The views are those of the authors and do not represent the views of the Central Bank of Ireland or of the Eurosystem.

This paper first provides empirical evidence that the labour market for the less educated workers is much more volatile than for the well-educated ones. We estimate job finding and separation rates by educational attainment for several European countries and find that fluctuations of the job finding rate explain up to 80% of unemployment fluctuations for the less educated. We then construct a HANK model augmented with search and matching and ex-ante heterogeneity in terms of educational attainment level. We show that monetary policy has stronger effects when the job market for the less educated, and more likely poorer workers, is more volatile because they have very procyclical income and high marginal propensities to consume. An expansionary monetary policy shock disproportionally affects the labour market of the poor, causing a strong increase in consumption. This amplifies labour demand and increases labour income of the poor even more, amplifying the initial effect. The same mechanism applies to forward guidance.

The distribution of wealth, the incidence of income (who receives the income), its riskiness, and the cyclical properties of different types of incomes have been shown to matter substantially for macroeconomic fluctuations in heterogeneous agent New Keynesian (HANK) models (Kaplan et al., 2018; Auclert 2019; Broer et al., 2019). In these papers, there was less emphasis on the incidence of labour income itself over the business cycle for different households, even though labour income is typically the most important source of income for most households.

This paper attempts to fill parts of this gap by first providing empirical evidence that labour market outcomes (and therefore labour income) are more sensitive to business cycles and to monetary policy for workers with lower educational attainment. These workers are also more likely to be poorer than the others and are, therefore, more likely to have higher marginal propensities to consume (MPCs). For instance, Elsby et al. (2010) find that males, younger, less educated workers, and individuals from ethnic minorities experience steeper rises in unemployment during all recessions. Patterson (2023) finds that the earnings of individuals with higher MPCs (young, black, and poor) are more exposed to recessions. Using German data, Kramer (2022) finds that the sensitivity is substantially higher at the bottom of the earnings distribution (but not at the top). Moreover, he can attribute this to the fluctuations in the extensive margin rather than to wages.

We first provide new empirical evidence on job finding and separation rates by educational attainment for several European countries, which is novel and of independent interest. We find that job finding rates for the less educated workers are lower, highly procyclical, and more volatile than for the better-educated workers. Separation rates are higher, tend to be more volatile, and often acyclical for less educated workers. Fluctuations in job finding rates contribute most to fluctuations in unemployment of the less educated at cyclical frequencies, with the contribution of job finding rate fluctuations exceeding 80% in countries like Germany and France. In all cases, the evidence suggests that workers with low educational attainment face higher employment risk over the business cycle than workers with high educational attainment. Moreover, empirical evidence suggests that also conditional on a monetary policy shock, the labour market for the less educated is more volatile and that this volatility is due to the fluctuations in the job finding rate.

Then, we build a stylised model with the search and matching framework embedded in a HANK framework that attempts to capture the above empirical regularities. The model considers the economy as composed of different labour market segments, where workers can either stay in the same market segment and face its income risk or exogenously switch to another labour market segment, with different characteristics regarding wage fluctuations and (un)employment risk. These exogenous switches between labour market segments are rare but persistent and can be thought of as persistent changes in the desirability of a particular skill. Each segment functions as a separate labour market with search and matching frictions. This means that each labour market segment has an endogenous job finding probability, which depends on firms’ incentives to create vacancies in that segment, which in turn varies with economic conditions. Cyclical income fluctuations for households that stay in the same labour market segment occur because search frictions, combined with wage rigidities, lead to an increased vacancy posting following an expansionary shock, which increases job finding rates and, therefore, expected labour income within each labour market segment. Because the intensity of vacancy posting differs across labour market segments, the differences between labour market segments change over the business cycle and affect the idiosyncratic labour income risk for households.

