The opinions expressed in this article are the sole responsibility of the authors and should not be interpreted as reflecting the views of Sveriges Riksbank or the ECB.

Against the recent experience with surging inflation that, at least partly, has been driven by supply shocks to the energy sector, we analyse to what extent a green transition to a state with sustainable energy use is expected to generate upward pressures on inflation – so called Greenflation. We show that a green transition requires the relative price of energy to increase, the relative price of all other goods to decrease, and the real wage to fall. If all prices are flexible, the necessary adjustments can come about without any consequences for inflation. We then extend the analysis to incorporate sticky prices and wages and our findings continues to support the notion that a transition to a green economy may progress without too much consequences for inflation, at least in the case where the fiscal measures are introduced in an orderly and well planned fashion.

It is by now, well established that humans affect the climate by emitting greenhouse gases into the atmosphere, and that this contributes to global warming (IPCC, 2021). The most important greenhouse gas resulting from human behaviour is carbon dioxide (CO2), and it is generated as a by-product when fossil fuel is burnt. The main problem then comes from the fact that it is too cheap—basically free—to emit greenhouse gases into the atmosphere even though these emissions give rise to climate change and climate related costs.

There is, however, a simple solution: we should put a price on carbon dioxide emissions that makes it expensive enough to emit. In other words, the relative price of fossil (brown) energy should increase. With the intention to reduce their emissions, some countries have introduced a carbon tax whereas the EU has adopted the European Union Emission Trading System (EU ETS), which is a “cap and trade” scheme that limits the amount of emissions that can come from EU. Carbon taxes and quantity restrictions are both efficient ways to reduce emissions and both policies will lead to an increase in the price of fossil fuel. The EU has taken even further measures with the “Fit-for 55” package that aims at reducing net greenhouse gas emissions by at least 55% by 2030.1 This will be achieved by linearly reducing the newly emitted emission rights—and thus increasing the price—each year going forward.

In the central banking community there is some concern about “Greenflation”, which we here take to refer to the upward pressures on inflation that might arise from the green transition to a state with sustainable energy production. The concern for Greenflation has likely been amplified by the recent experience with surging inflation, which at least partly has been driven by supply shocks to the energy sector.

Against this background, we (Olovsson and Vestin, 2023) ask two specific questions: what are the inflationary implications of the green transition, and how should monetary policy react during this transition? As our laboratory, we use a New-Keynesian model where firms use energy as an input to produce, and households consume consumption goods and energy services. We consider a region such as the European Union that embarks on a green transition by implementing a policy that increases the price of fossil energy so that fossil energy use falls by about 60% in the coming decades (similar to the Fit for 55 package). We focus on a carbon tax, but as mentioned above, this will have virtually identical implications as a cap-and-trade system.

Before we go into the analysis, it should be mentioned that we consider a scenario where only the EU implements a policy that leads to a green transition. Since the share of global carbon dioxide emissions that are coming from the EU are relatively small, the green transition in EU will only have a marginal effect on global emissions.2

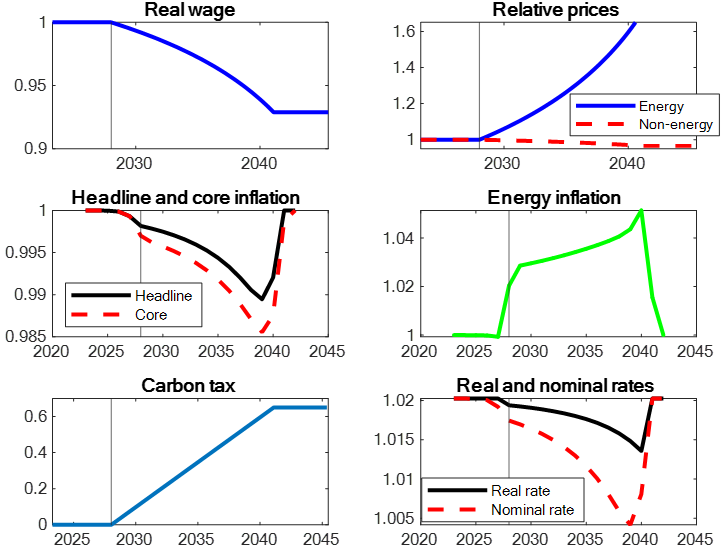

As mentioned above, the green transition as manifested through the Fit-for55-package features a linearly increasing price of brown energy, with the increase taking place over about two decades. In the short to medium run, this increase will lead to an overall increase in the relative price of energy. The reason is that it implies switching to more expensive energy inputs.3 With higher production costs, output will decline and the real wage will fall. In other words, a tax on brown energy increases the relative price of energy, decrease the relative price of all other goods – which we from now on will refer to as “non-energy goods” – and decrease the real wage. Furthermore, the falling level of output generates a decline in the real interest rate. These are the real economic changes that the green transition will bring about.

