This policy brief is based on Bucher-Koenen, T., Fessler, P., & Silgoner, M. (2024). Households’ risk perceptions, overplacement, and financial literacy. Oesterreichische Nationalbank Working Paper No. 259.

Abstract

This policy brief examines overplacement in households’ risk perceptions: overplacement describes the tendency of individuals to underestimate their likelihood of experiencing certain negative financial shocks compared to similar households. Using data from a randomized survey experiment, we find significant overplacement bias, especially for households with lower financial literacy. This bias can undermine crisis preparedness and lead to inadequate financial planning. Our findings also reveal that households with past experience of economic hardship show stronger risk awareness. These two findings underscore the critical role of both financial literacy and experience for building resilience. To mitigate overplacement and strengthen financial stability, we recommend targeted financial literacy programs focused on risk awareness, particularly for vulnerable groups, to help households build greater resilience against future economic hardship.

Overplacement, a form of overconfidence where individuals assess their own risks as lower than those of others, plays a significant role in households’ financial decision-making. In the context of financial risk perception, overplacement leads households to underestimate the likelihood of adverse economic events, such as unemployment or income loss, occurring to themselves, compared to the same shocks affecting similar households. This phenomenon is particularly prominent among households with lower levels of financial literacy. Through a randomized survey experiment, our study reveals that Austrian households tend to evaluate negative financial shocks as less likely for their own household than for a comparable one, indicating a psychological distance from potential risk. Interestingly, this effect is absent when households are asked to assess positive financial shocks – such as income gains –, suggesting a bias that specifically distorts perceptions of vulnerability.

The overplacement bias carries significant implications for household financial resilience. By underestimating their exposure to financial risks, households may inadequately prepare for economic downturns, leaving themselves more vulnerable in times of crisis. Additionally, our results suggest that financial literacy is not only instrumental for managing finances but also a critical factor for assessing personal risk, enabling households to engage in more proactive and effective financial planning.

Households’ experience with past economic shocks, such as unemployment or significant unexpected expenses, shape their perceptions of future risks. Our study reveals that individuals who have experienced financial setbacks are more likely to assign higher probabilities to similar risks in the future, suggesting that personal experience serves as reference point in assessing potential threats.

These findings highlight the importance of fostering accurate risk perception, especially in economically stable times where households may be more prone to complacency and overplacement.

The randomized survey experiment in our study provides a powerful approach to understanding overplacement bias in household risk perceptions. By randomly assigning respondents to assess financial risks for either their own household (treatment group) or a similar, hypothetical household (control group), we create two comparable groups (similar with regard to characteristics), minimizing the influence of individual differences. This randomization makes it possible to attribute differences in risk assessment solely to overplacement bias, ensuring a high degree of confidence in identifying the effect accurately.

Combined with extensive survey information on each household’s demographics, financial behavior, and financial literacy level, this experimental approach enables robust causal inference. By isolating overplacement bias through randomization and examining its heterogeneity across financial literacy levels, we demonstrate that the overplacement bias decreases with higher financial literacy. With this approach we can show not only that overplacement exists but also how it varies across different groups, offering important insights for policy intervention focused on improving financial resilience.

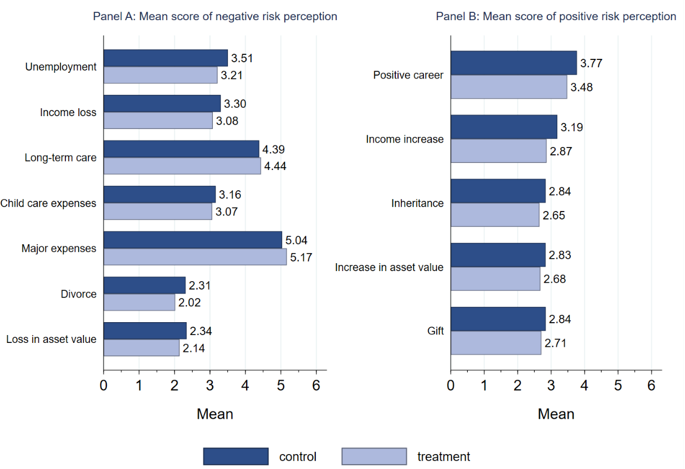

Figure 1 displays the observed differences in risk perception between the treatment group (evaluating risks for their own household) and the control group (evaluating risks for a similar household), to test for the presence of overplacement bias. However, to interpret these differences causally, it’s essential to account for any remaining random variation across socioeconomic groups, which might still exist despite the randomized design. Using causal inference techniques as described in our paper and outlined by Imbens and Rubin (2015), we control for an extensive set of observable characteristics.