Using the model, we show that if poor workers obtain jobs after a monetary expansion (consistent with empirical evidence), they spend more of the additional income because their MPCs are higher. This amplifies aggregate demand, which leads to more labour demand from firms that must meet consumption demand. Because the labour market for the poor is more sensitive to the business cycle, this leads to a relatively stronger increase in employment of poorer households, which in turn leads to a stronger increase in consumption. This works as an amplification mechanism that makes monetary policy more potent. The direct policy implication is that monetary policy will have stronger demand effects when there are more less educated and, therefore, poorer workers among the unemployed.

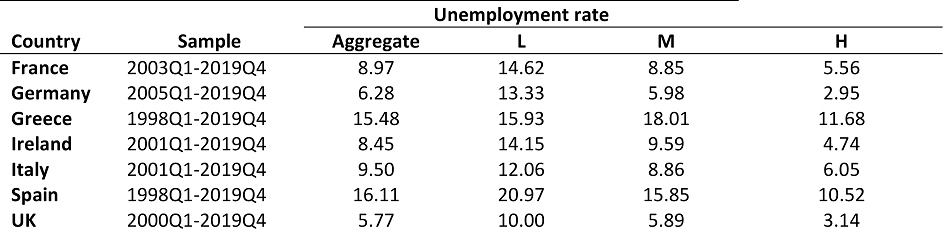

Table 1 shows unemployment rates by educational attainment in several European countries. The empirical regularity is that the unemployment rates for those with the lowest education are typically at least by a factor of 2 (and often by a factor of 3) larger than unemployment rates for those with high education.

Table 1: Unemployment rates by educational attainment

Notes: The table reports unemployment rates by educational attainment, in percent. L = Less than primary, primary, and lower secondary education, M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary education. We end the sample in Q4 2019 to exclude the COVID-19 period. Source: Eurostat.

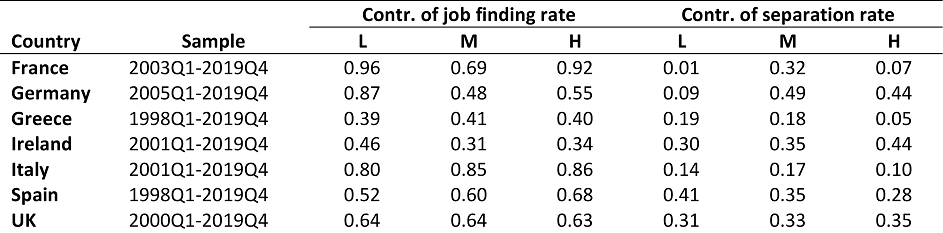

We are, however, interested in what drives these unemployment rates. To this end, we use data on unemployment duration by educational attainment from the Labour Force Survey to compute job finding and separation rates following the approaches by Shimer (2012) and Elsby et al. (2013). Job finding rates turn out to increase with educational attainment, and separation rates fall with educational attainment. Table 2 shows the contributions of the job finding and separation rates to the cyclical variation of unemployment, computed as in Fujita and Ramey (2009). The contribution of the job finding rate tends to be the largest and especially important for the group with the lowest educational attainment, where it drives more than half and often more than 80% of cyclical unemployment fluctuations.

Table 2: Contributions of job finding rate and of separation rate to cyclical variation in unemployment

Notes: The table reports contributions of the fluctuations of the job finding rate and of the separation rate to cyclical fluctuations of the unemployment rate by educational attainment. L = Less than primary, primary, and lower secondary education, M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary education. The rates do not add up to 1 due to the variance contribution of the residual.