The inflationary consequence of the necessary relative price adjustment will then depend critically exactly on how monetary policy is conducted, and the extent to which the economy features sticky prices and wages. We start our analysis in a setting where all prices and wages are fully flexible.

In an economy with fully flexible nominal prices and wages, and where the central bank employs a Taylor rule that sets the nominal interest rate in response to how much inflation deviates from its target, we show that current inflation is fully determined by the expectations of current and future real interest rates. Since (as mentioned above), the real interest rate is falling in our main scenario, this, perhaps surprisingly generates a (slight) downward pressure on inflation.

These results are plotted in Figure 1. The top graphs plot the responses of the real wage and the relative prices. The middle graphs provide the inflationary consequences for headline (Consumer Price Index, CPII), core (headline inflation excluding energy inflation) and energy inflation. Finally, the bottom graphs plot the carbon tax and the real and nominal interest rates.

Figure 1: The green transition

Note: The grey vertical line denotes the first year that the carbon tax is increased.

Exactly how much downward pressure that the green transition puts on inflation depends critically on how aggressive the Taylor rule is: the higher the weight on remaining on the inflation target is, the less downward pressure on inflation there will be. It is, in fact, possible to drive down the inflationary response arbitrarily close to the target with a high enough weight.4

Alternatively, the central bank could “see through” the energy price increase and instead focus exclusively on core inflation. In this case, monetary policy could be designed so that core inflation would not at deviate at all from its target, which would imply a larger nominal price adjustment of energy in order to keep the relative price at the desired level. This would also imply a higher level of CPI inflation. Under flexible prices, however, the real effects would be unchanged.

Let us now introduce nominal rigidities of the type considered in most work related to monetary policy into the analysis. In contrast to without nominal rigidities, monetary policy may now have real effects on the economy. We start with the case with sticky prices, while maintaining the assumption that wages are fully flexible. To be specific, it is assumed that that prices of non-energy goods are sticky, but we maintain the realistic assumption that energy prices are flexible. For simplicity, we assume that the inflation target is zero.

If the central bank in this economy targets CPI inflation, then the price of non-energy goods must fall when the energy prices increase in order to make sure that the CPI index does not deviate from its target. However, if prices on non-energy goods are sticky so that not all these prices can change at once, then the result will be a costly price dispersion that gives rise to an inefficient allocation of goods.

So how should monetary policy be conducted in this setting? A well-known result in the monetary-policy literature is that it is optimal for the central bank to focus on the sectors with more rigid prices.5 The reason is that flexible prices can adjust to achieve the correct relative prices vis-a-vis the more rigid sectors of the economy.

This implies that the central bank should make sure that core inflation, i.e., the change in CPI excluding energy, remains on target. This policy eliminates the realization of a costly and inefficient price dispersion for non-energy goods. The nominal wage and the price of energy can then simply adjust so that efficient equilibrium with flexible prices can be replicated. In other words, it is optimal for the central bank to “see through” the rising energy prices during the green transition.

If we now consider the case where all prices are fully flexible, but instead assume wages to be sticky, we can apply a similar logic. If, in this economy, the central bank aims at keeping CPI inflation on target, then the nominal wages needs to adjust when the tax rate on energy changes. Similar to the case with rigid prices, the wage rigidity will give rise to an inefficient outcome when the nominal wages adjust in a staggered way.

In this case, it is therefore instead efficient for the central bank to stabilize the nominal wage-growth. The goods prices and the energy price can then adjust to achieve the relative prices that are consistent with the flexible price allocation, and hence replicate the first best.