Figure 1.

Notes: Panel A shows the mean score of the subject’s risk perception on unexpected negative events. Panel B shows the mean score of the subject’s risk perception on unexpected positive events. The dark (light) blue color reports the results of the control (treatment) group. All scaled from one ((almost) impossible to occur) to ten (will (almost) certainly occur).

Our results reveal that households assess the likelihood of adverse events as 10% to 15% lower for their own risk compared to similar households. Evaluated at the means the effects are rather large and reduce the subjective assessment of the negative event by between 10.0% and 15.6% for unemployment, 10.5% and 11.2% for income loss, and 14.3% and 14.6% for divorce. This suggests that overplacement bias leads many households to underestimate personal financial risks, potentially leaving them unprepared for adverse shocks.

Interestingly, the overplacement effect is absent when households are asked to assess positive financial shocks – such as positive career developments or income gains. Figure 1 shows that – contrary to the overplacement hypothesis – households attach higher probabilities to such strokes of luck to happen to them rather than to similar households. This suggests that the overplacement bias specifically distorts perceptions of vulnerability.

An important insight from our findings is the role of financial literacy in moderating this overplacement bias. Households with higher financial literacy tend to show only minimal or no overplacement bias when assessing financial risks, whereas those with lower financial literacy exhibit stronger overplacement tendencies. This pattern highlights that financial literacy not only equips individuals with knowledge but also affects their ability to accurately assess personal risks – a skill critical for making prudent financial decisions.

The study further reveals that households’ past experiences with financial shocks, such as unemployment or unexpected expenses, significantly shape their risk perception (see also figure 2). This finding emphasizes that direct experience with economic challenges can serve as a reference point.

Figure 2.

Notes: Panel A shows the mean for the binary variables of experience of financial shocks, which takes on the values one and zero; one means that the subject has experienced the financial shocks before and zero otherwise. Panel B shows the mean of the subject’s risk perception on unexpected events, scaling from one ((almost) impossible to occur) to ten (will (almost) certainly occur).

Our findings have significant implications for enhancing household financial resilience. When households underestimate their financial vulnerabilities due to overplacement bias, they may neglect to build adequate savings or take steps to prepare for financial crises. This risk of underpreparedness is especially pronounced during periods of economic stability, where complacency can exacerbate overplacement tendencies. Measures with the aim to improve financial literacy – particularly regarding risk awareness and realistic financial planning – can support households to better understand their exposure to potential risks and induce them to take measures to build financial buffers against future hardship.

Financial literacy programs that emphasize preparedness based on past economic challenges and current vulnerabilities may induce households to build up greater resilience against future economic uncertainties. Given that overplacement bias is most prevalent among those with lower financial literacy, targeted financial education programs are essential. These programs should prioritize helping individuals realistically assess personal financial risks and the importance of precautionary savings. By addressing overplacement directly, such initiatives can encourage more cautious financial behavior and enhance preparedness for economic shocks.

Tailored interventions would also benefit from alignment with specific economic contexts. For example, in Austria, where many households are directly or indirectly linked to small and medium-sized enterprises (SMEs), resilience programs that consider this unique economic landscape are especially relevant. Collaboration between financial institutions, educational bodies, and government agencies can broaden the reach and impact of these programs, ensuring that they cover both general financial literacy and practical skills for managing risks.

In sum, strengthening financial literacy with a focus on risk awareness can likely reduce overplacement bias, bolster financial resilience, and contribute to economic stability.

Imbens, G. W. and D. B. Rubin. 2015. Causal Inference for Statistics, Social and Biomedical Sciences, An Introduction.