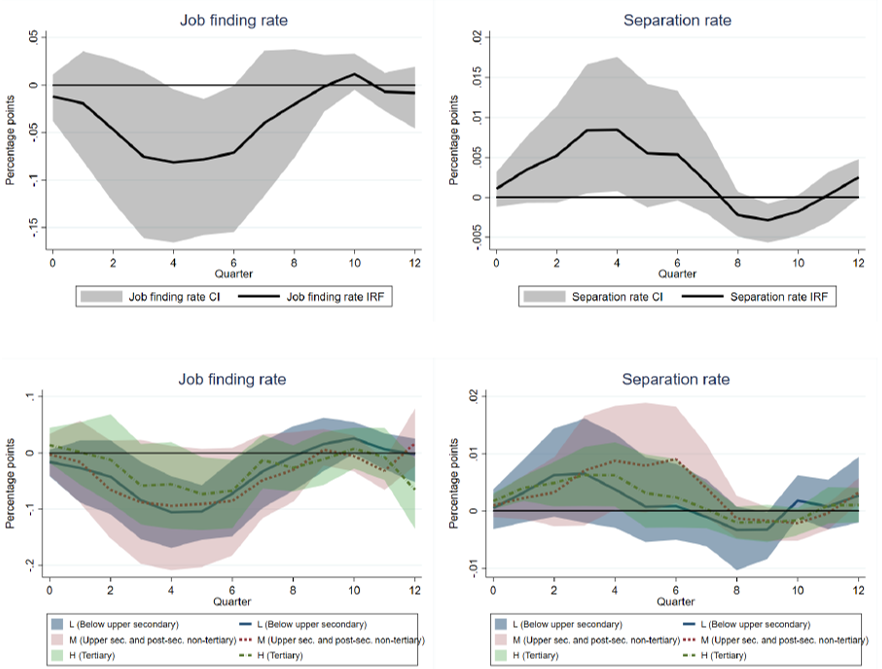

The statistics reported in Table 2 are unconditional – they are the result of all shocks that have affected the economy during the sample period. The question is whether there is an indication that the same logic also holds when conditioning the analysis on an identified structural shock. It turns out that this is indeed the case (see Herman and Lozej, 2023a, for details). Figure 1 shows the responses of total job finding and separation rates in the upper two panels, and the breakdown by educational attainment in the lower panels, all conditional on a contractionary monetary policy shock (a local projection on an identified monetary policy shock in the euro area, as in Jarocinski and Karadi (2020)). Both variables have the expected responses (job finding rates fall and separation rates increase), and the same holds when done separately by educational attainment. However, note that because there are more unemployed at lower educational attainment (see Table 1), the same change in the job finding rate will have more effect on employment of these workers than for those with high educational attainment, simply because the number of the latter in the unemployment pool is small.1 This indicates that the job finding rate is the main driver of (un)employment fluctuations for those with lower educational attainment, also conditional on a monetary policy shock.

Figure 1: Empirical responses to a monetary policy tightening

Notes: The figure shows impulse responses following a contractionary monetary policy shock. Shaded areas are 90 percent confidence bands, which are calculated using wild bootstrap cluster robust standard errors (Roodman et al., 2019). Standard errors are clustered at the country level.

We use this empirical evidence to calibrate our HANK model augmented with search-and-matching frictions and simulate a temporary expansionary monetary policy shock.

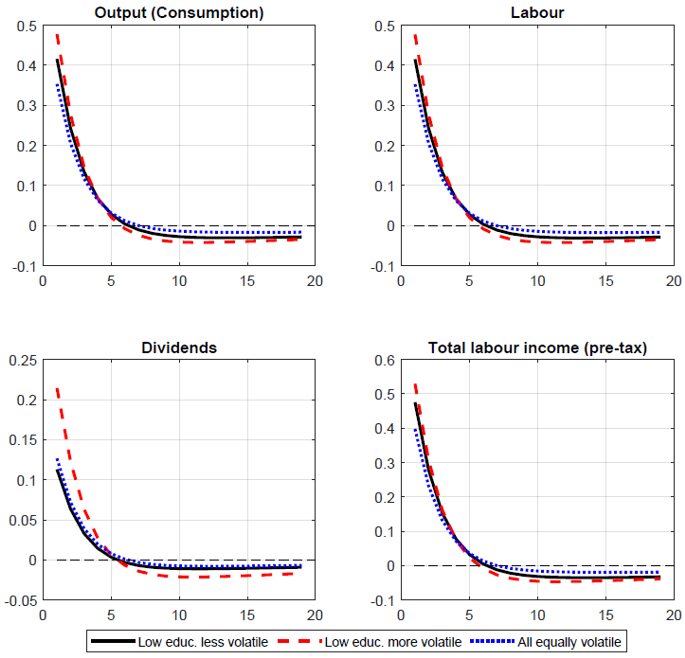

Figure 2 shows the responses of the aggregate quantities to a monetary expansion. The red dashed line represents our benchmark calibration, where the labour market segment for the less educated households is calibrated to be more volatile than the other labour market segments, in line with the empirical evidence. For comparison, we plot the case where the volatility of labour market outcomes is similar across all labour market segments, shown as a dotted blue line. The full black line shows the case where the labour market outcomes for the less educated are only half as volatile as the benchmark case (but still more volatile than the other two labour market segments).

