structural reforms also play a key role. Absent the completion of the banking and capital markets union, fiscal redistribution among EU countries might be needed further, after NextGenEU, to counteract the current centrifugal forces of intra-EU private capital flows. Conversely, the completion of the banking and capital markets union would minimize the need for fiscal transfers among EU countries.