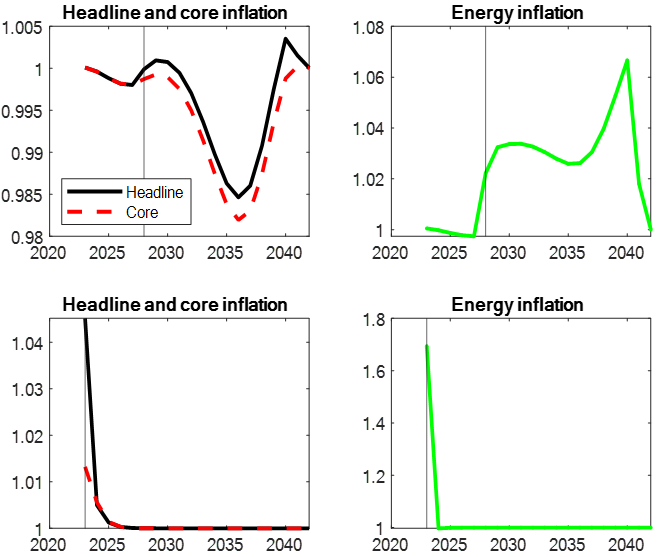

Finally, if prices of non-energy goods and wages are rigid, then it will no longer be possible to implement the efficient solution (i.e., the first best). The price of energy is flexible and it can either adjust so that the relative price between energy and non-energy is correct, or so that the relative price between energy and wages is correct – but not so that both these relative prices are correct. An optimal monetary policy will instead need to accept some deviations of inflation for both non-energy goods and wages. The more rigid wages are and the more costly wage dispersion is perceived to be, the larger the share of the adjustment will go through goods-price inflation and vice versa.6 As shown in the top graphs in Figure 2, our results does not change that much even though prices and wages are sticky.

We conclude that in a simple energy extension of the standard monetary policy model, theory predicts that inflation may remain checked during the transition, provided that monetary policy is well calibrated, which in our setting, implies focusing on core inflation. These theoretical results are in line with the empirical findings in Konradt and Weder di Mauro (2022) that finds only limited effects on inflation from green policies.

Figure 2: The green transition with sticky prices and wages

Note: The top graphs feature a gradual increase of the carbon tax as illustrated in Figure 1. The bottom graphs feature an immediate increase of the carbon tax without any time for firms and households to adjust in advance.

These results may appear surprising, given the recent worrisome surge in inflation, in part triggered by the large increase in the price of energy. We note, however, that the gradual increase in the brown energy tax is important for the results. The bottom graphs in Figure 2 plot a scenario where the transition is abruptly introduced without any chance for firms and households to adjust in advance. In this case, the economy experiences sharp increases in both headline and core inflation, as well as in energy inflation similar to the recent experience with surging inflation.

We find that a green transition requires the relative price of energy to increase, the relative price of all other goods to fall, and the real wages to fall. If prices are flexible, a transition to a green economy can then come about without any consequences for inflation. If goods prices are sticky, but energy prices and wages are flexible, then it is optimal for the central bank to “see through” the rising energy prices during the green transition. Even if both good-prices and wages are sticky prices, our findings continues to support the notion that a transition to a green economy may progress without too much consequences for inflation, at least in the case where the fiscal measures are introduced in an orderly and well planned fashion.

Aoki, K. 2001. “Optimal monetary policy responses to relative-price changes,” Journal of Monetary Economics 48, pp. 55-80.

Del Negro, Marco, Julian di Giovanni, and Keshav Dogra. 2023. “Is the Green Transition Inflationary?”, Federal Reserve Bank of New York Staff Report no 1053.

IPCC, 2021: Summary for Policymakers. In: Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Masson-Delmotte, V., P. Zhai, A. Pirani, S. L. Connors, C. Péan, S. Berger, N. Caud, Y. Chen, L. Goldfarb, M. I. Gomis, M. Huang, K. Leitzell, E. Lonnoy, J.B.R. Matthews, T. K. Maycock, T. Waterfield, O. Yelekçi, R. Yu and B. Zhou (eds.)]. Cambridge University Press. In Press.

Hassler, John, Per Krusell, and Conny Olovsson. 2020. “On the effectiveness of climate policies,” Working paper, IIES, Stockholm University.

Hassler, John, Per Krusell, and Conny Olovsson. 2021. “Directed Technical Change as a Response to Natural-Resource Scarcity,” Journal of Political Economy, 129 (11).

Konradt, M. and B. Weder di Mauro. 2022. “Carbon Taxation and Greenflation: Evidence from Europe and Canada,” Mimeo, Graduate Institute for International and Development Studies

Olovsson, Conny, and David Vestin (2023) “Greenflation?,” Sveriges Riksbank, WP No. 420.

Specifically, the 55% is relative to the 1990 level.

See for instance, Hassler, Krusell, and Olovsson (2022).

A similar result is independently derived in Del Negro et al. (2023).

See for instance, Aoki (2001).

In reality, the central bank mandate typically includes concerns for inflation and real economic stability, such as the output-gap, and not wages. However, several research papers have found that a way to mitigate the adverse effects from wage dispersion is to put a relatively higher weight on the output-gap.