The key finding is that aggregate fluctuations are amplified when the labour market segment of the poor is more volatile. The initial output response is, for instance, 17% higher for the red dashed line compared to the full black line, and this is similar for aggregate labour and labour income responses. The difference in the magnitude of responses is even larger when compared to the symmetric case. Dividends are procyclical due to sticky wages.2

Figure 2: Aggregate responses to an expansionary monetary policy shock

Notes: Impulse responses to a temporary expansionary monetary policy shock. The units on the x-axis are quarters. All responses are percent deviations from the steady state.

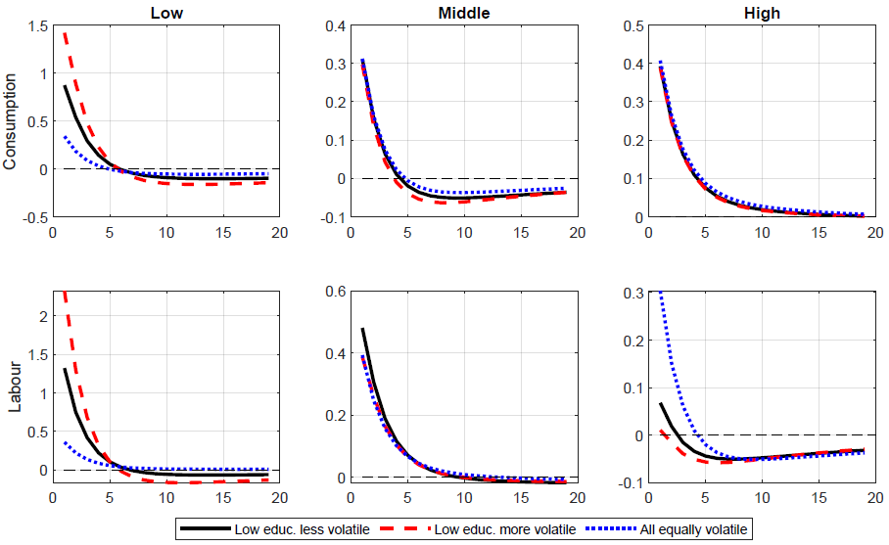

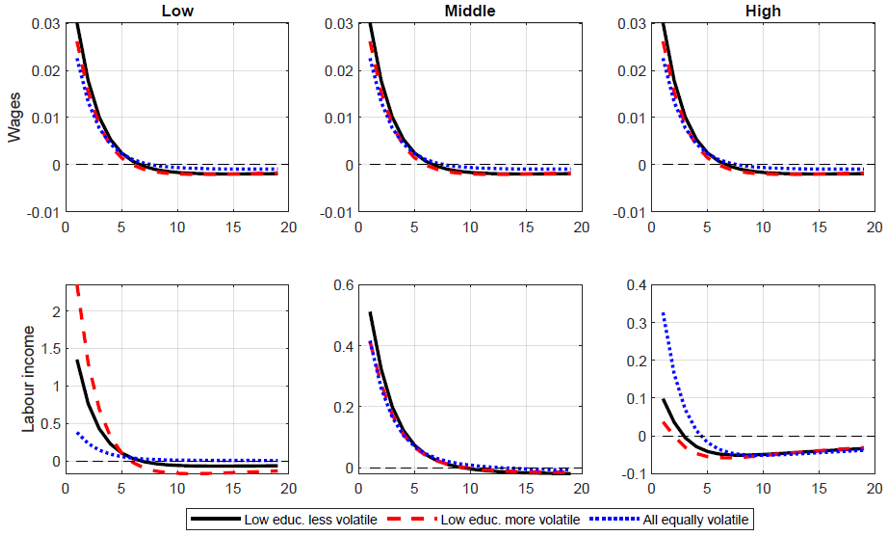

To understand the mechanism behind these results, it is instructive to look at the disaggregated quantities. Figures 3 to 5 show impulse responses of the main variables of interest by labour market segments. First, note in Figure 3 that the labour of the low-educated (poor) households increases substantially in the benchmark case, with the labour market outcomes of the poor more volatile. In contrast, the labour of the highly-educated (rich) households only increases on impact and then falls. This becomes less pronounced if we make the labour market for the poor less procyclical. At the same time, consumption of the poor increases markedly in the benchmark case and follows the pattern of the labour income responses shown in Figure 4. This is because low-educated households in the model are also poor since they are often unemployed and, therefore, receive lower effective wages. The consumption of the rich is almost unaffected, as they can smooth their consumption by changing their asset holdings. Wages respond symmetrically across all labour market segments (the calibrated wage rigidity is the same in all cases shown).

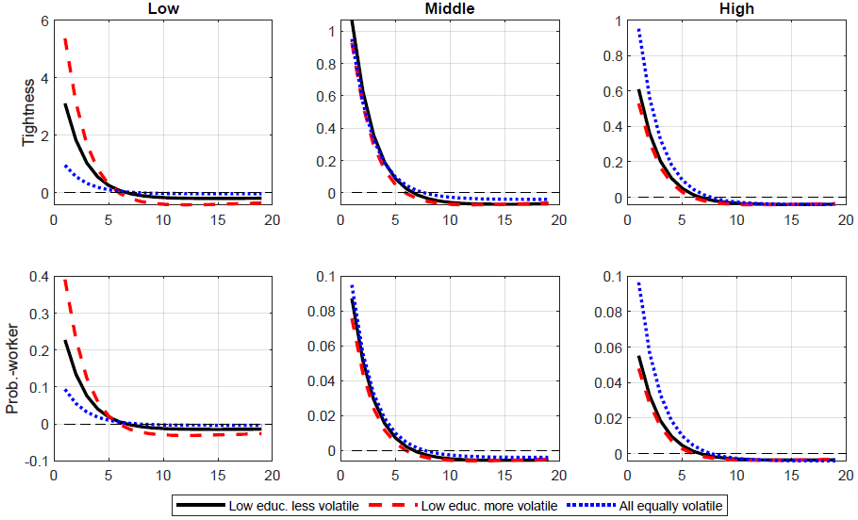

Figure 5 explains the mechanism behind these responses. When the labour market of the poor is more volatile, firms post relatively more vacancies in this labour market segment during the expansion. This is because labour firm profits in this segment are small, in line with Hagedorn and Manovskii (2008), so they increase by more in percentage terms after a positive shock whenever there is some wage rigidity. With more vacancies, labour market tightness in the segment increases, and with it also the job finding probability, causing more employment and more labour income for the poor. Households in this labour market segment have high MPCs, which is why their consumption increases strongly. Even though this labour market segment is small and even though the consumption of households in this segment is also small, the increase in consumption is sufficient to increase aggregate demand, which in turn leads to more labour demand and, again, more hiring from the poor labour market segment, leading to further amplification.

More employment in the poor labour market segment partly crowds out employment in the rich labour market segment, which is why we see a decline in labour in that segment for the benchmark case (in addition to the effect of lower labour supply of these households, who can enjoy both higher consumption and more leisure, as they hold sufficient assets to insure themselves). Note that this is not because firms would not want to hire from this segment (tightness still increases) but because wages and the matching probability in this segment do not rise enough to induce the richer households to supply more labour. When labour market segments are similar in terms of their cyclical behaviour (dotted blue lines), there is little crowding-out on the labour market by the poor households, which leads to a lower income and consumption response. The same mechanisms apply to the transmission of forward guidance.

Figure 3: Consumption and labour

Notes: Impulse responses to a temporary expansionary monetary policy shock. The units on the x-axis are quarters. All responses are percent deviations from the steady state.

Figure 4: Wages and labour income

Notes: Impulse responses to a temporary expansionary monetary policy shock. The units on the x-axis are quarters. All responses are percent deviations from the steady state.

Figure 5: Labour market tightness and job finding probability of workers

Notes: Impulse responses to a temporary expansionary monetary policy shock. The units on the x-axis are quarters. All responses are percent deviations from the steady state, except the job finding probability for workers, which is in percentage points.

We find that in several large European countries, the labour market at low educational attainment levels is typically more precarious, with lower job finding rates than those for high educational attainment. Moreover, job finding rates for low educational attainment are typically also more volatile and more procyclical, which indicates higher labour income risk in this segment of the labour market. Fluctuations in job finding rates explain most of the cyclical fluctuations in unemployment at the lower educational attainment levels.

When we calibrate the model to mimic these empirical characteristics, we find that the effectiveness of monetary policy on consumption and output is amplified. This result is only in part due to poor households having the highest MPCs. There is also a general equilibrium feedback effect from higher aggregate consumption and output that leads to more labour demand. When labour markets of the poor are more cyclical, this leads to more hiring in these segments, which amplifies the income and consumption of the poor households and, hence, aggregate consumption.

An implication of these findings is that whenever there is a large share of unemployed who are poor (for which our low educational attainment level is a proxy), monetary policy is likely to be more potent in stimulating output.

Auclert, A. (2019): “Monetary policy and the redistribution channel,” American Economic Review, 109, 2333–67.

Broer, T., N.-J. H. Hansen, P. Krusell, and E. Oberg (2019): “The New Keynesian transmission mechanism: A heterogeneous-agent perspective,” Review of Economic Studies, 87, 77–101.

Elsby, M. W., B. Hobijn, and A. Sahin (2010): “The labor market in the Great Recession,” Working Paper 15979, National Bureau of Economic Research.

Elsby, M. W., B. Hobijn, and A. ,Sahin (2013): “Unemployment dynamics in the OECD,” Review of Economics and Statistics, 95, 530–548.

Fujita, S. and G. Ramey (2009): “The cyclicality of separation and job finding rates,” International Economic Review, 50, 415–430.

Hagedorn, M. and I. Manovskii (2008): “The cyclical behavior of equilibrium unemployment and vacancies revisited,” American Economic Review, 98, 1692–1706.

Herman, U., and Lozej, M (2023): “Who gets jobs matters: Monetary policy and the labour market in HANK and SAM,” ECB Working Paper 2850.

Herman, U., and Lozej, M (2023a): “Who gets jobs matters: Monetary policy and the labour market in HANK and SAM,” Central Bank of Ireland Research Technical Paper, vol. 2023, No. 10.

Jarocinski, M., and P. Karadi (2020): “Deconstructing monetary policy surprises – the role of information shocks,” American Economic Journal: Macroeconomics, 12, 1-43.

Kaplan, G., B. Moll, and G. L. Violante (2018): “Monetary policy according to HANK,” American Economic Review, 108, 697–743.

Kramer, J. (2022): “The cyclicality of earnings growth along the distribution – causes and consequences,” mimeo, University of Copenhagen.

Patterson, C. (2023): “The matching multiplier and the amplification of recessions,” American Economic Review, 113, 982–1012.

Roodman, D, M. Ø. Nielsen, J. G. MacKinnon, and M. D. Webb (2019): “Fast and wild: Bootstrap inference in Stata using boottest,” The Stata Journal, 19, 4-60.

Shimer, R. (2012): “Reassessing the ins and outs of unemployment,” Review of Economic Dynamics, 15, 127–148.

The opposite will be the case for the separation rate, because the number of workers with low educational attainment in employment is smaller compared to those with middle and high education.

In our model, all dividends are given as lump-sum to the rich households, who can smooth consumption, so the cyclical properties of dividends do not play an important role. Note that because dividend income is also procyclical, it matters less if we distribute it equally.